It shouldn’t be a surprise for you to find out that Indians love Fixed Deposits. In fact, Fixed Deposits are the most widely used financial savings medium that has been and still is used by all traditional Indians. Whatever the reason for saving the capital, FDs simplify the process of reaching a financial milestone. For instance, if anyone is saving for a dream car, home, wedding, or vacation, having a fixed deposit for a particular reason helps to keep one’s financial interest aligned with one’s financial goals.

The Concept of Fixed Deposit

Most people make an assumption that Fixed Deposits mean stacking a big chunk of capital at a PSU where these banks pay a fixed rate of interest toward the capital. The capital gains that shall be incurred on the deposit are equivalent to whatever interest rate has been agreed to during the initial deposit period. The gained interest is payable monthly, quarterly, or annually depending on the needs of the depositor. If you have a fixed financial goal in mind and are not using the FD as a fixed source of income that it can actually be used for, then the amount can be withdrawn as a lump sum at maturity. This has the advantage of compounding as the interest earned on the capital the previous year is added to the principal amount the next year.

Sovereign Gold Bond and Digital Gold

What kind of Fixed Deposits are available?

FDs can be made at banks and most PSUs which are government-owned banks and NBFCs which are non-bank financial institutions/companies. Both these mediums are excellent for anyone willing to make fixed returns on their investable capital. The interest rates that can be received can be checked and the total amount that will be received upon investment will be calculable even before the investments are made.

Senior citizens can avail higher interests on the Fixed Deposits in both these mediums which makes FDs attractive for retirement. Fixed Deposits also act as a source of income and suit best for people who need fixed monthly income as well. The PSU-owned Fixed Deposits are highly trustworthy and are insured by the DICGC up to half a million rupees (Rs 5,00,000). However, the Corporates that take public money are highly scrutinized as there are extremely cautious rules and regulations in place for a Corporate entity in order to be eligible to offer Fixed Deposits. Even though there are 10,000 such institutions, hardly a few are eligible for offering FD schemes to the general public. It is advised that anyone willing to make investments in such companies make their own due diligence which includes checking the track record of such institutions and also closely observing their financials such that the pledged investments are safe against company defaulting, as such a scenario is NOT insured by DICGC.

However, there are agencies that rate these companies by taking into account all the financial state parameters, thereby making it easier for the general public to make decisions. It is still mandatory to closely track these companies for negative advancements with respect to financial conditions as the invested capital is not insured but the penalty period is generally lesser than for PSU based FDs owing to such instabilities. In fact, this is what makes corporate FDs lucrative for an informed investor.

What is a Corporate Fixed Deposit?

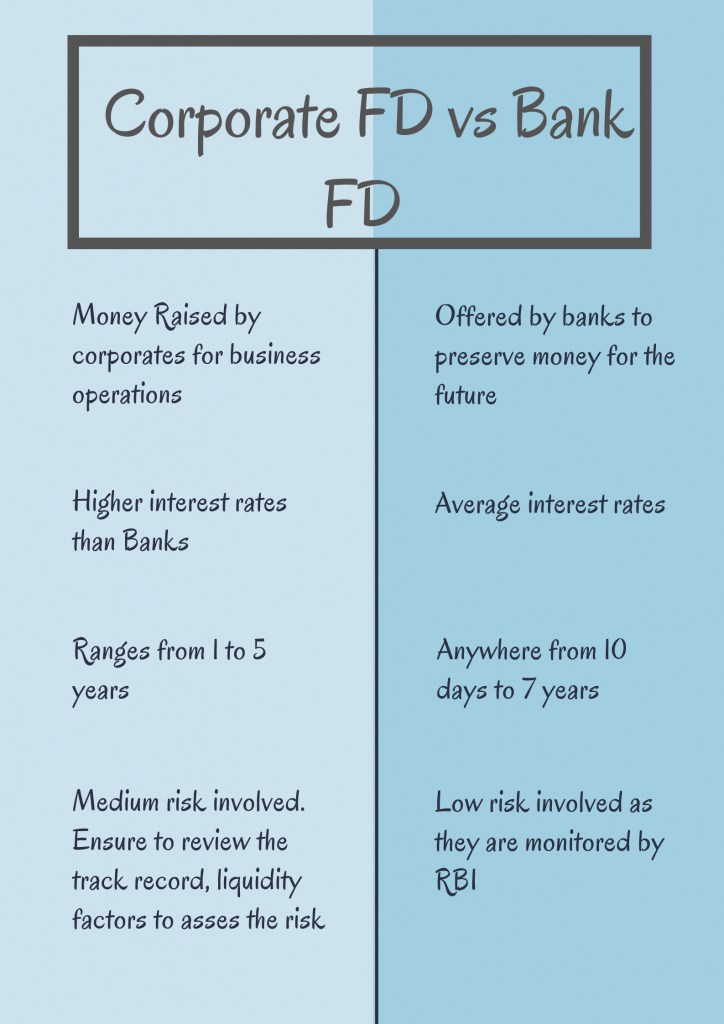

“A corporate fixed deposit (FD) is a financial instrument provided by corporates that provide investors with a higher rate of interest than a bank fixed deposit, until the given maturity date.”

