|

Getting your Trinity Audio player ready...

|

The Indian debt market plays a crucial role in the country’s financial landscape, providing avenues for both government and corporate entities to raise funds through fixed-income securities. It serves as a vital source of capital for various projects and investments, contributing to overall economic growth.

As the financial year comes to an end, the debt market experiences heightened activity and focus. This period is significant as it marks the closure of financial accounts, prompting companies and investors to reassess their positions, realign portfolios, and make strategic financial decisions.

The purpose of this report is to delve into the key factors affecting the Indian debt market outlook for 2024. By analysing trends, regulatory changes, economic indicators, and global influences, we aim to offer insights into what may shape the landscape of debt securities in the upcoming year.

Global Macroeconomic Environment

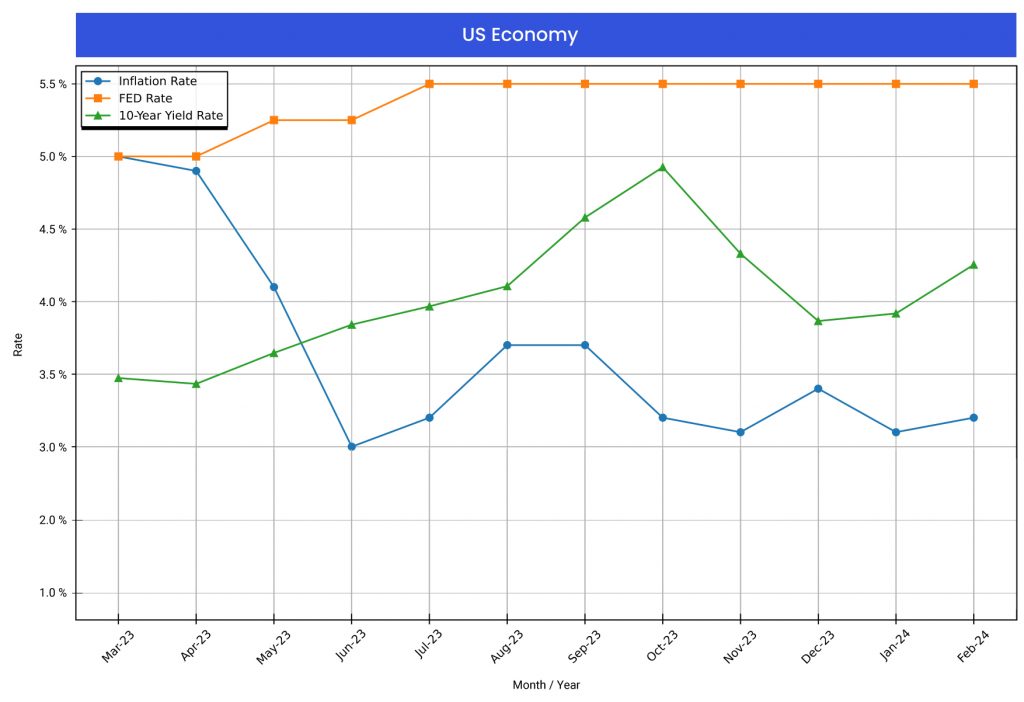

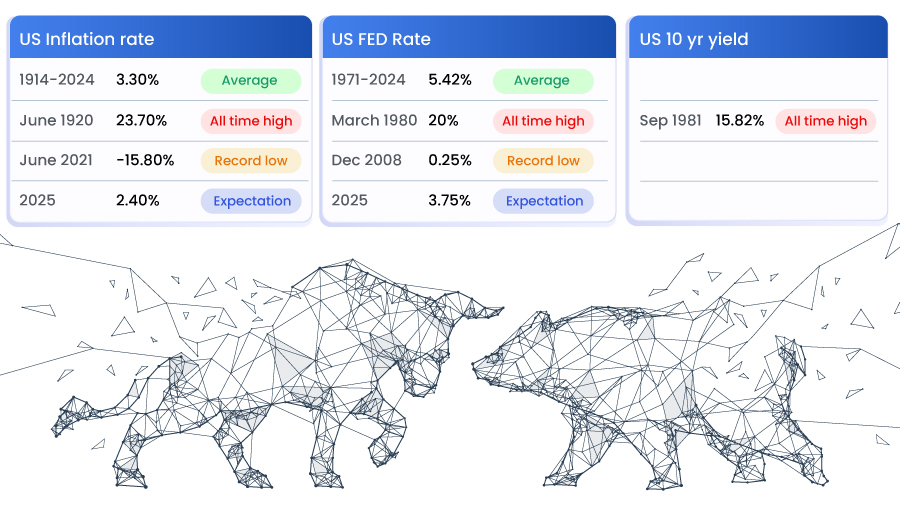

US Economy

Source- Trading Economics, IMF

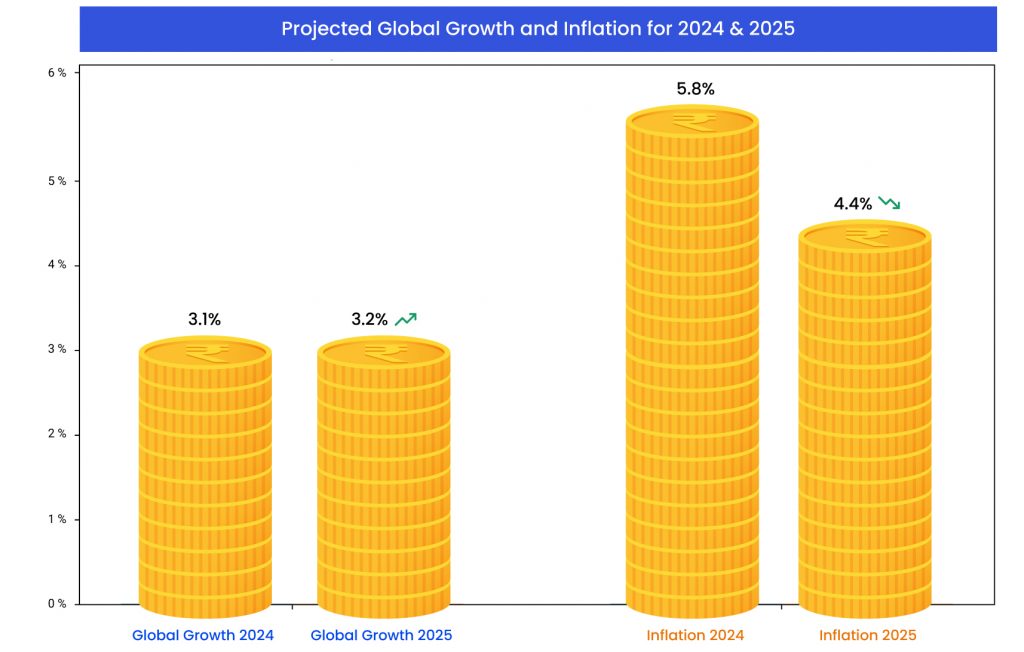

Global Economic Update: Mixed Signals and Elevated Risks

Growth Surprise, But Moderation Ahead: While global GDP growth has outperformed initial forecasts in 2023, it is now expected to slow down. This moderation is attributed to tighter financial conditions (higher interest rates), weakening international trade, and a decline in business and consumer confidence.

Downside Risks Persist: Several factors could further dampen near-term economic prospects. These include:

- Geopolitical Tensions: Heightened tensions on the global stage, such as the ongoing conflict following Hamas’ attacks on Israel, pose a significant risk to economic stability.

- Monetary Policy Impact: The tightening of monetary policy by central banks to combat inflation could have a larger-than-anticipated negative impact on economic activity.

- Deepening property sector woes in China or, elsewhere, a disruptive turn to tax hikes and spending cuts could also cause growth disappointments.

Upside Potential: There are also potential sources of upside for global growth.

- Unlocking Savings: If households tap into the excess savings accumulated during the pandemic and increase their spending, it could provide a boost to economic activity.

