For many of us, our parents were the ones who introduced us to the world of investing and saving. And more often than not, their go-to investment option was the good old bank Fixed Deposit (FD). But times have changed, and so have the investment options available to us. So, is FD still the best choice for us, or is it time to explore newer options?

Why FD was a Popular Choice Earlier?

FDs have been a popular choice for many years because they offered a few key benefits:

- Safety: FDs are offered by banks, which are regulated by the government. This means that your money is relatively safe, as banks have to follow certain rules and regulations to ensure the safety of your deposits.

- Guaranteed returns: FDs offer guaranteed returns, which means that you know exactly how much you will earn from your investment. This can be helpful for those who want to plan their finances and budget accordingly.

- Convenience: FDs are easy to open and manage. You can open an FD account at your local bank branch or even online, and you don’t have to worry about actively managing your investment.

Why should milennials consider investing in bonds & debentures?

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowBut why FD may Not be the Best Choice Anymore?

While FDs might have been a great choice earlier, the landscape has changed, and there are a few reasons why FDs may not be the best choice anymore:

- Low-interest rates: One of the biggest drawbacks of FDs is that they offer low-interest rates. With the current low-interest rate scenario, FDs may not provide the returns that you are looking for.

- Inflation: Another factor to consider is inflation. If the rate of inflation is higher than the interest rate on your FD, the value of your money will actually decrease over time. This means that even if you are earning a return on your FD, it may not be enough to keep up with the rising cost of living.

- Limited flexibility: FDs are inflexible, which means that you can’t withdraw your money before the maturity date. This can be a problem if you need to access your money in an emergency or if you want to invest in a different opportunity that comes up.

So, What are the Alternative Options?

If you are looking for higher returns and more flexibility, you may want to consider alternative investment options such as bonds. Here’s why bonds could be a better choice for you:

- Higher interest rates: Bonds generally offer higher interest rates compared to FDs. This means that you can earn higher returns on your investment.

- Inflation protection: Some bonds, such as inflation-indexed bonds, offer protection against inflation. This means that the value of your investment will increase along with the rate of inflation, helping you keep up with the rising cost of living.

- Flexibility: Unlike FDs, bonds offer more flexibility in terms of when you can liquidate. You can choose to hold onto your bonds until they mature or sell them earlier if you need to.

What is Corporate Fixed Deposit?

Why Bonds and Not Fixed Deposit?

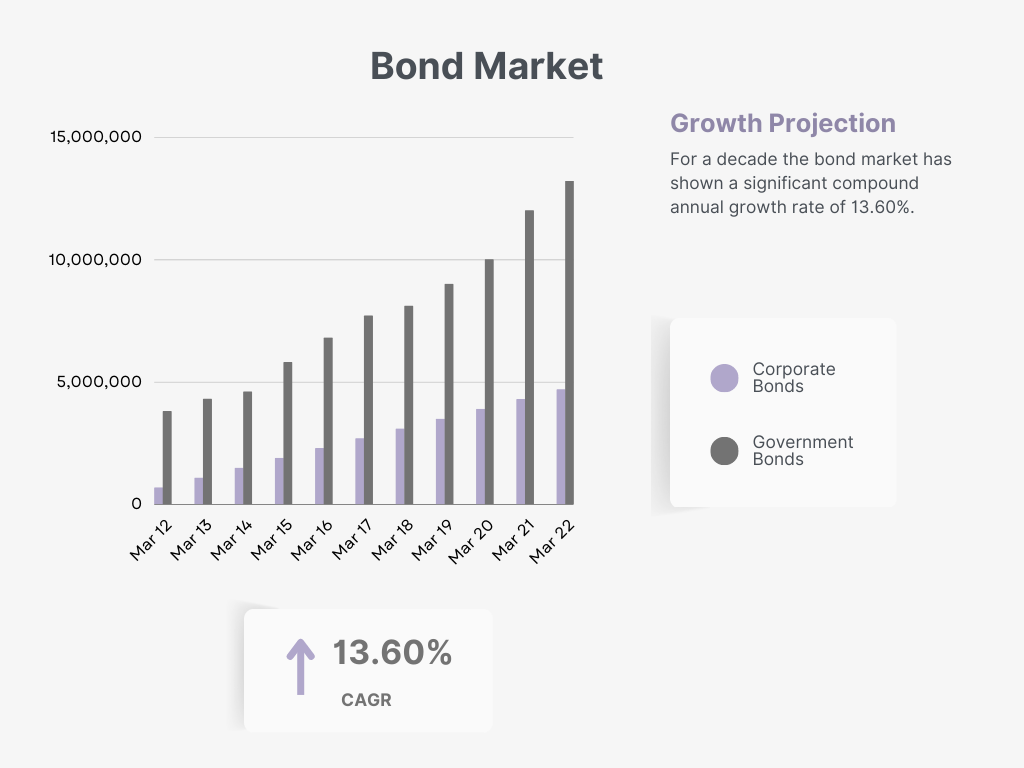

Despite facing challenges, the bond market in India has seen significant growth in the past decade, with a Compounded Annual Growth Rate (CAGR) of 13.60%.

