A good number of investors prefer bank bonds to park their money. There are valid reasons for choosing bank bonds. Here are some of the reasons.

Returns from the bond investments are higher than Fixed Deposit returns.

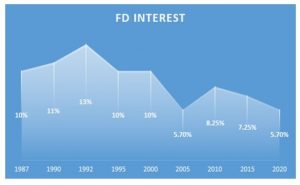

During the year 1987, the FD rates were around 10%, and it was about 13% during the early 1990s. Hence FDs were lucrative. The present FD rate is approximately 5.6% (for a duration between 1 year to 10 years). Refer to the Figure below.

The Bond Interest Rates are higher than the Fixed Deposit Interest Rates offered by the same bank.

Tenure: More than three years of investment As on date: 05/06/2020

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowExample for Bank Bonds:

Entity: State Bank of India

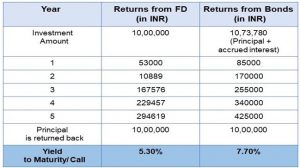

FD Rate 5.30% Maturity 5 years availed.

SBI Bond Paper ISIN INE062A08223 FaceValue 10,00,000 Coupon Rate 8.50% Maturity: 2024 ( 5 years residual maturity left from the date of writing this article )

Total Interest earned by the end of each year (from the time of investment)

Investor earns the following amount more in Bonds = (10,00,000+4,25,000 – 10, 73,780) – (10,00,000+ 2,94,619 – 10,00,000) = 56,601

Also, note that for Bond, the interest payments get credited to the investor’s bank account religiously every year till maturity. So its actual cash flow that the investor enjoys from his Bond investment. If he wants, he can reinvest this amount to earn even higher returns.

On other hand , Bank FD with a special scheme that pays out annually, provides lower effective returns

Note: ADDITIONAL TIER I BONDS (AT1 BONDS)

Tier I Bonds also called Perpetual Bonds. It is a popular option among Banks to raise capital to meet their core capital (Tier1 capital) needs as instructed by RBI. This category carries considerable risk and hence pays high-interest rates to investors. To know more, visit our Bond Glossary.

Why are FD rates low?

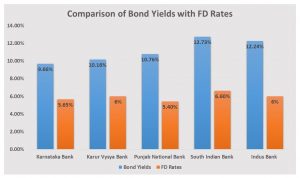

FD rates are lower than bond interest rates. Banks have to maintain CRR(Cash Reserve Ratio) as per regulations laid down by the central bank. The banks have to reserve a portion of capital received via FDs; entire capital can not be lent out. This reserved capital can be utilized to supply closures (or pre-closures) in FD. Such constraints are not there on banks on the capital that is raised via bonds. Hence bond rates are higher than FD rates. Refer to the figure(above). With each one of these banks, you can see bond rates are higher than FD rates.

Bonds are tradable; hence you can sell when interest rates increase, resulting in capital gain. FDs are not tradable, and they come with fixed lockin. The investor has to pay the penalty on premature closure of FD. Both FD and bonds fall into the category of low-risk securities.

Banks provide stability for your investments:

The banking sector is a strictly regulated and well-governed system. The Banking Regulation Act, 1949, governs banks in India. And Reserve Bank of India Act, 1934, makes a strict framework of rules, regulations, and guidelines for banks. BASEL-3 norms strengthen the banking system. Basel-3 norms are the global regulatory framework to manage capital adequacy, financial stress, and market discipline. Above all Foreign Exchange Management Act, 1999, regulates bank’s cross border transactions. Banks are not only well-governed, but they are backed by the government, making them sustainable. Investing with banks is always encouraging.

Liquidity of bank bonds

Banks facilitate savings and investments and lend money to businesses and individuals to bring cashflow into the financial system. Banks need a large amount of capital so that banks can maintain liquidity. One of the ways how banks raise capital is via bonds including upcoming bond IPOs in India issued by leading banks to meet their funding requirements. Hence bank bonds are available most of the time where you can invest and earn the benefits.

There is a proper equilibrium between supply and demand of bank bonds that adds liquidity to bank bonds.

In the worst situation, if a bank is non-performing, a weaker bank will merge with a stronger bank as banks are too big to fail. These were the few reasons why investors prefer bank bonds.

Here is the list of Bank Bonds currently available on our investment platform.

15 comments

Thank you, Ravindra. Can you suggest blog topics? We would be glad to write.

[…] October 10, 2018 | 3 min read Strategy […]

Easy to invest small amount.

Valuable information from you.I am a beginner so, kindly arrange malayalam speaking executive to make conversion by phone .send information to my email.

Best

Good

Very good

Excellent

Do investors in Tier 1 & 2 bonds lose money Incase of bank being taken over by another bank? What are the scenarios under which these investments are lost ?

Additional Tier 1 & 2 bonds are riskier, hence in some circumstances they might be written off. It depends upon the the restructuring that takes place on the time of merger or insolvency.

For any further details, kindly contact our customer care team – contact-us@goldenpi.com

Thank you for your kind words

Thank you for your kind words.

Thank you.

SIB bond is safe as the rated category is A-

Hi Ram,

Thank you for reading our blogs. you can run through the following blog to understand the bond ratings.

https://goldenpi.com/blog/uncategorized/how-to-analyse-the-credit-worthiness-of-corporate-bonds/

Comments are closed.