Why should you choose to invest in Corporate Fixed Deposits?

One of the main benefits of making an investment offered by Corporate is the return rate of interest. Typically, these companies are raising capital from the general public for use in company growth and the certainty of growth is reflected in the higher interest that is offered to the depositor. Given strong financial stability and proper financial plan from the company, it is only logical that the institution itself will use the capital to expand its operations which implies a bigger company, higher revenue, and a higher cash flow for the company in the short term projections.

From the company standpoint, the offering is similar to offering an IPO for investors, but the major difference is that the growth of the company would not result in the dilution of promoter shares and the pledged amount by the investors will not be tied to the exact current financials of the company. As the company itself will be strong, that is, the minimum size of the company should be greater than 5000 crores to even offer the FD scheme, the company will pay the fixed interests that it owes to the depositors from the company financials and not exactly from the venture. For whatever reason, if the company/institution is not at all doing well, then as a depositor, there’s always an option to withdraw from the FD scheme.

As long as the depositor is well-informed with respect to the company financials and will be on top of the general whereabouts of the institution in which one is invested, safety concerns can be kept at bay. The lucrative interest rates that the depositor is entitled to can be easily used to attain one’s own financial goals.

When it’s clear to be assured of higher interest rates through Corporate Fixed Deposit, on the other hand, it is noteworthy to consider the penalty period for early withdrawal. Usually, for withdrawing money early any time before maturity from a Bank Fixed Deposit the investor has to pay a penalty whereas for the Corporate Fixed Deposit, the penalty period is three months. Investments withdrawn before three months will only be penalized and not after that.

Who should invest in Corporate FD?

A corporate FD can complement any investor’s needs with premature withdrawal unlike the FD that locks your investment, but the point to note is that only some corporate FDs allow such a withdrawal with minimal conditions.

By parking your investment in the corporate FD, you can choose intervals like monthly, quarterly, semi-annually, and annually for receiving the interest payments that meet your changing needs.

An investor should check the credit rating before investing in high-returning CFD as the lower rating increases the risk. That way a higher return and a good-rated corporate FDs are most beneficial over the higher return low-rated corporate FDs.

But if you have a higher risk appetite, investing in a Corporate FD can still be an option, if you can diversify your investment in other Corporate FD that have higher than normal returns compared to a bank FD and a good credit rating such as AAA.

Why do corporates need your deposits?

Just like how banks operate, corporates create a revenue flow by making reinvestments. More specifically, the core difference in the operation of the corporates is the fact that the corporates operate specifically to a segment. There are companies that invest in real estate, tourism, etc. The companies bank on the growth projection of an entire industry and make smart bets on the expansion of industry-leading companies and industry-redefining companies that require capital injection for company growth. The corporates provide this capital at a higher interest rate and earn via the net interest difference. There are other sources as well that are non-interest related such as loan-processing fees but the major source is interest-based revenue. If the entire portfolio owned by the corporate returns greater yields, it implies higher liquidity and asset appreciation for the corporate. Having now known the way these companies/institutions work, you can better understand the risks as well as the opportunities associated with being involved in an FD scheme offered by NBFCs.

Types of Government Bonds

Benefits of Corporate FD

1. Assured Returns

Feature: Corporate FDs offer fixed interest rates.

Benefit: Investors can rely on stable and assured returns, unaffected by market fluctuations, facilitating effective investment planning.

2. Higher Interest Rates

Feature: Corporate FDs often provide comparatively higher interest rates.

Benefit: Investors can earn better returns than traditional bank FDs, making Corporate FDs an attractive choice.

3. Flexibility of Tenure

Feature: Corporate FDs offer flexibility in choosing the investment tenure.

Benefit: Investors can align the tenure with their financial goals and preferences, with the option for customizing the investment period.

4. Premature Withdrawal

Feature: Many Corporate FDs allow for premature withdrawal with fewer conditions.

Benefit: Investors have the flexibility to access their funds when needed, making these FDs more liquid compared to other locked-in investments.

5. Rated by Credit Rating Agencies

Feature: NBFCs offering Corporate FDs are rated by credit rating agencies.