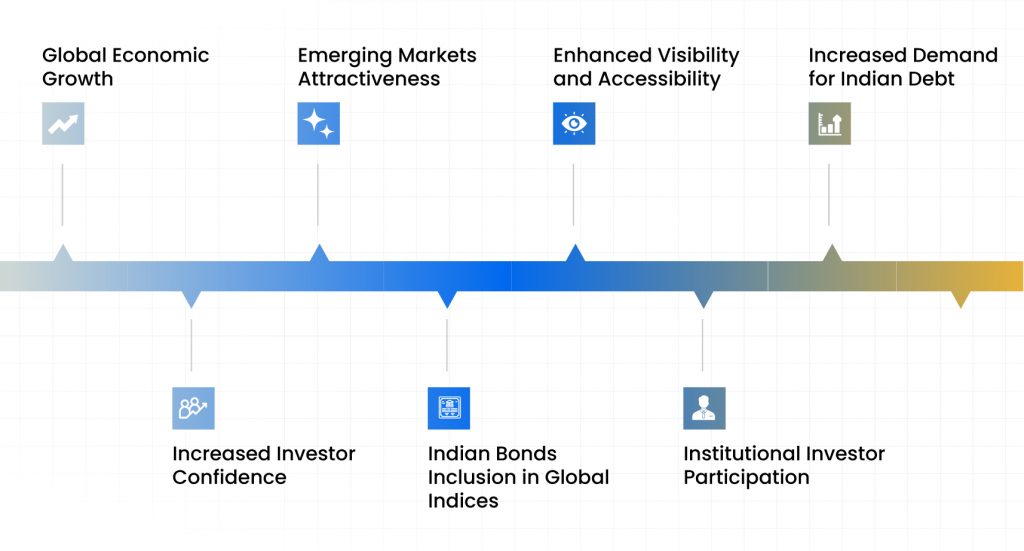

How global growth might influence demand for Indian debt?

Domestic Factors

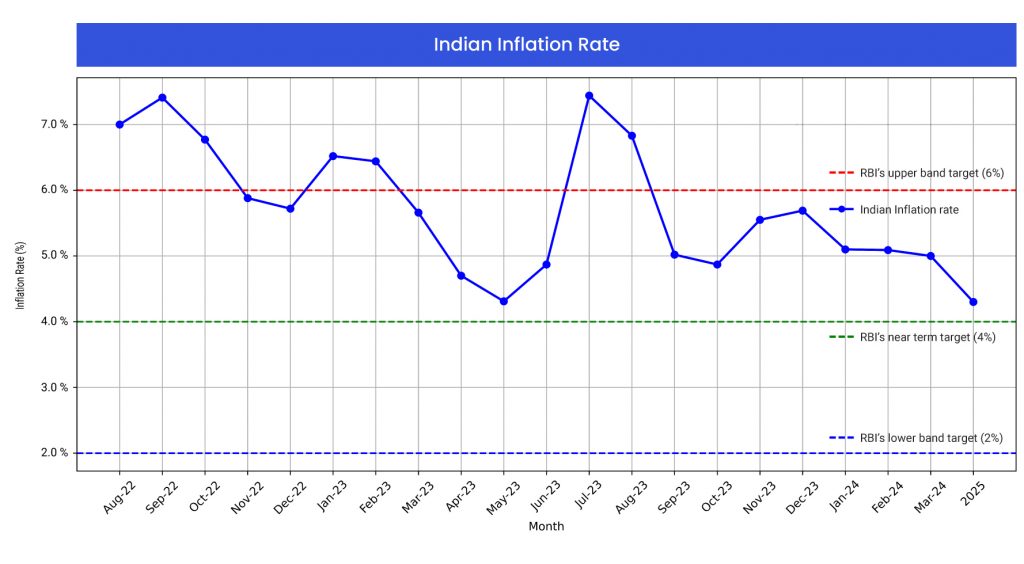

Domestic Inflation & RBI’s Tolerance Limit

Source- RBI

- CPI Inflation Remains Stable: February 2024 saw CPI inflation meet expectations at 5.09%, unchanged from January 2024 and significantly lower than 6.44% in February 2023. This stability occurred despite a rise in food prices.

- Within RBI’s Tolerance Range for Six Months: Positively, CPI inflation has remained within the RBI’s target range of 2% to 6% for six consecutive months, with February 2024 recording the lowest level in this period.