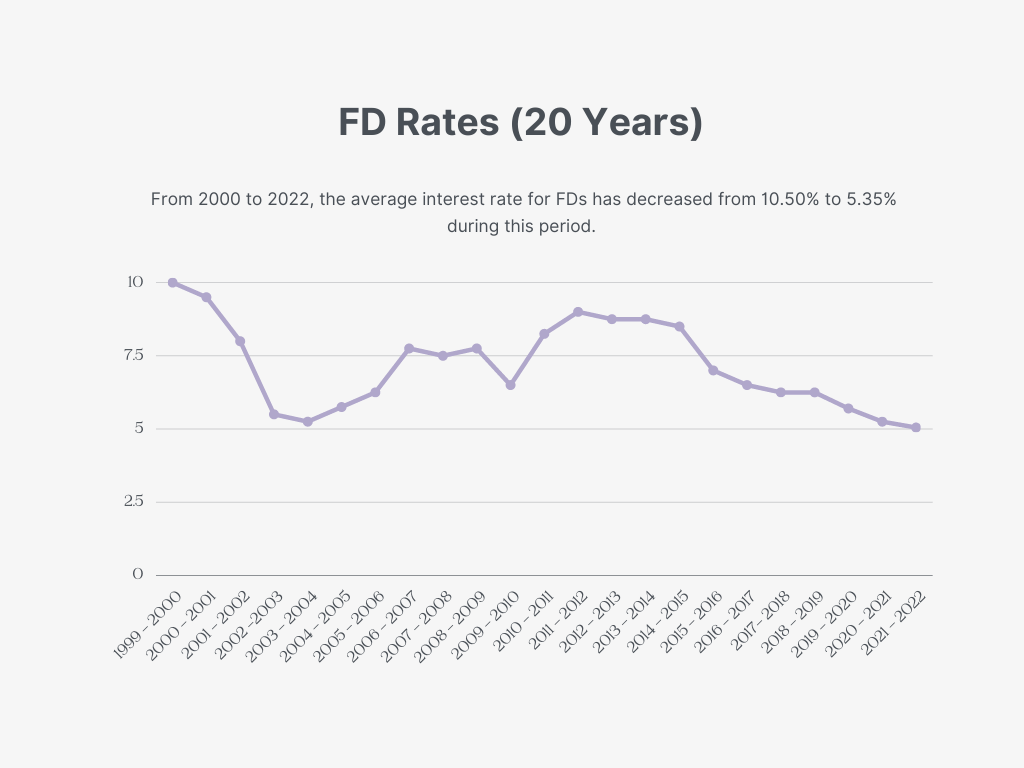

While on the other hand, it is evident from the trendline that the interest rates for fixed deposits in India have dropped significantly over the past two decades, from 2000 to 2022. The average interest rate for FDs has decreased from 10.50% to 5.35% during this period.

Why Switch to Bonds?

There are a few reasons why you might want to consider switching some of your investments to bonds:

- You’re getting older: As you approach retirement age, you may want to shift your focus from growth to preservation of capital. Investing in bonds can help you do this, while still earning a decent return.

- You’re risk-averse: If you’re the type of person who gets anxious about the ups and downs of the stock market, bonds can provide some much-needed stability when compared to stocks, but although it involves some risk.

- You want to balance your portfolio: As mentioned above, adding some bonds to your portfolio can help to diversify your holdings and reduce overall risk. This is especially important if you have a lot of money invested in stocks.

Implication for the Topic at Hand

In conclusion, there are a few reasons why fixed deposit interest rates may be going down. The Reserve Bank of India (RBI) has been cutting its policy rate in order to stimulate economic growth and make it cheaper for banks to borrow money. Weak economic conditions, such as low inflation and weak growth, also make it less likely that interest rates will be high. Additionally, banks may have excess funds available, which can also result in lower interest rates on fixed deposits, as they do not need to attract as much money from customers to meet their funding needs. So, all these factors contribute to the falling fixed deposit rates in India.

Given these factors, it may be worth considering switching to other investment options, such as bonds, as a way to potentially increase your returns. While bonds do come with some level of risk, they can offer a relatively stable and predictable stream of income. They can also be a good option for those who are looking for a lower level of risk compared to stocks.

It’s important to keep in mind that no investment is completely risk-free and it’s always a good idea to diversify your investment portfolio to spread your risk. By considering a mix of different investment options, including fixed deposits, bonds, and other securities, you can potentially increase your overall returns and mitigate risk. So, it is always good to explore other investment options and not rely solely on fixed deposits.

Investment strategies in the bond market

FAQs ON BANK FD

1. What are some alternative investment options to fixed deposits?

Some alternative investment options to fixed deposits include bonds, corporate fixed deposit stocks, mutual funds, and real estate.

2. How do bonds compare to fixed deposits in terms of risk and return?

Bonds generally have a lower risk compared to stocks, but a higher risk compared to fixed deposits. They also offer a higher return compared to fixed deposits but lower than stocks.

3. What are some things to consider when investing in bonds?

When investing in bonds, it is important to consider factors such as the creditworthiness of the issuer, the maturity date, and the bond’s yield.

4. Why are FD interest rates falling?

FD interest rates are falling due to a combination of factors such as policy rate cuts by the Reserve Bank of India, weak economic conditions, and excess funds with banks.