Benefit: This rating system helps investors assess and select options based on their risk tolerance and investment objectives.

6. Loans on FD

Feature: Corporate FDs may offer loans of up to 75% of the FD value.

Benefit: Investors can access funds through loans against their FDs, providing liquidity and financial flexibility.

Tax implication on CFD

As per the Income Tax Act, it mandates that if your corporate FD interest in a year exceeds Rs. 5,000, Tax Deducted at Source (TDS) will be deducted.

So the interest is considered as the income from other sources and is taxed according to the tax slab you come under. Suppose you fall under the 10% tax bracket, 10% tax is applicable on the interest income.

If you’re in the zero or NIL tax bracket, you must submit Form 15H annually to prevent TDS deductions.

How do I build trust and ensure safety for my investment?

Fundamentally, only large-cap corporates that have a strong history are eligible to create an FD scheme. There are credit rating agencies such as CRISIL, ICRA, and CARE which rate all the companies that are offering corporate FDs. The financials of such companies can be checked and studied by using various metrics such as CAGR (Compounded Annual Growth Rate), PEG Ratio (Price Earnings to Growth Ratio), Quality of assets owned by the Corporate, Revenue Statements, Profitability, etc. A deeper insight into the specific company that you want to deposit in ensures that the deposited capital is in safe hands and if things seem averse, they can anyway be withdrawn as early as one year. Platforms such as Tickertape can be used to study direct company-specific data and perform financial analysis.

On the whole

Having financial goals is mandatory for healthy financial growth. Investing in Fixed Deposits maximizes safety and guarantees a return on investment. Corporate Fixed Deposits can be taken advantage of and used by an informed safe investor for maximizing the returns one can earn from a Fixed Deposit. With just basic fundamental analysis and using the labels provided by the credit rating agencies, one can be informed and also feel safe about making such deposits in a Corporate and enjoy maximized return from an FD scheme which cannot be obtained by being involved in the same exact scheme but through a PSU.

Investment Strategies in the Bond Market

FAQs

1. Can I do premature withdrawal?

Corporate FDs offer a premature withdrawal option but it need not be offered by all other companies as it may vary from company to company.

In the case of a company offering premature withdrawal, as per the RBI’s regulation on premature withdrawal, the deposits are currently locked in for 3 months. It states that the depositor can’t withdraw until 3 months.

They can after 3 months but with penalties that vary. For instance, if it is after 3 months but before 6 months, then no interest will be offered. If it is after 6 months, then you may receive an interest that is 2% lower than the interest that you are supposed to receive in that period. In case the interest is not mentioned for the period then 3% is lowered to the existing interest.

Again the penalty charges may vary from company to company.

2. What is the difference between a bank FD and a corporate FD?

Bank FDs are offered by banks to individuals, generally considered safer with lower interest rates and government-backed insurance. Corporate FDs are issued by companies, offering potentially higher interest rates but with more risk due to the issuer’s creditworthiness. The choice depends on your risk tolerance and financial goals to invest in the instruments you prefer.

3. Can you apply for a corporate FD online?

Yes, you can typically apply for a corporate FD online through the company’s official website or a financial platform that offers such services. Online applications for corporate FDs have become more common and convenient in recent years, allowing investors to complete the application and investment process electronically. Be sure to choose a reputable company and follow their specific online application procedures. Such as GoldenPi is one such Financial Sebi-registered platform that offers various fixed deposit instruments including corporate fixed deposits.

4. What is the minimum tenure for a corporate FD?

The minimum tenure for a corporate fixed deposit (FD) can vary from one company to another. There is no fixed standard for the minimum tenure, and it depends on the terms and conditions set by the specific company issuing the FD. Some companies may offer corporate FDs with minimum tenures as short as a few months, while others may require a minimum tenure of a year or more. To find out the exact minimum tenure for a corporate FD, you should refer to the company’s FD offer document or contact them directly.

5. What are the tax implications?

Under the Income Tax Act, if your corporate FD interest for the year surpasses Rs. 5,000, TDS is obligatory. This interest is categorized as “income from other sources” and taxed based on your applicable tax bracket. For instance, if you’re in the 10% tax bracket, a 10% tax applies to the interest income. If you’re in the zero or NIL tax bracket, you need to submit Form 15H each year to avoid TDS deductions.

6. Is company FD different from Corporate FD?

No, the terms “Company FD” and “Corporate FD” are often used interchangeably to refer to fixed deposits offered by non-banking financial companies (NBFCs) or corporations. They both essentially mean the same thing: fixed deposits issued by companies other than traditional banks. These FDs may offer different interest rates, tenures, and terms compared to bank FDs, but they are both non-bank fixed deposit options.