|

Getting your Trinity Audio player ready...

|

High Yield | CRISIL, CARE & ICRA AAA/Stable Rated

Bond overview:

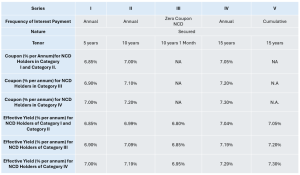

Power Finance Corporation Limited is issuing the Non-Convertible Debentures. These NCDs are AAA/Stable rated by CRISIL, ICRA and CARE. The NCDs are being issued in five series: coupon ranges from 6.85% to 7.30% p.a. and different tenures of 5 Years, 10 years, 10 years 1 month & 15 years. The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series:

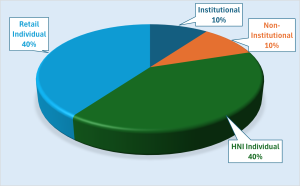

Allocation Ratio:

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Power Finance Corporation (PFC) NCD-IPO.

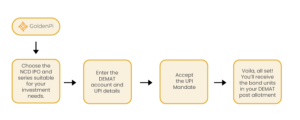

Investment Process for Power Finance corporation NCD IPO:

You can invest in IPOs via GoldenPi in these easy steps.

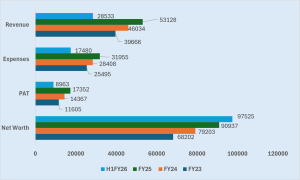

Financial Overview:

Snapshot stating the Revenue, Expenses, PAT and Net-worth (In crores):

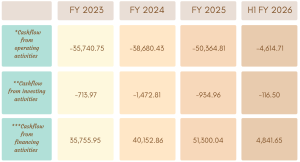

Cash flow for last few years (In crores):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

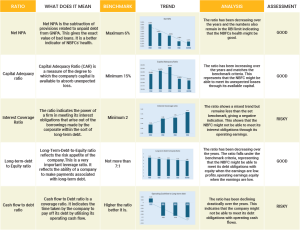

Ratio Analysis:

Issue analysis:

Pros:

- PFC has a AAA/Stable rating from CRISIL, CARE & ICRA which means that it is considered to be a very safe investment.

- These NCDs are senior secured in nature providing an additional layer of protection to your investment. Minimum security cover of at least 100% till final redemption of NCDs.

- An opportunity to invest in one of the leading power sector NBFC of India having Govt of India (GOI) backing.

- Including AAA/Stable rated NCDs in an investment portfolio can diversify risk, especially for investors with a large exposure to equities or other high-risk assets.

Cons:

- The interest rates on NCDs are typically lower than the returns on other types of investments, such as stocks or mutual funds.

- In a changing interest rate environment, the fixed interest rate on the NCD may become less attractive if market interest rates rise significantly.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About PFC:

Power Finance Corporation Limited (“PFC”), established in 1986, is a Schedule-A Maharatna Central Public Sector Enterprise (“CPSE”) and a premier public financial institution in India, specializing in the power sector’s financing. As a publicly traded Government of India (“GoI”) business and a public financial institution under the Companies Act of 2013, PFC is registered with the RBI as a systemically important, non-deposit-accepting NBFC. It is also classified as an Infrastructure Finance Company (IFC), enabling it to meet India’s long-term power and infrastructure financing requirements.

PFC holds a strategically important position in the Government of India’s power sector development initiatives, benefitting from strong policy support. It serves as the nodal agency for various key government schemes, including the Revamped Distribution Sector Scheme (RDSS), Ultra Mega Power Projects (UMPPs), and the Late Payment Surcharge (LPS) mechanism for Discoms.

The company offers a comprehensive range of financial products, such as long-term and short-term loans, project finance, refinancing, equipment lease financing, guarantees, and advisory services. These are provided across the entire power value chain, covering generation, transmission, and distribution. PFC’s diverse client base includes central and state power utilities (SPUs), private power producers, renewable energy companies, and equipment manufacturers.

In recent years, PFC has broadened its focus to include renewable energy, clean technologies, and energy transition projects. Furthermore, it has selectively ventured into infrastructure and logistics segments like electric mobility, roads, metro rail, and smart cities. The company also accesses global capital markets, notably through green bonds.

Key Highlights:

Strengths:

- Quasi-sovereign backing: Strategic GoI entity with 55.99% ownership (Jun ’25); nodal agency for key power sector schemes, supporting funding access and policy backing.

- Healthy profitability: PAT grew 21% YoY to ₹17,352 cr in FY25, driven by improved NIMs at 3.6% (3.3% FY24), low opex (0.13% ATA) and controlled credit costs, supporting strong Return on total assets (RoTA) of 3.2% (3.3% annualised in Q1FY26).

- Improving asset quality trend: GNPA declined to 1.94% (Mar ’25) vs 3.34% (Mar’24) with sustained recoveries; PCR ~80% on Stage III assets (Jun ’25).

- Healthy capitalisation: Capital adequacy ratio (CAR) at 22.4% (Jun ’25) well above regulatory minimum of 15%; gearing improved to 6.4x (Mar’25) from 6.7x (Mar ’24).

- Diversified and low-cost funding profile: Access to domestic bonds (57%), bank loans, ECBs and multilateral funding; 95% of forex borrowings hedged, limiting currency risk.

- Market leadership in power financing: Loan book grew ~13% YoY to ₹5.43 lakh Cr (FY25) and further to ₹5.50 lakh Cr (Jun ’25) led by LPS (Late Payment Surcharge) and RBPF ( Revolving Bill Payment Facility) disbursements.

- Gradual portfolio diversification: Rising exposure to renewables (15% of loan book) and initial foray into infrastructure (~2% as of Jun ’25) reduces long-term concentration risk.

- Strong liquidity position : Cash & investments of ~₹12,700 Cr (Mar ’25), scheduled collections of ₹93,945 Cr and ₹14,768 Cr of undrawn bank lines, together comfortably covering FY26 debt obligations of ₹83,715 Cr.

Weakness:

- High sectoral concentration: Power sector exposure remains dominant, reflecting mandate; diversification into infrastructure is still nascent (2% of loan book).

- Exposure to financially weak state power utilities (SPUs): Discoms account for ~40% of loan book, exposing PFC to state utility payment risks despite government-backed mechanisms (LPS).

- Borrower concentration risk: Top 20 borrowers account for ~54% of loan book (Mar ’25), though marginally improved from ~57% in Mar’24.

- ALM structural mismatch: Negative cumulative mismatch in 3-5 yr bucket, though mitigated by strong liquidity buffers and sovereign-linked funding access.

- Rising private sector exposure: Private sector loans increased to 23% (Jun’25) from 19% (Mar’24), which could add to asset quality volatility over cycles.

- Infrastructure lending execution risk: Entry into non-power infrastructure introduces new asset quality and execution risks, requiring careful monitoring.

Invest in Bond IPO online in just 5 minutes

Source: Tranche I Prospectus Dated January 9, 2026

Disclaimer – The information is published as on date 15/01/2026 based on information available on Tranche I Prospectus dated January 9, 2026. The information may be subject to change in case of change in terms of prospectus or any other reason as the case may be. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors