|

Getting your Trinity Audio player ready...

|

What’s Happening in Microfinance Companies? Should You Be Investing?

The microfinance sector in India, once hailed as the silver bullet for financial inclusion, is at a critical juncture. With over ₹3.6 lakh crore in gross loan portfolio and 6.5 crore active borrowers (as of March 2025, MFIN Micrometer), microfinance institutions (MFIs) are deeply entrenched in India’s socio-economic fabric. But rising borrower distress, tighter regulation, and investor anxiety have cast a long shadow on this once-flourishing sector.

So, should you invest in microfinance-linked debt instruments in 2025? Is the model still robust, or is it straining under its own weight?

Let’s break it down.

What Are Microfinance Institutions (MFIs)?

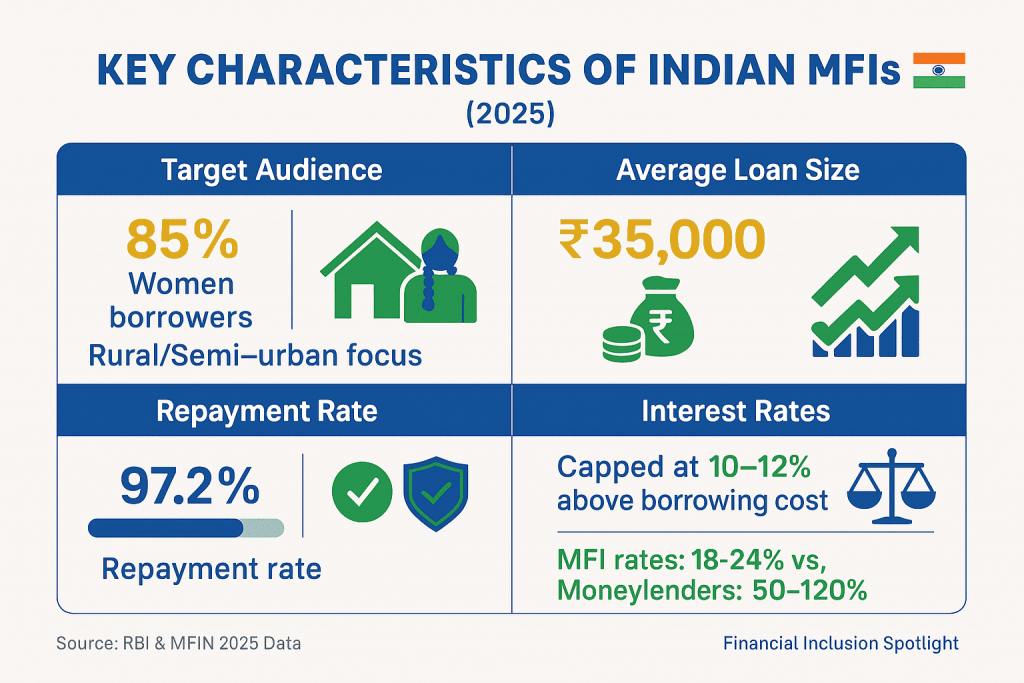

MFIs are financial entities that provide small-ticket loans (typically between ₹10,000 and ₹75,000) to low-income individuals and households, primarily in rural and semi-urban India. Around 97% of MFI borrowers are women, according to Sa-Dhan data, and the loans often support home-run businesses, farming, or working capital for petty shops.

In regions where formal banking channels fail to reach, MFIs serve as a lifeline. They help with:

- Enabling credit access for the unbanked

- Fostering self-employment and rural entrepreneurship

- Reducing dependence on moneylenders

- Promoting financial discipline and credit culture

How Does the MFI Business Model Work?

- MFIs raise capital through:

- Equity investments

- Bank borrowings (typically under Priority Sector Lending norms)

- Non-convertible debentures (NCDs)

- Securitization of their loan portfolios

They disburse loans with minimal paperwork and no collateral, often through group-lending models like Joint Liability Groups (JLGs). Collections are made weekly or monthly, with field officers physically visiting borrowers.

Typical interest rates: 18%-24% per annum

Average ticket size: ₹22,000-₹26,000

Repayment cycle: Weekly/bi-weekly/monthly

The business model hinges on scale – high disbursement volumes, peer pressure in groups, and strict repayment monitoring. However, in an environment of macro stress and loose underwriting, this model can quickly unravel.

Cracks in the System: What’s Going Wrong in 2024-2025?

While MFIs have grown rapidly post-COVID, the growth has not been without risks. Key challenges include:

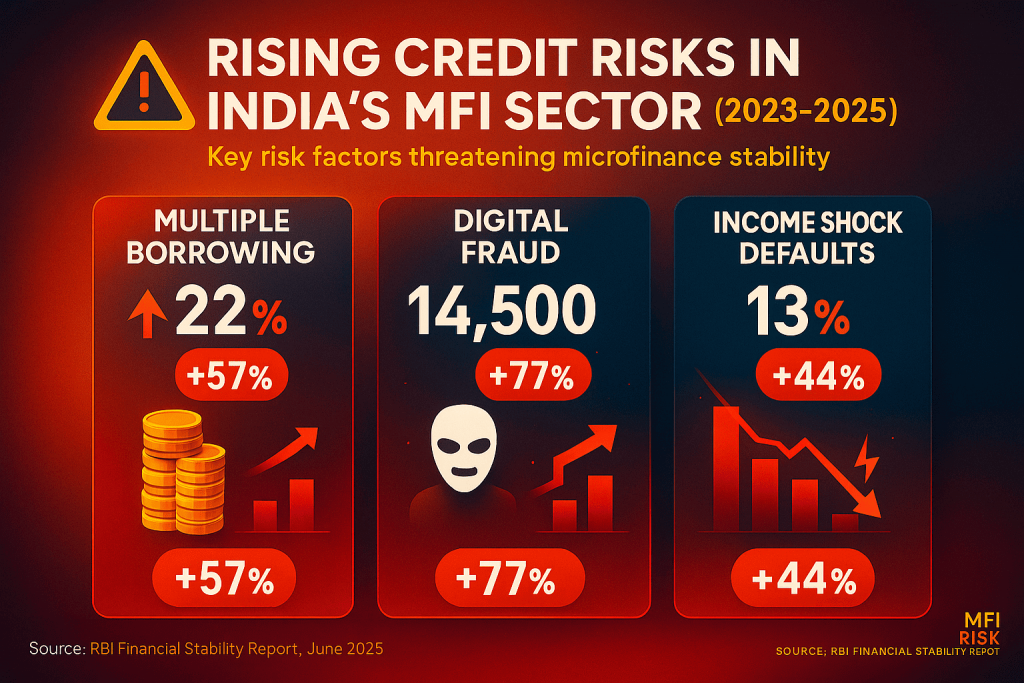

1. Over-Indebtedness

Borrowers now often juggle loans from 4-5 lenders. The Reserve Bank of India (RBI) has capped total loan repayment obligation to 50% of household income – but enforcement is tricky. According to CRIF High Mark, over 22% of MFI borrowers in Tamil Nadu and West Bengal hold four or more active loans.

2. Loan Quality Concerns

Rising default levels are worrying. As of Q4 FY2025:

- PAR30+ (Portfolio at Risk beyond 30 days) stood at 8.1% for smaller NBFC-MFIs (source: MFIN).

- GNPA (Gross Non-Performing Assets) exceeded 5% for 18% of MFIs.

The problem is worse in states like Assam, where socio-political instability has disrupted repayment cycles.

3. Aggressive Lending and Weak Appraisal

Some MFIs have expanded without proper credit assessment. Digital loan disbursals -though efficient – often miss field-level verification, resulting in “ghost lending” or loans disbursed to proxy borrowers.

4. Recovery Tactics and Reputational Risk

Incidents of coercive recovery – including threats, public shaming, and harassment – have come under scrutiny. While not widespread, such practices can erode trust and invite regulatory backlash.

What Is the RBI’s View?

The Reserve Bank of India, alarmed by the sector’s drift, is actively reining it in. In a March 2024 policy address, Deputy Governor M. Rajeshwar Rao cautioned against a “profit-over-purpose” model taking root in MFIs. His concerns were echoed in the RBI’s 2024 Financial Stability Report.

RBI’s Key Concerns:

- Misalignment of social mission with commercial expansion

- Weak grievance redressal mechanisms

- Margin expansion despite low borrowing costs

- Overdependence on digital KYC and algorithmic lending

Regulatory Actions So Far:

- Implementation of Uniform Regulatory Framework for all REs offering microfinance loans.

- Tightening of loan origination norms: Cap on borrower indebtedness and stricter documentation.

- Push for risk-based pricing: MFIs must now explain their spreads transparently.

Already Invested in MFI Instruments? What Should You Do?

Many investors hold MFI exposure through NCDs or securitized instruments. Here’s what you should review in 2025:

Credit Ratings:

Look for recent downgrades or outlook changes. Even AAA ratings should be reviewed with scrutiny.

GNPA/PAR Metrics:

Avoid institutions with a GNPA over 4% or PAR 30+ above 8%.

Capital Adequacy:

A healthy CRAR (Capital to Risk-weighted Assets Ratio) of over 18% is preferable.

Collection Efficiency:

Steady monthly collections above 96% signal borrower stability.

If your investment is nearing maturity and there are signs of stress, consider an early exit – provided there’s sufficient liquidity in the secondary market.

here’s no denying that the social value of microfinance remains intact. The demand is real, and India’s financial inclusion agenda is far from over. But as an investor, you need to pick your spots wisely.

Here’s how to evaluate:

Choose Responsible Lenders

Look for:

- Transparent interest disclosures

- Solid grievance redressal

- Diversified geography (avoid high saturation regions like Tamil Nadu, Assam)

Read the Fine Print

- Is the instrument secured or unsecured?

- What are the default triggers?

- How diversified is the underlying loan pool?

Stay Updated

- Follow MFIN, CRISIL, RBI publications

- Watch state-specific borrower trends – repayment behavior is increasingly localised

Diversify

Limit MFI exposure to no more than 10-15% of your debt portfolio. Combine it with government bonds, blue-chip NCDs, and structured debt.

Final Word: Risk and Purpose Must Be Balanced

Microfinance is not a sector you can blindly trust – nor should you write it off entirely.

The growth story remains compelling, but risk governance is becoming the make-or-break factor. As a socially meaningful but commercially complex space, MFIs demand an investor approach that is informed, measured, and selective.

In 2025, investing in microfinance isn’t about chasing high yields. It’s about backing the right institutions, with clear models, ethical practices, and strong risk buffers.