|

Getting your Trinity Audio player ready...

|

India’s cities need a lot of money. Roads, water supply, drainage, public transport, building and maintaining urban infrastructure require consistent, large-scale funding. One of the ways cities raise this money is by issuing municipal bonds.

When a city issues a municipal bond, it borrows from investors and promises to repay with interest. For investors, it’s a way to earn fixed returns. Some of these bonds are also tax-free, which makes them look even more attractive at first glance.

So should retail investors consider them? Here’s what the market actually looks like in 2026.

What Are Municipal Bonds?

Municipal bonds are bonds issued by urban local bodies, or ULBs. This includes municipal corporations, city development authorities, and similar civic entities. SEBI regulates these bonds under the SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

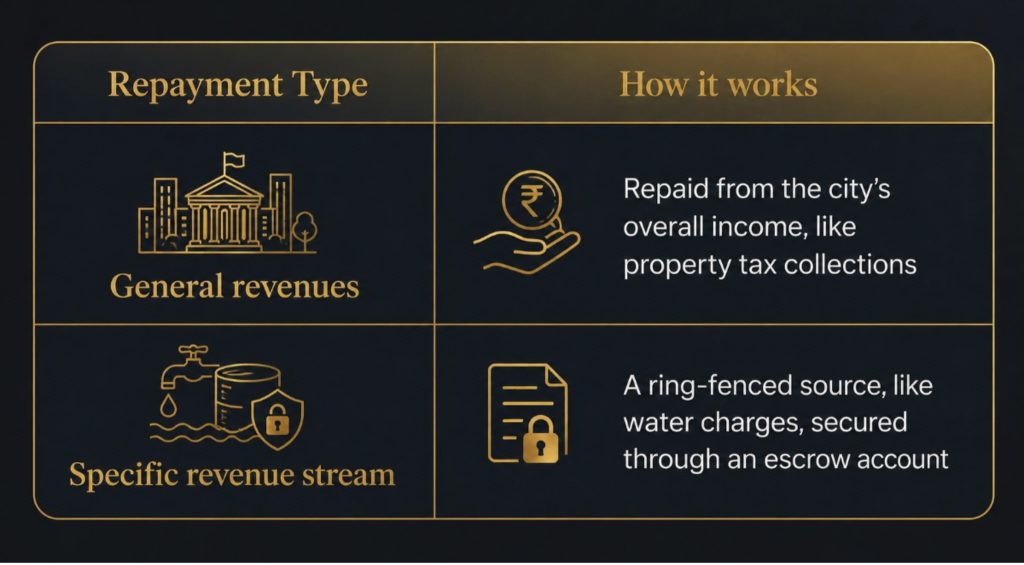

Invest NowHow does repayment work?

When a city issues a municipal bond, it commits to paying interest over the bond’s tenure and returning the full principal at the end. The repayment source is one of two types:

How has the market developed?

- India’s first modern municipal bond was issued by Bengaluru’s BBMP in 1997

- Cities like Pune, Ahmedabad, Hyderabad, and Indore have issued bonds since

- SEBI’s 2015 framework created formal rules covering disclosures, credit ratings and listing

- The Smart Cities Mission gave the market a push from 2018 onwards

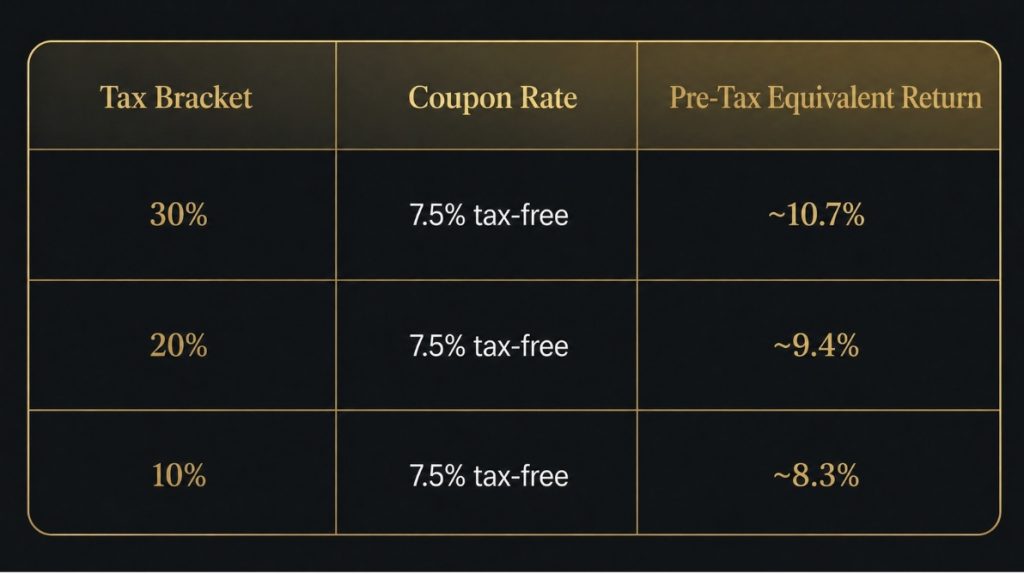

Are Municipal Bonds Tax-Free?

