1. Please let us know about the taxation on income earned through Bonds etc.

Taxation

Generally, a Bond investment’s interest income is under-taxable, it depends on the tax slab rate. It can go up to 30 % maximum.

In case it is a listed bond and the holder holds it for more than 12 months – the interest income will be taxed at 10%. For the unlisted bonds, if the investor holds the bond for more than 36 months – then the interest income will be taxed at 10%.

In both the bond case, the short-term capital gain tax will be 5 to 3%.

Indian tax slab if anyone’s annual income is more than 5.5 lakh, it comes under various tax slabs.

ABC investor has invested Rs. 10 lakhs in listed bonds. The coupon rate, i.e., interest rate, is 10% paid annually. ABC annual income is 9 lakh. So, ABC comes under the 20% slab rate.

Investment amount – 10,00,000

Coupon rate -10%

Annual Interest income – 1,00,000

Tax on Interest Income:

Tax – 20%X 1,00,000

Tax- 20,000

ABC has to pay Rs. 20,000 tax on interest income every year till maturity or till he resells bonds.

STCG:

After 10 months, if ABC sells bonds for Rs.10,50,000, then the capital appreciation is Rs.50,000

Tax- 20% X 50,000

Tax – 10,000

ABC has to pay Rs.10,000 as Short Term Capital Gain Tax.

LTCG:

After three years, if ABC sells bonds for Rs. 13,00,000, then the capital appreciation is Rs. 3, 00, 000.

Tax – 10% X 3,00,000

Tax- 30,000

ABC has to pay Rs. 30,000 as Long term Capital Gain Tax.

What are Tax Free Bonds?

2. Is there a convertible debenture i.e. can be converted to equity?

Convertible Bonds

For example, 1 stock can be R. 40

A convertible bond gives the right to the bondholder to convert the bonds into stock and become part of the company, then receive a dividend. During the conversion, the bondholder will receive a lower yield than other bonds. The bond’s stock price will be dedicated during the purchase. 1 stock = Rs. 40.

Example: A bondholder has a bond of Rs. 1000, a coupon rate -of 10%, and a Tenure of -10 years.

After two years, the bondholder decides to convert the bonds to stock.

= Bond price / Stock price

Then the bondholder will receive 25 stocks for the bond and will not have any assured return as fixed.

Non- Convertible Bonds

A non-convertible fall under the debt category, bondholders do not have rights to the bond to convert the bonds into either equity or stock. The non-convertible bond holder can receive fixed returns based on its coupon rate for its said tenure.

Example. A bondholder has a bond of Rs. 1000, a coupon rate -of 10%, and a Tenure of -10 years.

Here the bondholder will receive Rs.100 interest every year till maturity.

3. What is a Subordinate Bond?

Subordinate debt or Junior bondholders are the ones given second priority after the senior debt holder if the bond issuer or the company files bankruptcy or gets defaults.

For example: Invest ABC holds a Subordinate debt of Rs. 1000 from XYZ company with a 10 % coupon rate and 10-year tenure. In case due to various reasons the XYZ company has filed bankruptcy or defaulted, then the company’s assets will be sold and It will be given to the senior debt (bondholders) will be paid first before and then will be given to subordinate debt.

In case the fund was not sufficient after paying the senior debt and subordinated debt won’t receive anything.

4. What are Coupon Rates and Yield To Maturity (YTM)?

Coupon Rate

The rate at which a bond’s investor receives interest payments is known as the coupon rate. It is a percentage that represents the annual interest rate that the bond pays in relation to its face value. The coupon rate is comparable to fixed-income government and corporate bonds, in which the bond’s issuer receives yearly interest payments.

Yield To Maturity

The return rate that investors receive while holding the bond until it matures is known as yield to maturity. The yield to maturity (YTM) figure includes interest received on interest and includes all interest payments made from the day of purchase until maturity.

What is the difference between Yield to Maturity vs Coupon Rate?

5. How safe is an investment in NCD IPO?

The company uses fixed-term instruments to raise money in the form of loans from the public at a predetermined rate of return. These are known as Non-Convertible Debentures as these cannot be converted into shares. They are of 2 types.

1. Secured NCDs

This tranch of NCD is basically secured by the assets of the company. Therefore, in case the company is unable to pay back its borrowers, the assets could be liquidated and the amount derived by it could be utilized to pay back the company borrowers.

2. Unsecured NCDs

These are not secured against the assets of the company. Hence, they are riskier and offer higher yields when compared with the secured NCDs, to compensate for the risk borne by the borrowers.

It entirely depends on the kind of NCDs you are investing in. Both types have their own risk and advantages.

What is the Difference between Equity IPO and NCD IPO?

6. Can a company recall/buy back its NCD Bond in the middle when it can raise capital for less interest?

The corporate bonds do not have an option either to call back or raise the price of the existing bonds before their maturity. Nevertheless, government issues call back or put option bonds during its emergency in order to raise funds for various projects.

Bonds with Call or Put Option

These bonds include a call option that gives the issuer the opportunity to repurchase the bond or a sell option that gives the investor the option to sell the bond to the issuer (put option). Only five years after the date of issue will the investor or issuer be able to exercise their rights.

Example:

Bond Price – Rs. 1000

Tenure – 10 years

Government can buy back the same bond at the same price of Rs. after the completion of 5 years before the maturity period (10 years). If only the government wants to re-purchase the bond.

In the same way, the investors can sell the bond to the government at the same price which they had purchased five years before.

