|

Getting your Trinity Audio player ready...

|

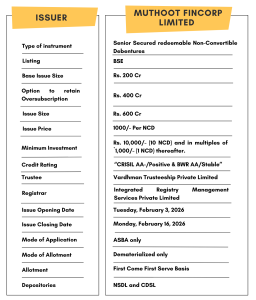

High Yield | CRISIL AA-/Positive & BWR AA/Stable Rated | Minimum Investment: 10K Only

Note: New Muthoot Fincorp Limited NCD IPO is now Open

Bond overview:

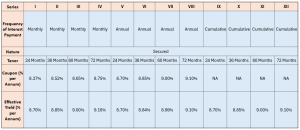

Muthoot Fincorp Limited is issuing the Non-Convertible Debentures. These NCDs are AA-/Positive rated by CRISIL and AA/Stable by Brickwork Ratings. The NCDs are being issued in twelve series: yield ranges from 8.70% to 9.10% p.a. and different tenures of 24 Months, 36 Months, 60 Months & 72 Months. The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series:

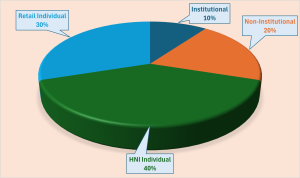

Allocation Ratio:

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Muthoot Fincorp Ltd. NCD-IPO.

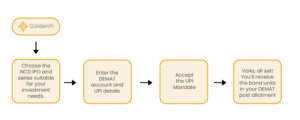

Investment Process for Muthoot Fincorp Limited NCD IPO:

You can invest in IPOs via GoldenPi in these easy steps.

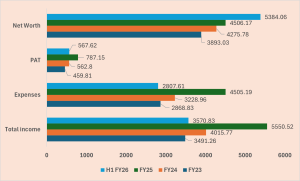

Financial Overview:

Snapshot stating the Total Income , Expenses, PAT and Net-worth (In crores):

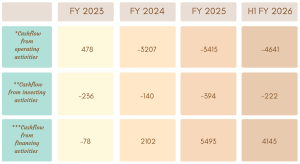

Cash flow for last few years (In crores):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

Ratio Analysis:

Issue analysis:

Pros:

- Strong Credit Rating: Rated CRISIL AA-/Positive and BWR AA/Stable, indicating high degree of safety and low credit risk.

- Secured NCDs: Backed by a subservient charge on loan receivables and current assets, offering security to debenture holders.

- Security Cover: The security cover required must be a minimum of 100% of the total of the outstanding principal balance of the NCDs and any accrued interest.

- Competitive yields: up to 9.10% vs bank FDs.

- Wide tenor and payout options: monthly to cumulative

- Extensive Reach: Over 3,736 branches across India ensures strong customer base and rural presence.

Cons:

- Exposure to Gold Loan Volatility: A large portion (approx 87%) of business still depends on gold loan pricing and demand cycles.

- Asset Quality Pressure: Any adverse movement in collateral value (especially gold) could impact collections.

- Interest Rate Risk: More pronounced in longer tenors (60-72 months).

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Muthoot Fincorp Limited:

Muthoot Fincorp Ltd. (MFL), incorporated in 1997 and registered with the RBI, is a Kerala-based, non-deposit taking NBFC. It primarily offers small-ticket gold loans against household gold jewellery, a segment where it has over two decades of experience. As of September 30, 2025, gold loans comprised approx 87% of its total loan book, reflecting a secured, retail-focused model.

Muthoot Fincorp Ltd, the flagship entity of the diversified Muthoot Pappachan Group (also known as Muthoot Blue Group), also provides secured and unsecured MSME lending. Beyond lending, the company offers mutual fund and insurance distribution, foreign exchange/money transfer services, operates as a Category II Depository Participant of CDSL, and owns wind power assets in Tamil Nadu.

Its three subsidiaries are: Muthoot Housing Finance (affordable housing loans), Muthoot Microfin (micro credit to women entrepreneurs), and Muthoot Pappachan Technologies (IT services). MFL has a strong pan-India presence, operating approx 3,736 branches across 25 states and union territories, with key presence in Kerala, Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, and Maharashtra.

Key Highlights:

Strengths:

- Experienced management & strong promoter commitment: Promoters hold 99.86% equity stake, reflecting high confidence and long-term commitment; Muthoot Fincorp is part of the Muthoot Pappachan (Blue) Group with 138+ years legacy, backed by promoters’ deep, multi-decade expertise in gold loan and retail lending.

- Predominantly secured retail portfolio: ~96% of AUM is secured, with ~87% backed by gold jewellery and ~10% through mortgages (home loans and LAP), supporting a low-risk, small-ticket retail lending model with strong collateral cover and high recoverability.

- Adequate Capitalisation: Net worth stood at ₹5,384 Cr as of Sept’25, supported by strong internal accruals. Gearing was moderate at 5.8x, while a healthy CRAR of 18.91% provides adequate buffers to support growth and maintain financial stability.

- Improving profitability profile: AUM per branch has improved to ₹6.97 Cr in FY25 from ₹5.90 Cr in FY24. PAT increased to ₹787 Cr in FY25 from ₹563 Cr in FY24, with Return on Managed Assets (RoMA) improving to 2.3% (FY24: 2.1%), driven by strong core gold loan performance. Profitability remained stable in H1 FY26, with annualised RoMA of ~2.6%, supported by low credit costs and operating efficiency, reflecting resilient standalone earnings.

- Healthy Asset Quality : Net-NPA (NNPA) improved to 0.76% as of Sept’25 from 1.28% in Mar’25, reflecting strong collection efficiency and low delinquencies in the gold loan book.

- Diversified funding profile: Funding is well diversified, with access to a wide network of PSU and private banks (including SBI, PNB, BoB, Axis bank, HDFC bank IndusInd, Federal Bank, among others), alongside capital market instruments (NCDs, ECBs, Subdebt, CP), supporting funding stability and refinancing flexibility.

- Strong liquidity: As of Sep’25, Muthoot Fincorp had liquidity of ₹3,063 Cr (₹2,457 Cr cash & equivalents + ₹606 Cr undrawn CC/WCDL), with positive ALM gaps in the up to 1-year bucket, comfortably covering near-term debt repayments of ₹1,793 Cr over the next three months.

Weakness:

- Geographical concentration risk: Despite a pan-India presence, ~56.3% of AUM is concentrated in five states – Karnataka (16.0%), Tamil Nadu (12.6%), Telangana (10.7%), Andhra Pradesh (8.6%) and Maharashtra (8.4%) – exposing the portfolio to regional economic and regulatory risks.

- High reliance on the gold loan segment: While gold loans are a strength, high business concentration limits diversification benefits and makes earnings sensitive to regulatory changes or sharp volatility in gold prices.

- Asset quality pressure in microfinance segment: Microfinance GNPA increased, with 90+ dpd at 6.2% (June 2025) vs 5.6% (March 2025) and elevated credit costs (7.5% in FY25) vs (1.5% in FY24 & 2.5% in FY23), driven by borrower overleveraging, elections, heat waves and localised collection challenges.

Invest in Bond IPO online in just 5 minutes

Source: Tranche I Prospectus Dated January 29, 2026

Disclaimer – The information is published as on date 05/02/2026 based on information available on Tranche I Prospectus dated January 29, 2026. The information may be subject to change in case of change in terms of prospectus or any other reason as the case may be. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors