")

1.What is the difference between bonds & debentures?

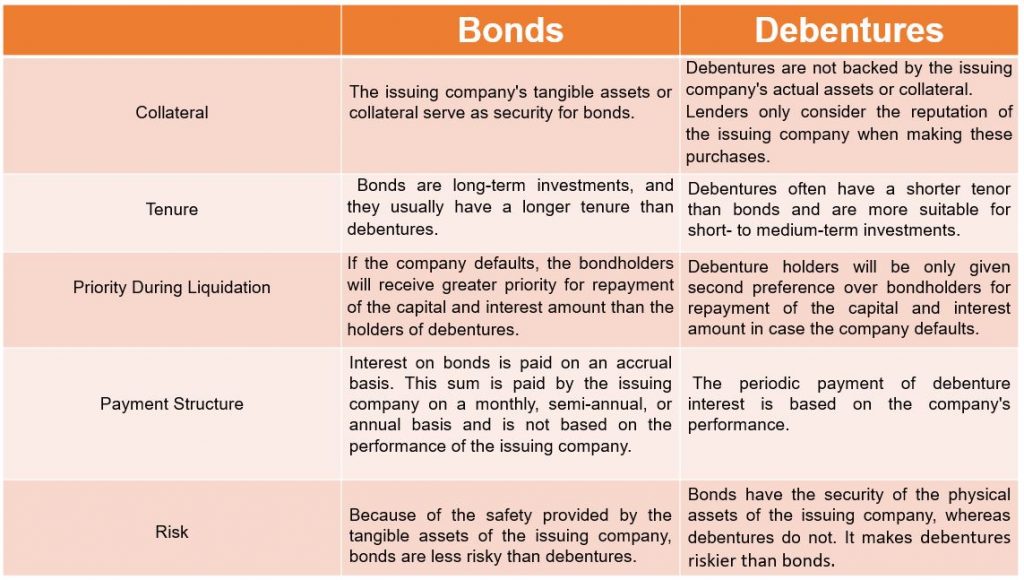

Bonds

Most corporates, governmental organisations, and other financial institutions use bonds as their primary form of debt financing. In essence, bonds are loans with a physical object as collateral. The bond issuer becomes the borrower, and the bond’s holder becomes the lender. With the assurance of repayment at the designated maturity date, the bondholder, or lender, lends money to the borrower. For the course of the bond’s tenure, the lender often also gets paid a fixed rate of interest.

Debentures

Bonds and debentures both belong to the debt category. These tools help organisations obtain the cash they need to meet their everyday expenses. They carry a higher level of risk than bonds because they typically are not backed by any real property of the issuers. They also have an interest rate, which may be fixed or variable. When it comes to the distribution of dividends and interest, debenture holders are given priority over shareholders of the company. Given that they are not backed by a company’s tangible assets; debentures typically have higher interest rates than bonds.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest Now2.What is senior and subordinate bonds? Please elaborate more

Senior Bond Holders

Senior debt or senior bondholders are the one given high priority if the bond issuer or the company files bankrupt or get defaults. For example: Invest ABC holds a Senior bond Rs. 1000 from XYZ company with 10 % coupon rate and 10-year tenure. In-case the due to various reasons the XYZ company has filed bankrupt or defaulted, then the company’s assets will be sold and the senior debt (bondholders) will be paid first before anybody else.

Therefore, senior debt is considered a safer option than the subordinate debt .

Subordinate Bonds

Subordinate debt or Junior bondholders are the one given second priority after the senior debt holder if the bond issuer or the company files bankrupt or get defaults

For example: Invest ABC holds a Subordinate debt Rs. 1000 from XYZ company with 10 % coupon rate and 10-year tenure. In-case the due to various reasons the XYZ company has filed bankrupt or defaulted, then the company’s assets will be sold and It will be given to

the senior debt (bondholders) will be paid first before and then will be given to subordinate debt.

In case if the fund was not sufficient after paying to the senior debt then subordinate debt won’t receive anything.

3. Can you please explain interest risk with example?

Bond’s price fluctuates along with market interest rates; an investor is exposed to the risk that a bond’s price will decrease if those rates increase. The most frequent danger experienced by bond investors.

Example: An invest holds bond Rs. 1000 with coupon rate of 5% and 5-year tenure. In the second year of the bond tenure, the bond issuer issues the same bond with higher coupon as in 7%. Now the previous bond holder will be sell the bond in discounted price in order to get the new issuer with higher coupon rate.

4.What is the difference between coupon rate and yield rate?

Coupon rate

The rate at which a bond’s investor receives interest payments is known as the coupon rate. It is a percentage that represents the annual interest rate that the bond pays in relation to its face value. The coupon rate is comparable to fixed-income government and corporate bonds, in which the bond’s issuer receives yearly interest payments.