7. What are the risk factors in these bonds? Can you explain?

Interest Rate Risk:

A Bond’s price fluctuates along with market interest rates; an investor is exposed to the risk that a bond’s price will decrease if those rates increase. The most frequent danger experienced by bond investors.

Example: An investor holds a bond of Rs. 1000 with a coupon rate of 5% and a 5-year tenure. In the second year of the bond tenure, the bond issuer issues the same bond with the higher coupon as in 7%. Now the previous bondholder will be tempted to sell the bond at a discounted price in order to get the new issuer with a higher coupon rate.

Credit Risk:

Investors will be exposed to credit risk if interest payments are not made on time by the bond issuers. Those who invest in secured and better crediting rating bonds experience less credit risk. Whereas, whoever invested in unsecured or negative credit rating bonds would likely experience credit rating risks.

Liquidity Risk:

Two scenarios are possible.

Bondholders could not be able to sell their bonds before the due date because a buyer might not be accessible, another scenario is bond issuers may find it challenging to sell their assets in the market.

Call Risk:

It only happens to the callable bonds which allow the bond issuer to buy back the bond before the maturity date. It depends on the issuers’ financial condition whether to buy back or not. Such bonds always come with risks.

How does Inflation affect Bond Price?

8. Please talk about secondary market Bonds

The secondary market is centered around trading securities that are already listed and cannot trade the securities. The investors trade amongst themselves and there is no direct cash flow to the companies

9. What are listed bonds?

A listed bond is listed on exchanges that are openly tradable on NSE or BSE stock exchanges. Examples: HDFC Bank, and Indian Oil Corporation.

10. What are Unlisted bonds?

The bonds are issued by companies that are not traded in an official stock exchange. Trading of the securities is done over the counters. Muthoot Fincorp Limited. The dealers facilitate the buying and selling of the unlisted bonds

Even Listed companies also issue unlisted bonds based on their requirements which will not be traded on an official stock exchange.

Example: CHOLAMANDALAM INVESTMENT AND FIN. CO. LTD

11. What are the Tier 1 and Tier2 Bonds?

Tier I

Additional tier 1 bonds are a type of Unsecured, Perpetual Bonds that the Banks Issue to shore up their Core capital base to meet the Basel III Compliance.

These Bonds are riskier and can be written off by RBI.

Tier II

As per BASEL III norms, Banks raise money via Tier II bonds to meet regulatory norms around capital adequacy. Tier II bonds are subordinated debt and hence not first to be paid during the liquidation process. Tier II bonds are senior to Tier I Bonds.

Example: If XYZ bank raises funds through Tie 1 and Tie 2 bonds and the banks go into default, both the bondholder will not be guaranteed either interest payment or principal returns.

12. What happens to my bonds if GoldenPi goes out of business?

Rest assured that your investment is safe. GoldenPi is only an enabler of transactions in bonds. Even in the unlikely case of us shutting down in the future due to some unforeseen circumstances, your investments will remain intact. You will continue to hold your Bond units in your Demat account and receive the Bonds’ regular interest payouts into your Bank Account. On maturity, the Bond’s face value will be credited to your bank account, as well.

13. How to close NCD before maturity?

NCD IPOs can not be closed before their maturity instead, the holder can sell/trade in the secondary market based on the market conditions, and you can receive a capital gain.

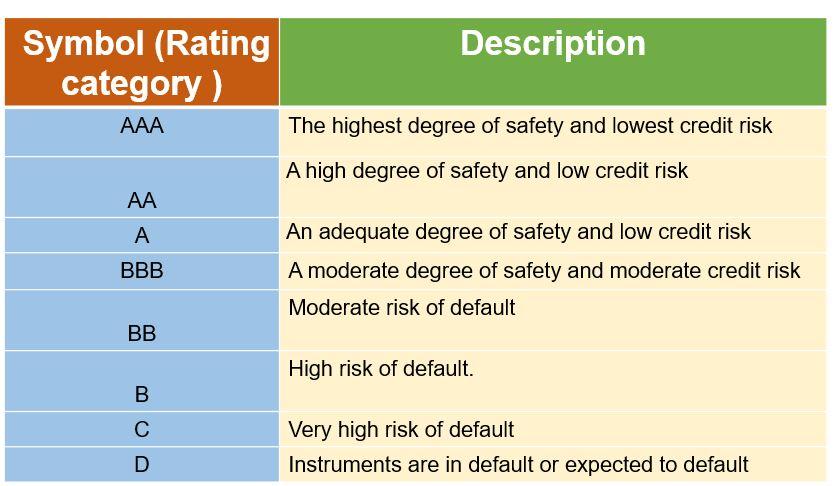

14. How safe are bonds rated A, A-for example U-Gro?

Purpose of Credit

The investor will be completely aware of the bond issuers and their financial or business capacity while they are issuing bonds. Therefore, credit agencies will issue the real condition of the bond issuers based on various parameters of calculations which would enable the investor to arrive at a conclusion about whether to invest in the particular corporate bonds or not.

15. What is the risk associated with Unsecured debentures?

Unsecured bonds by their very nature incur more risk than secured bonds; as a result, they typically have higher interest rates. When a firm that issues debentures liquidate, it pays secured bondholders, debenture holders, and owners of subordinated debentures in that order.

16. Difference between Bond and NCD

A bond serves as collateral for a secured investment. Here, a resource is pledged. Therefore, Bond owners can sell the asset and recoup their investment money if the issuer fails to pay the debt. CDs, on the other hand, are typically unsecured. Debentures are backed by no assets, therefore picking a reputable company is crucial when investing in them.