Some are, some aren’t. This is where a lot of investors get confused.

Municipal bonds issued under specific central government notifications are exempt from income tax on coupon income. Here’s what that means in numbers:

What you must verify before investing

- Not all municipal bonds are tax-free. The exemption applies only to bonds issued under specific central government notifications

- Always check the tax status of the specific bond you’re looking at

- If you sell before maturity, capital gains are taxed under standard debt taxation rules, regardless of tax-free status

- The tax exemption covers coupon income only, not secondary market gains

Secondary Market Liquidity for Municipal Bonds

Here’s something that doesn’t get enough attention when municipal bonds are discussed. These bonds are listed on exchanges, but they don’t trade much.

Why the secondary market is thin

- At issuance, most bonds are bought by institutional investors like insurance companies and pension funds

- These investors hold on to their bonds till maturity and do not sell

- This means on most trading days, there is very little activity in municipal bond series on the BSE or the NSE

Related Post

- India in Global Bond Indices: Retail Investor Impact Explained

- How Infrastructure Bonds and InvIT-Linked Debt Work in India

- Bond Investment Strategy by Age: 30s vs 50s Compared

What this means for you

If you invest in a municipal bond and need money before it matures, finding a buyer at a fair price can be very difficult. You might find one eventually, but probably not at the price you’d want.

In practice, you should only invest money in municipal bonds that you are sure you won’t need for the full tenure of the bond.

How Retail Investors Can Access Municipal Bonds

On paper, SEBI’s framework allows retail investors to buy listed municipal bonds. The minimum face value for public issues is Rs. 1,000. But the practical reality is more limited.

Public issues vs. private placements

You can hold municipal bonds in your demat account through NSDL or CDSL if you do manage to access them. But finding them takes more effort than buying a regular NCD from a corporate issuer. They’re not showing up in the “available bonds” section of most retail platforms right now.

What to Know About the Issuer’s Ability to Repay

Many municipal bonds in India carry investment-grade credit ratings. Several are also backed by an escrow over a specific revenue stream. That structure is a genuine protection for investors.

But it’s worth understanding the broader financial condition of Indian cities.

Common financial challenges for Indian ULBs

- Property tax collection rates are low in many cities

- Water and sewerage charges often don’t cover the cost of the service

- Many ULBs rely on grants from the state and central governments to manage day-to-day expenses

- The 15th Finance Commission flagged own-source revenue weakness as an unresolved problem

When a bond’s repayment depends on an escrow over water charge collections, how safe that escrow really is depends on whether the city is actually collecting those charges reliably. In cities where billing systems are outdated or collection is inconsistent, the escrow gives less comfort than it might seem on paper.

So, Are Municipal Bonds Right for Retail Investors Right Now?

The honest answer is: it depends on your situation.

Municipal bonds are a real, regulated investment option. Several cities have issued and repaid bonds cleanly. SEBI’s framework covers disclosure, credit rating requirements, and listing obligations.

A quick checklist before you consider investing

If you can confirm all of these, municipal bonds may be worth looking at. For most retail investors who are newer to the bond market, it may be worth getting comfortable with more accessible bond options first. To make the experience effortless GoldenPi is here at you service

FAQs on Municipal Bonds in India

A: Municipal bonds are bonds issued by urban local bodies like municipal corporations and city development authorities to raise money for infrastructure projects. They’re regulated by SEBI and can be listed on exchanges. Investors earn interest during the tenure and receive their principal back at maturity.

A: No. The tax exemption on coupon income applies only to bonds issued under specific central government notifications. It doesn’t apply to all municipal bonds. Always check the tax status of the specific bond you’re looking at before investing. Capital gains from selling before maturity are taxed under standard debt rules regardless.

A: For publicly issued municipal bonds under SEBI’s framework, the minimum face value is Rs. 1,000. But most municipal bond issuances are private placements with higher minimum ticket sizes, mainly accessible to institutional and high-net-worth investors.

A: Most municipal bonds are bought by institutional investors at issuance and held till maturity. After listing, there’s very little trading activity in the secondary market. If you want to sell before maturity, you may not find a buyer easily, and those available may offer a lower price than you’d expect.

A: The primary difference between the two is what backs repayment. A general obligation bond is backed by the city’s overall revenues and taxing authority. A revenue bond is backed by a specific income stream, like water charges or toll collections, secured through an escrow account. Most municipal bonds issued in India so far have been revenue bonds.

Ready to Invest?

Visit GoldenPi to explore current bond options. Compare yields, ratings, and tenures in one place and invest online with as little as ₹10,000.

Disclaimer:

Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities and municipal debt securities/securitized debt instruments are subject to credit risks, market risks, and default risks, including delay and/or default in payment. Read all the offer-related documents carefully. This blog/article should not be construed as financial advice or as an offer or recommendation to buy or sell any security or any products/services of/on GoldenPi or any product/services of its third-party client(s). For a detailed calculation of YTM, visit our website. T&C’s Apply.