WHAT HAPPENED IN 2022?

The low single digit return for the calendar year 2022 was similar to the previous year, but here is where the similarities end. The brief sharp increase in global inflation that was anticipated for 2022 actually occurred. This was mostly caused by the conflict between Russia and Ukraine, which disrupted supply chains and caused a rise in oil and other commodity prices that sent inflation rates worldwide above central banks’ target range. Globally, this forced central banks to sharply raise policy rates and tighten financial conditions. Evidence for this can be found in the dramatic change in capital flows, increase in bond yields, and decline in both global equities and bond prices.

To combat sticky inflation at home, the RBI increased the repo rate from 4% to 6.25% in 2022, which reduced liquidity from almost Rs. 8 lakh crores to Rs. 2 lakh crores. This resulted in a bearish flattening of sovereign bond yields.

REPO RATE EXPECTATION FROM RBI IN 2023?

We anticipate RBI to likely increase the repo rate one more time in 2023, to 6.5% i.e. by 25 bps , if necessary, and then take a significant pause. Despite this, RBI will maintain its hawkish stance. Before lowering, we should maintain elevated sovereign yields for a while. Additionally, we anticipate that the private sector will contribute more in 2023.

FOR THE YEAR 2023

The local dynamics in India are a mixed bag of growth, inflation, and the external sector; yet, they do not provide any significant obstacles for the upcoming year. Growth would be slow compared to 2022;

Impact of 👇

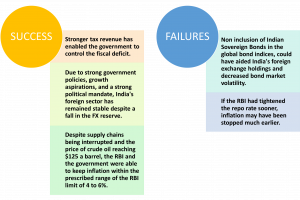

Indian inflation is below 6% for the first time since January 2022, while core inflation is still persistent and broadening, which will be a problem for RBI in 2023. Second, India’s FY23 current account deficit is on pace to equal 3% of GDP. This is worrisome. Increased current account deficits are a sign of an overheated economy and put additional pressure on the rupee to dollar exchange rate. Despite this, tax revenues are increasing and India’s growth is still strong.

On the American market, we think that the Federal Reserve will continue to be hawkish and hike interest rates until inflation starts to decline. The U.S. bond yield curve will remain inverted as a result.

It makes sense that the RBI’s December policy was hawkish. While the overall level of inflation was expected to decline over time. With core inflation being stuck at 6% or above, the RBI is uneasy. Furthermore, RBI observed that the Indian economy is slowing down. Despite this, they continue to be inflation hawks because they are worried about expanding core inflation and how it would affect consumer spending. On the basis of this, we think the RBI will continue to sound hawkish next year until core inflation starts to decline. The sovereign yield curve ought to remain flat as a result.

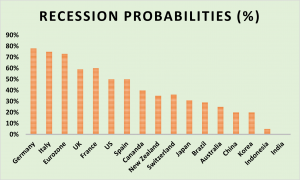

Don’t expect India to see a big contraction or recession. 5.25–5.75% is the predicted growth for FY 2023.

Source- Bloomberg

DEBT MARKET OUTLOOK

In the foreseeable future, we anticipate a narrow range of trading in government bond yields. Investors will arrive in the shape of the Union budget for FY 2024, which will serve as a significant government bond market catalyst. The bond market anticipates a minimum 50 basis points reduction in the fiscal deficit to 5.9% of GDP. The upcoming Union Budget in February 2023 will drive the debt market, as it will also talk about the government’s borrowing plan. The RBI’s assessment of the demand-supply dynamic for bonds in FY23 as well as the actions taken by significant central banks would therefore be a key factor in the bond market. As a result of all of these, benchmark sovereign yields should avoid trading in the higher portion of their trading range.

In recent months, the primary supply of corporate bonds has dramatically increased. Credit spreads should progressively expand if this pattern continues. It is anticipated that the 10-year Indian Government security would trade at 7.38% by the end of this quarter and 7.60% during the following 12 months. The Indian inflation rate is predicted to be 6% by the end of this quarter and to trend around 4.8% in 2023 and 4.5% in 2024.

In 2023, flatter yield curves will provide little incentives for investors to add duration to their portfolios. However, given the generous level of returns, we anticipate investors to make more money💸 next year with the possibility of a small price increase.