|

Getting your Trinity Audio player ready...

|

Budget 2026 brings attention to how the bond market functions once bonds are issued. For a long time, India’s bond market has had a familiar problem:

- Issuance has grown, but trading has not.

- Investors can buy bonds, but exiting them is often difficult.

- And confidence depends less on returns and more on liquidity and predictability.

This budget addresses that problem in small but meaningful ways. Instead of focusing only on how much the government or companies will borrow, Budget 2026 spends attention on:

- Liquidity in corporate bonds

- Scale and credibility in municipal bonds

- Predictability in government borrowing

- And the way household money moves within fixed income

None of these changes will show immediate impact on yields. But together, they shape how investors think about bonds as instruments they can actually trade, hold and rely on.

Budget 2026: Proposed Reforms for the Corporate Bond Market

One of the most important signals in Budget 2026 is where the focus has shifted in the corporate bond market. For years, policy efforts were aimed at encouraging issuance. This budget focuses instead on improving participation after issuance. That shift is visible in three decisions.

1) Introduction of a market making framework for corporate bonds

A market making framework means having identified institutions whose job is to continuously quote buy and sell prices for selected corporate bonds. Under this framework:

- Certain institutions act as liquidity providers

- They commit capital to buy and sell bonds in the secondary market

- A dedicated funding or support mechanism reduces their risk of holding inventory

Over time, this can lead to more reliable price discovery, narrower gaps between buy and sell prices, greater comfort for investors who may need liquidity before maturity.

2) Permission to introduce futures and options on corporate bond indices

These are derivative contracts based on a basket of corporate bonds, not individual bonds. Instead of trading or selling specific bonds, investors can:

- Hedge interest-rate or credit exposure at the portfolio level

- Adjust risk without touching underlying holdings

Today, if interest-rate risk changes, investors often need to sell bonds to reduce exposure or stay invested even when conditions change. With bond index futures or options – Investors can hedge rate movements using a single instrument and the underlying bonds remain invested.

This improves risk management without forcing exits. For:

- Insurers → better duration control

- Pension funds → flexibility without disrupting long-term allocations

- Large debt funds → smoother portfolio adjustments

3) Total Return Swaps (TRS) on Corporate Bonds

A Total Return Swap allows one party to receive the returns of a bond interest and price changes without owning the bond itself. In a TRS, one party holds the bond on its balance sheet, another party receives the bond’s total return and payments are exchanged based on agreed terms.

TRS expands who can participate in the corporate bond market. It enables:

- Investors with regulatory or balance-sheet limits to gain exposure

- Funds to manage exposure more efficiently

- Better use of capital within the system

Importantly, this does not increase leverage for the market as a whole. It improves capital efficiency and participation.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowMunicipal Bonds Scale-Up

Municipal bonds in India have existed for years, but mostly at a small scale. Issuances were often fragmented, limited in size and largely symbolic. Budget 2026 signals a shift away from that approach.

To boost urban infrastructure, the Union Budget 2026-27 has introduced an incentive for municipal bonds. Specifically, a bonus of ₹100 crore will be awarded for any single bond issuance that surpasses ₹1,000 crore. It pushes large cities to approach the bond market as long-term borrowers with clear projects, predictable cash flows and stronger disclosure standards.

Larger issuances:

- Improve investor interest and participation

- Support better price discovery

- Make municipal bonds easier to track and evaluate

The continued support under AMRUT 2.0 complements this shift. While AMRUT helped smaller and first-time issuers enter the market, Budget 2026 nudged mature cities to move beyond pilot issuances.

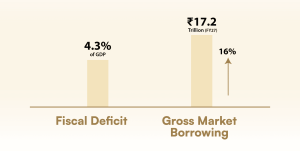

Fiscal Discipline & Borrowing Program

In Budget 2026, the government announced gross market borrowing of ₹17.2 trillion for FY27, an increase of about 16% over the previous year. At the same time, it set the fiscal deficit target at 4.3% of GDP, slightly better than market expectations.

On the surface, these numbers point to higher bond supply in the near term.

The market responded accordingly, with the 10-year G-Sec yield moving up to around 6.78%, reflecting absorption pressure.