For example: If a bond has a face value of Rs. 10000, a coupon rate of 10%, an annual payment schedule, and a maturity period of 5 years, the investor will receive Rs. 1000 each year until the bond matures. Similar to when we obtain a loan from a bank, the interest we may be required to pay the bank on a monthly basis is referred to as the coupon rate in the bond market.

Yield Rate

A bond’s yield is the annual interest payment it makes as a proportion of its market value. Although it may appear to be the same as the coupon rate, it is not. The yield would fluctuate inversely with the bond’s market price.

Difference between Coupon Rate and Yield to Maturity?

5.Taxation on Bond Investment

Generally, Bond investment’s interest income is under taxable, it depends on the tax slab rate.

It can go up to 30 % maximum. If it is listed bond and the holder holds it more than 12 months – the interest income will be taxed at 12.5%

For the unlisted bonds, if the investor holds the bond more than 24 months – then the interest income will be taxed at 12.5%

In both the bond case, the short term capital gain tax will be as per applicable slab rates

Indian tax slab if anyone’s annual income is more than 5.5 lakh, it comes under various tax slabs.

ABC investor has invested Rs. 10 lakhs in listed bonds. The coupon rate, i.e., interest rate, is 10% paid annually. ABC annual income is 9 lakh. So, ABC comes under the 20% slab rate.

Investment amount – 10,00,000

Coupon rate -10%

Annual Interest income – 1,00,000

Tax on interest income:

Tax – 20%X 1,00,000

Tax- 20,000

ABC has to pay Rs. 20,000 tax on interest income every year till maturity or till he resells bonds.

STCG

After 10 months, if ABC sells bonds for Rs.10,50,000, then the capital appreciation is Rs.50,000

Tax- 20% X 50,000

Tax – 10,000

ABC has to pay Rs.10,000 as Short Term Capital Gain Tax.

LTCG

After three years, if ABC sells bonds for Rs. 13,00,000, then the capital appreciation is Rs. 3, 00, 000.

Tax – 10% X 3,00,000

Tax- 30,000

ABC has to pay Rs. 30,000 as Long term Capital Gain Tax

6.How will I understand shut period?

A “shut period” is the time frame during which securities cannot be delivered. There will be no settlements or deliveries of the security that is under shut during that time. The major goal of having a shut period is to make it easier to service the securities, which includes finishing the payment of the coupon and the revenues from redemption, and to prevent any change in ownership of securities while doing so. The closure time for stocks stored in SGL accounts is currently one day.

In the delivery versus payment (DvP) method of settlement, both the securities and the money are transferred at the same time. As a result, it is guaranteed that neither the securities nor the funds will be provided unless the funds are paid. Transactional settlement risk is eliminated by the DvP settlement. There are three different DvP settlement types, which are DvP I, DvP II, and DvP III.

DvP I

The securities and funds legs of the transactions are settled on a gross basis, meaning that the participant’s payables and receivables are not netted off as they are settled transaction by transaction.

Dvp II

Here, the fund is settled on a net basis whereas the securities are settled on a gross basis. This means, the payable and receivable of the entire transactions of a part are netted to arrive at the final destination of payable or receivable, which is then settled.

Dvp III

Only the final net position of all transactions made by a participant is settled, and both the securities and funds legs are settled on a net basis.

Since the payables and receivables are offset against one other in the net mode, the liquidity need in a gross mode is higher than that in a net mode.

7. Top three things to consider while buying a bond?

Bond Price and Maturity

- Need to verify that whether the bond is being sold at par or discounted or high price.

- Tenure of the bond.

Coupon Rate

- Is the coupon rate better than FD?

- How much difference between FD and the current coupon rate?

Yield

- Investor has to differentiate between coupon rate and yield to maturity.

Credit rating

- Rating would give an idea security of the bonds.

- The bonds can fall under AAA, AA, A or BBB rated bonds.

What’s a corporate bond? How to select one.

Disclaimer:

This information is for general information purposes only. GoldenPi makes no guarantee on the accuracy of the data provided here; the information displayed is subject to change and is provided on an as-is basis. Nothing contained herein is intended to or shall be deemed to be investment advice, implied or otherwise. Investments in the securities market are subject to market risks. Read all the offer-related documents carefully before investing.

Bonds or non-convertible debentures (NCDs) are regulated by the Securities and Exchange Board of India and other government authorities. GoldenPi Securities Private Limited is a registered debt broker and acts as a distributor and not as a manufacturer of the product.

2 comments

Very well explained. Thanks a lot.

KNOWLEDGEABLE ARTICLE

Comments are closed.