- Cautious Policy Outlook Due to Food Price Volatility: Anticipating potential volatility in food prices in the near future, the RBI is likely to adopt a cautious approach. We expect the central bank to maintain current interest rates for the next quarter to monitor inflationary pressures.

How changes in monetary policy impact the debt market?

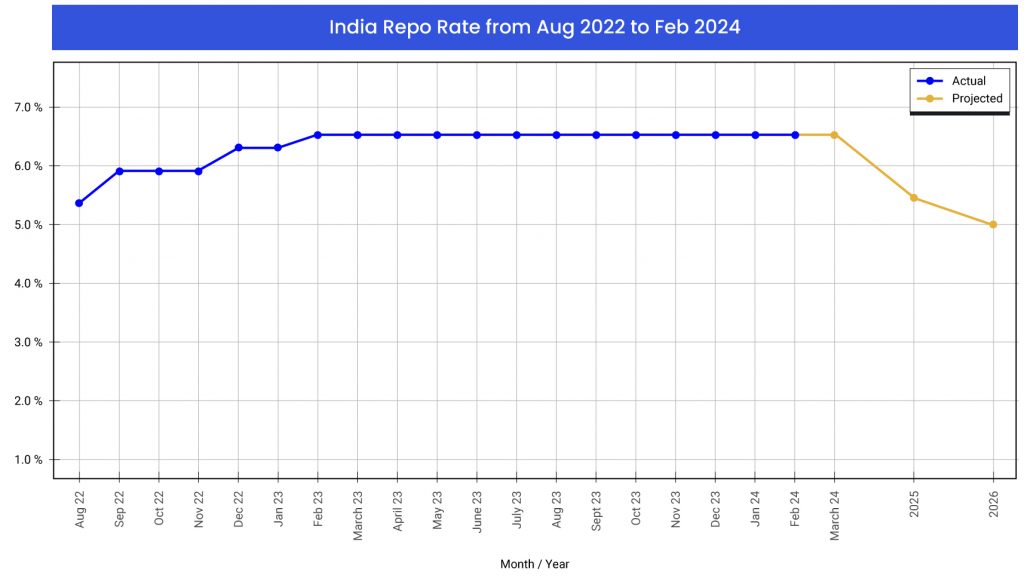

RBI MPC Repo Rate

Source- RBI

- RBI Holds Steady: The Reserve Bank of India (RBI) maintained its policy rates, growth projections, and headline inflation levels at their previous levels during its last MPC meeting.

- Growth Confidence Signals Rate Cuts: RBI’s stance suggests comfort with India’s strong domestic growth. This indicates a potential shift towards rate cuts in the second half of the current fiscal year (H2FY25).

- Liquidity Management and Neutral Policy Stance: The RBI’s ongoing efforts to manage liquidity and bring overnight rates closer to the repo rate suggest a potential move towards a neutral policy stance in the June policy meeting.