Alongside the annual borrowing figure, the budget clearly articulated a medium-term debt path. Government debt is projected at 55.6% of GDP in FY27, with a stated intent to bring it closer to 50% over the next few years.

Earlier, investors largely judged fiscal health through a single lens: the annual fiscal deficit. If the number looked manageable, the market was comfortable and the thinking was:

“A 4.3% fiscal deficit is acceptable.”

Now, the framework is:

“Government debt at 55.6% of GDP, with a clear path to reduce it to 50% by FY31.”

What this shift signals to markets

- Short-term borrowing is acceptable if the long-term debt trajectory improves

- The government is working with a defined four-year glide path, not open-ended deficit targets

- Greater visibility on fiscal discipline helps reduce uncertainty around bond yields

Sovereign Gold Bonds: Taxation Shift

A key change in the taxation of Sovereign Gold Bonds (SGBs) will alter how investors evaluate secondary market purchases.

What Has Changed (Effective April 1, 2026)

- Primary issuance of SGBs: Tax-free redemption on maturity remains unchanged.

- Secondary market purchases: Long-term capital gains (LTCG) will now be taxed at 12.5% on gains.

Impact on Investors

This change effectively ends the popular strategy of buying SGBs at a discount from the secondary market and holding them for eight years for tax-free gains. As a result, the relative tax advantage of secondary market SGBs diminishes.

With this shift, other fixed-income instruments such as tax-efficient Non-Convertible Debentures (NCDs) may appear more attractive for yield-seeking investors. At the same time, gold ETFs and physical gold regain relative competitiveness as gold exposure options compared to secondary market SGBs.

Key Takeaways on Budget 2026 and Bond Market

- The budget focuses on how bonds trade after they are issued, not just on raising money. Liquidity, risk management and exit options are clearly in focus.

- Corporate bond liquidity is being strengthened through structure, not incentives. Market-makers, bond index derivatives and TRS aim to make trading and pricing more reliable.

- New tools allow investors to manage risk without selling bonds. Futures, options and TRS help long-term investors stay invested while adjusting exposure.

- Municipal bonds are being pushed toward a meaningful scale. The ₹100 crore incentive for ₹1,000+ crore issuances encourages serious, trackable borrowing by large cities.

- Fiscal discipline is now communicated through a debt path, not just a deficit number. Markets are given visibility on how government debt is expected to decline over time.

- Secondary market Sovereign Gold Bonds lose their tax edge. This changes relative attractiveness across gold and fixed-income instruments.

Budget 2026: Frequently Asked Questions (Bond Market)

1. What exactly is the “market-making framework” for corporate bonds?

Under Budget 2026, the government proposes to identify and support institutions that will quote both buy and sell prices continuously for selected corporate bonds. These market makers help ensure that buyers and sellers can find each other more easily, improving trading activity and price discovery in the secondary market.

2. How do futures and options on corporate bond indices help investors?

These are derivative tools based on a portfolio of corporate bonds, not individual bonds. They allow investors to manage interest-rate or credit risk at the portfolio level without selling the bonds themselves. This gives long-term investors such as insurers or pension funds more flexibility to manage risk while keeping their bond holdings.

3. What are Total Return Swaps (TRS) on corporate bonds and why do they matter?

A Total Return Swap lets one party receive the interest income and price movement returns of a corporate bond without owning it directly. By separating exposure from ownership, TRS expands the pool of investors who can participate, especially those with balance-sheet or regulatory limits and can support higher trading volumes over time.

4. What incentive is provided for municipal bond issuances and who benefits?

Budget 2026 offers a ₹100 crore incentive for any single municipal bond issuance above ₹1,000 crore. This encourages large urban local bodies to raise significant capital through the bond market for infrastructure projects, improving participation and making municipal bonds more investable at scale.

5. How has Sovereign Gold Bond taxation changed and how does it affect investors?

Previously, capital gains on all Sovereign Gold Bonds were tax-free at maturity, even if bought on the secondary market. From April 1, 2026, only SGBs bought at original issuance and held till redemption remain tax-free. Secondary market SGBs will now be subject to long-term capital gains tax at 12.5%. This reduces the relative tax advantage of SGBs bought after issuance and may make alternatives like NCDs and gold ETFs more attractive.