|

Getting your Trinity Audio player ready...

|

For as long as a decade, bonds have been the sleepiest corner of fixed-income investing. With interest rates on yields sticking close to zero, it was never an alluring enough way to invest. But the economic tables have taken a turn for the better, and bonds are making their way to the top.

With inflation rates on the rise, central banks across the globe are succumbing to the pressure and are compelled to keep their interest rates high. Here’s where things start looking up for fixed-income investments: They provide a safer return on investments with sums that keep up with the inflation.

However, taking your first step in the realm of bonds isn’t so easy, and here are three crucial things a rookie investor should bear in mind:

The Seesaw of Bond Prices and Interest Rates

The first thing a fresh-out-of-the-house investor should know is that bond prices and market interest rates are inversely related; as the interest rate goes up, bond prices go down and vice versa.

When you choose to go with a bond, you’re promising yourself a guaranteed coupon rate for the entire lifespan of that bond or until the time you decide to sell it; whichever comes first. And with the repo rate going strong at 5.25%, the players in the Indian bond market are offering high yields of around 7-8% – rates that help investors sail through the seas of inflation without sinking.

Sticking to short-to-medium term bonds ranging from 1-5 years is the safe way to go, since any sudden changes in the geopolitical environment can cause the repo rate to go up, leaving you with bonds that now provide less value to you as well as anyone in the market for them. In simple terms- A provision that helps you cut your losses.

Start investing with just 10K & grow your wealth with fixed-return bond opportunities.

Explore NowHigh Yields, Credit Ratings, and How They Go Hand-In-Hand

While looking for bonds to invest in, you are bound to come across ones that provide yields that seem highly rewarding, but what you need to consider before locking in is the credit ratings they hold.

Top rating agencies like CRISIL, ICRA, CARE, etc. rate entities on the basis of their creditworthiness, which help investors know how reliable the bonds are if the entity defaults. For newbies, listed bonds with ratings of AA and higher are recommended.

Must Read: Credit Rating Agencies

Therefore a mix-and-match of high-yield and high ratings is key when making a decision, so that you don’t end up being blindsided by the facade of big numbers.

Latest Updates:

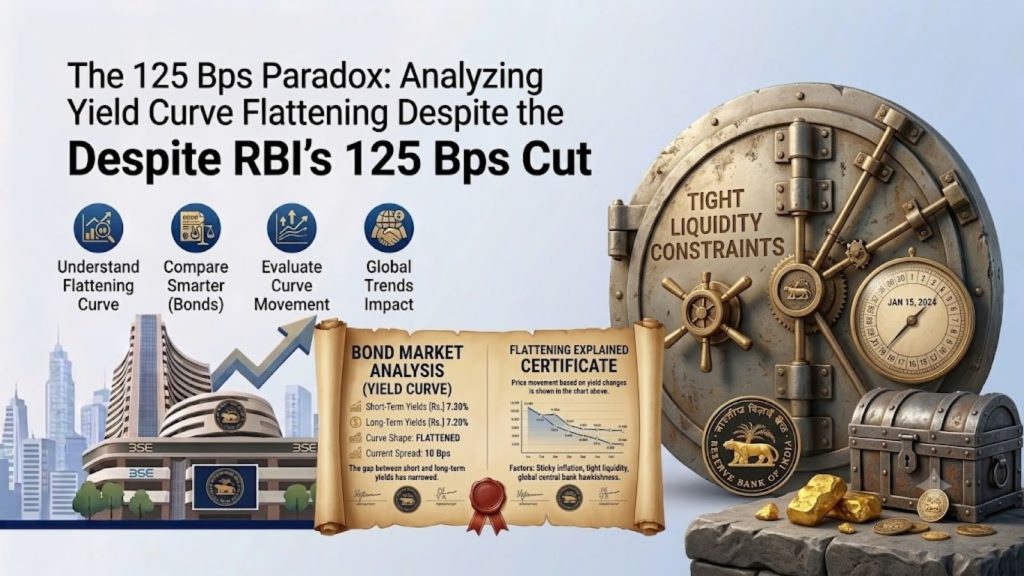

- The Bond Market Paradox: Why Prices Haven’t Rallied Despite RBI’s 125 Bps Cut

- Tax Rules on Sovereign Gold Bond Redemption in 2026: What Investors Should Know

- HDFC Bank Fixed Deposits (FDs) and Interest Rates for July 2026

Maximizing Returns: Why Yield to Maturity (YTM) Matters

When you buy a fixed deposit, you get what you see: A fixed annual return, with no compounded principal. Bonds work differently, where the price of a bond keeps changing every day on secondary markets. This is the reason why every new investor looking to invest long-term should place their bets after a look at Yield To Maturity (YTM).

Imagine a bond issued by a big league corporation with a face value of ₹1,000 and a coupon rate of 8%. If the market interest rate sees a climb, the price of the bond might drop (Remember the seesaw?). And if you buy the bond at the discounted price, you will still not only receive the 8% coupon payout, but the whole ₹1,000 at maturity as well, spelling profit for you in the long run. Conversely, if a highly rated bond is going for a premium, say ₹1100 instead of the original ₹1,000, and you buy it, your returns will be diminished since you paid extra for it.

When you are going through bond listings, always use YTM as the yardstick to compare the actual returns you’ll get in contrast to a FD or other debt instruments.

Conclusion

Investing in bonds in India in 2026 is no longer a hopeless affair. With daunting global oil price hikes and cautious central banks in the picture, fixed-income options are sliding in the good books of investors when it comes to battling inflation and yielding returns. With the repo rate holding steady at 5.25%, yields on 10-year government bonds are scaling north of 7%, which will lead to lucrative returns when the chaos around global oil finally subsides and the repo rate falls. PSUs like NHAI, REC and PCF, are issuing corporate bonds with bigger payouts than bank FDs.

Investing in Bonds in India FAQs

Q. Where can I start investing in bonds?

A. Online Bond Platform Providers (OBPP) help investors navigate through the noise and make sound investment decisions. With a slew of listed bonds to choose from, you can kickstart your bond investing journey without any hassle. Some platforms like GoldenPi even provide 24/7 purchasing authority, so that you can lock in any time you need.

Q. What is the least amount of money I’ll require for investing in bonds?

A. You can start with as little as ₹10,000 when investing in bonds. So you can start without having to worry about first securing a hefty capital.

Q. Which bonds should I invest in as a beginner?

A. Bonds with a rating of AA and higher are what you should be aiming for, as they provide a better guarantee of return with less room for you to bear any major losses.

Q. What happens to my investment if a company goes bankrupt?

A. If a company defaults or files for bankruptcy, bondholders are considered secured creditors. This means you have a legal right to be paid back before any stock investors see a single rupee from the liquidated assets.

Ready to Invest?

Visit GoldenPi to explore current gold bond options. Compare yields, ratings and tenures in one place and invest online with as little as ₹10,000.

Ready to Invest?

Visit GoldenPi to explore current bond options. Compare yields, ratings, and tenures in one place and invest online with as little as ₹10,000.

Disclaimer:

Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities and municipal debt securities/securitized debt instruments are subject to credit risks, market risks, and default risks, including delay and/or default in payment. Read all the offer-related documents carefully. This blog/article should not be construed as financial advice or as an offer or recommendation to buy or sell any security or any products/services of/on GoldenPi or any product/services of its third-party client(s). For a detailed calculation of YTM, visit our website. T&C’s Apply.