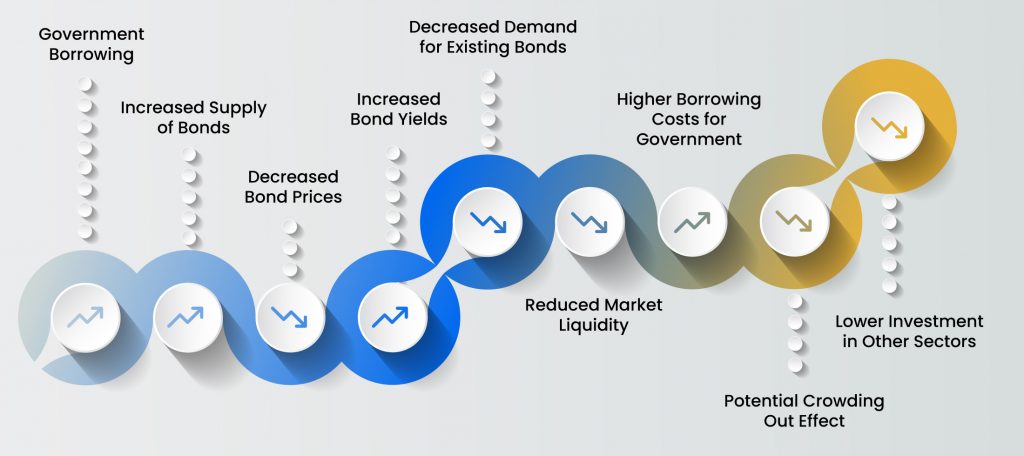

Borrowing and Fiscal Consolidation

- Lower Borrowing Target for FY25: The central government has set a gross market borrowing target of ₹14.13 lakh crore for 2024-25, significantly lower than the ₹15.43 lakh crore projected in Budget 2023.

- Commitment to Fiscal Consolidation: This reduced borrowing target reflects the government’s prioritization of macroeconomic stability over short-term spending. Furthermore, the government is committed to a fiscal deficit target of 5.1% for FY 2024-25, with plans for further reductions in the following fiscal year.

- Improved Fiscal Performance: The government’s borrowing so far in the current fiscal year (₹14.08 lakh crore) is on track with the revised target, indicating progress towards the planned fiscal consolidation.

How government borrowing affects overall debt market liquidity and yields?

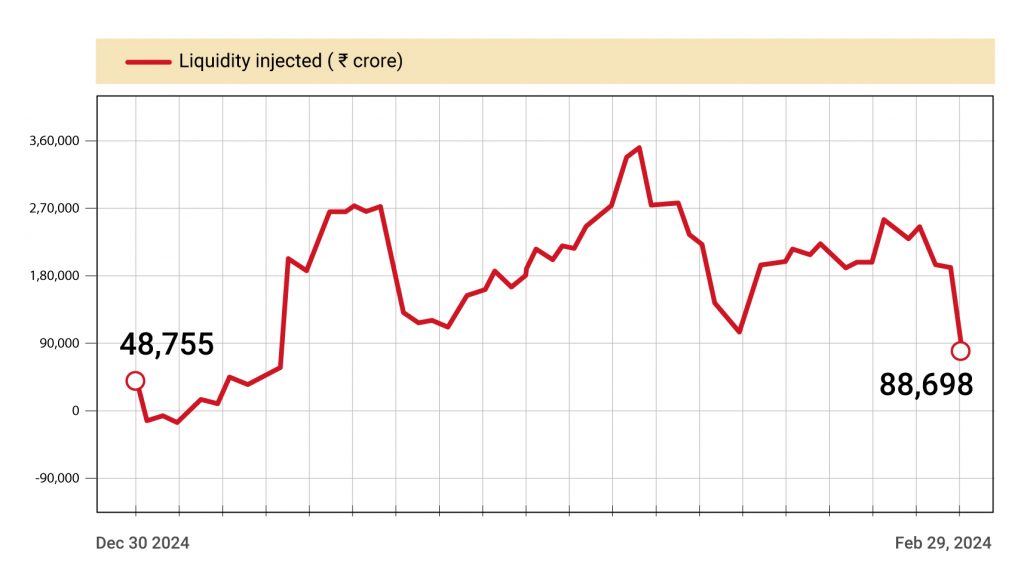

Market Liquidity

Source- Bloomberg, RBI

- Banking System Liquidity Improves: The liquidity deficit in the Indian banking system has narrowed significantly, reaching ₹88,698 crore, its lowest level in over two months. This improvement is attributed to recent government spending.

- Below ₹1 Trillion Deficit: This represents a major positive development, as the last time the deficit fell below ₹1 trillion was on December 15, 2023.

- Potential Short-Term Impact of Tax Outflows: Market participants anticipate that upcoming tax outflows of around ₹1.25 trillion could cause a temporary setback in the liquidity improvement.

- Expectation of Long-Term Relief: Despite the upcoming tax outflows, analysts project an overall easing of liquidity pressures between March end and May. This is based on several factors:

- Increased government spending exceeding its receipts.

- Distribution of dividends by the Reserve Bank of India (RBI).

- Normalization of currency outflows.

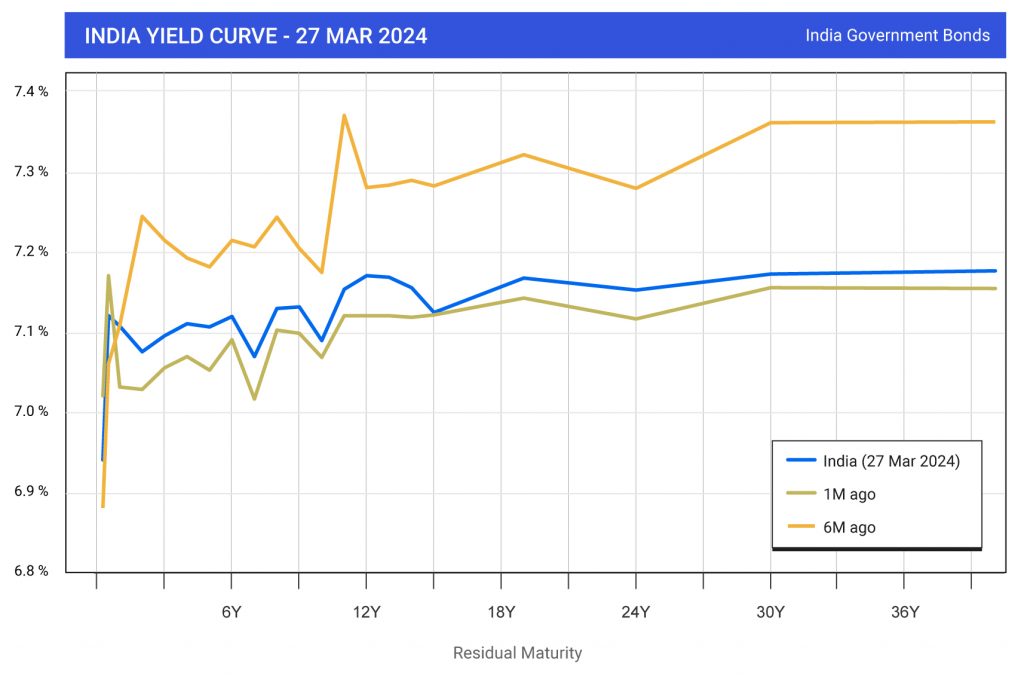

Rising Demand and Flattening Yield Curve

Source- World Government Bonds

- Strong Demand for Long-Term Bonds: High demand, especially from foreign banks buying for FRAs (financial agreements), has squeezed the yield spread on long-term government bonds to its lowest in a year. This flattens the yield curve (interest rates on short-term vs. long-term bonds).

- Insurance Companies Step Up: With government bond auctions finished, insurance companies are actively buying long-term bonds to fill their investment needs.

- Flattening Trend Likely to Continue: Analysts expect the yield curve to stay flat, possibly until March-end.

- FRAs More Attractive: Lower overnight index swap rates (another interest rate tool) and new investment limits for foreign banks are making FRAs more appealing, boosting demand for Indian bonds.

- Foreign Banks Drive Market: Foreign banks have net-bought ₹685 billion in bonds this year, with a significant portion potentially used for FRAs, further fueling overall demand.

Post Inclusion of Chinese bonds in Global Indices

- Second-Largest Bond Market and Third-Largest Government Bond Market

- Surge in Foreign Investment: China’s bond market is experiencing a significant influx of foreign capital, with estimates suggesting annual inflows exceeding $100 billion from 2020 to 2030.

- Growing Market Share: This foreign interest is reflected in a rising share of foreign investors in the domestic bond market, climbing from a mere 2% to a more substantial figure.

- Yield Compression: The increased demand from foreign investors has led to a compression of yields. China’s 10-year government bond yield has dropped by 16 basis points this quarter, reaching 3.06%, close to its lowest level since December 2016. This trend suggests that China’s bonds are becoming increasingly attractive to global investors.

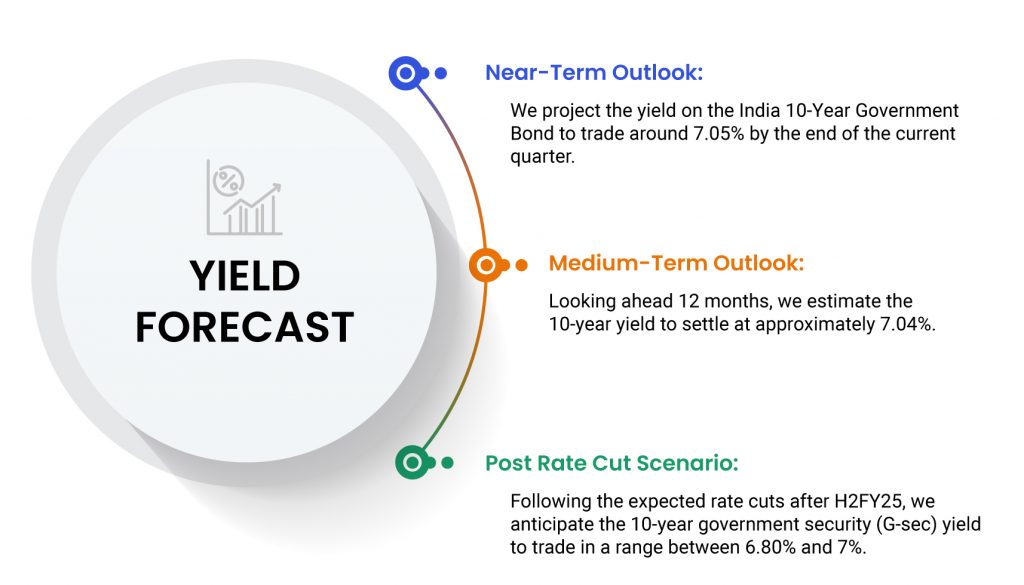

Investment Strategy

- Accrual Focus: We maintain an “accrual strategy,” prioritizing debt instruments that generate returns through regular interest payments. This approach is favorable because the short to medium-term sections of the yield curve offer an attractive risk-reward profile.

- Anticipated Inflation Dip: Assuming normal weather patterns, we expect Consumer Price Index (CPI) inflation to decline further in the coming months from its current level of 5.09%.

- Market Drivers: Global anticipation of central bank rate cuts and continued net foreign investment in the Indian debt market are likely to be the key drivers of the market in the near future.

Scenario 1: Continued Strong Demand and Flattening Yield Curve

- Focus on Long-Term Bonds: If you anticipate the flattening trend in the yield curve to persist, then long-term government securities could be a good option. However, remember that long-term bonds are generally more sensitive to interest rate changes.

- Credit Quality Matters: While demand for government bonds is strong, consider the credit quality of any corporate bonds you might invest in.

Scenario 2: Potential Liquidity Tightening Due to Tax Outflows

- Short-Term Instruments: If you are concerned about potential liquidity tightening due to upcoming tax outflows, then short-term debt instruments like commercial papers or Treasury bills might be a better choice. These offer lower returns but provide quicker access to your cash.

- Active Management: Consider an actively managed debt fund that can adjust its portfolio based on changing market conditions.

A Dynamic Landscape with Promising Opportunities

In conclusion, the outlook for the Indian debt market in 2024 is influenced by a combination of global and domestic factors. The global macroeconomic environment, including projected growth and inflation, will shape investor confidence and demand for Indian debt securities. Furthermore, domestic factors such as CPI inflation, RBI’s monetary policy, government borrowing, and market liquidity provide critical insights into the market’s future trajectory.

The report highlights the potential impact of global economic conditions on the demand for Indian debt, emphasizing the significance of increased investor confidence, emerging market attractiveness, and the potential inclusion of Indian bonds in global indices. It also underscores the effects of domestic factors, such as changes in monetary policy, government borrowing, and market liquidity, on the debt market.

As the financial year comes to a close, the report sheds light on key developments, including RBI’s policy stance, government borrowing targets, market liquidity trends, and investor behavior. Lastly, it provides valuable investment strategies based on different market scenarios and emphasizes the importance of active management in a dynamic market environment. In light of these insights, investors and organizations operating in the Indian debt market are encouraged to consider the interplay of these factors in their investment decisions.