Current 10-Year G-Sec Yield: ~7.05% (as of May 14, 2026)Yields have moved higher in recent months, driven by elevated global crude oil prices, geopolitical tensions, and FPI outflows from domestic debt markets. The benchmark 6.48% 2035 bond has seen its yield hold near the 7.05% level.(Source: Trading Economics / CCIL — updated May 2026)

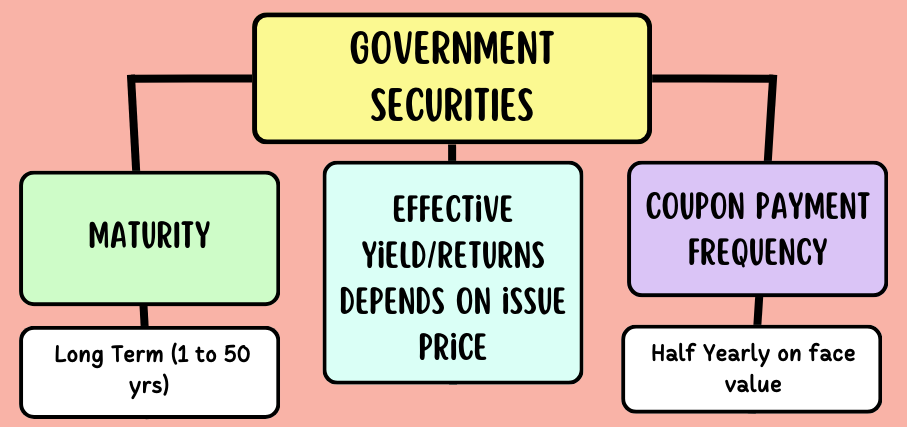

A ‘Government Security‘ (G-Sec) is a tradable financial instrument issued by either the central or state governments, representing an acknowledgment of their debt obligation. These securities come in two main categories:

Short-Term: Often known as “Treasury Bills,” these have initial maturities of less than a year.

Long-Term: Typically referred to as Government Bonds or Dated Securities, these have an original maturity of one year or more. Investors can conveniently access and purchase these government bonds online, streamlining the investment process and making it more accessible.

A typical dated G-Sec is identified by three components: the coupon rate, the issuer name, and the maturity year. Here is how to read a G-Sec name:

Component

Example Value

What It Means

Coupon Rate

7.17%

The annual interest rate paid on the face value of the bond.

Issuer

GS (Government Security)

Indicates it is issued by the Government of India.

Maturity Year

2028

The year in which the principal will be repaid.

SEBI Registered • OBPP Licensed

Invest in bonds & earn 9-14%* p.a. fixed returns

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

India’s government securities market has grown significantly in size and depth over the past several years. As per the Union Budget for FY 2025–26, the government’s borrowing program reflects both fiscal ambition and a measured consolidation strategy.

Borrowing Metric

FY 2024–25 (Actuals)

FY 2025–26 (Budget Estimate)

Gross Market Borrowings (Dated Securities)

₹14.01 lakh crore

₹14.82 lakh crore

Net Market Borrowings (Dated Securities)

~₹10.82 lakh crore

₹11.54 lakh crore

Sovereign Green Bonds (Included in gross)

₹20,000 crore

₹10,000 crore

Maturity Buckets (H1 FY26)

—

3Y to 50Y securities across 26 weekly auctions

Source: RBI / PIB / Union Budget 2025–26

The FY 2025–26 borrowing program spans maturities from 3 years to 50 years, with the 10-year bucket accounting for the largest share at 26.2% of total H1 issuance. The government has also continued its buyback and switching program to smooth out the redemption profile in the near-term years.

Current Market Yield Context: The 10-year benchmark G-Sec yield is hovering near 7.05% (May 2026), up from lows of around 6.22% seen in May 2025, reflecting the impact of rising global crude oil prices, FPI outflows, and geopolitical uncertainty.

Advantages of Holding G-sec

1. Security and Assurance:

Government securities are backed by the full faith and credit of the government, offering one of the safest investment options. Issued by the Reserve Bank of India, they provide a secure haven for investors.

2. Competitive Yields in a Dynamic Rate Environment

In the current interest rate environment, government securities offer competitive yields that are risk-free by nature. As of May 2026, the 10-year G-Sec benchmark yield stands near 7.05%, making it an attractive baseline for conservative fixed-income investors. With rising global uncertainty, investors increasingly value the security and predictability that G-Secs offer – particularly when corporate bonds carry additional credit risk. For investors seeking stable, sovereign-backed returns without credit exposure, G-Secs present a compelling case

3. Convenient Entry and Exit:

Facilitated by the National Stock Exchange’s auction platform, purchasing and selling these bonds in the secondary market is seamless. The active secondary market ensures investors can easily liquidate their holdings.

4. Steady Fixed-Income Returns:

With a predetermined interest rate, investors enjoy a reliable income stream until maturity. This fixed-income nature makes them particularly appealing for businesses seeking stability over an extended period.

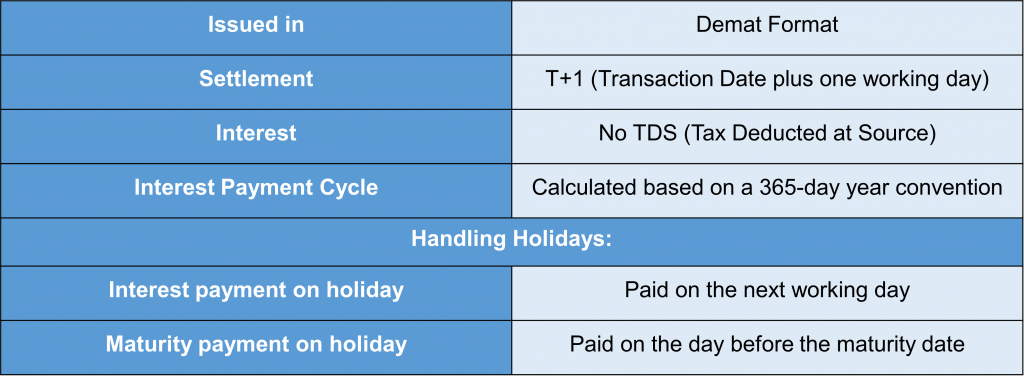

5. Tax Advantage – No TDS:

Interest earned on government securities is not subject to Tax Deducted at Source (TDS), enhancing returns for investors.

6. Versatile Collateral Option:

Government securities can serve as collateral for loans, providing an additional layer of financial flexibility for investors.

7. Dematerialized Convenience:

Eliminating the need for physical documentation, these securities can be held in dematerialized form, streamlining online transactions and enhancing overall accessibility.”

What are the limits for investors’ bidding amount?

The following limits apply to retail investors participating through the Non-Competitive Bidding (NCB) route via NSE goBID or registered trading members:

Parameter

Details

Minimum Bidding Amount

₹10,000 (face value)

Bidding Increments

Multiples of ₹10,000

Maximum Bid — GOI Dated Securities

₹2,00,00,000 (₹2 crore) per security per auction

Maximum Bid — Treasury Bills (T-Bills)

₹2,00,00,000 (₹2 crore) per security per auction

Maximum Bid — State Development Loans (SDLs)

₹2,00,00,000 (₹2 crore) per security per auction

Bidding Route

NSE goBID web platform or via NSE-registered trading members

Bid Type

Non-Competitive Bidding (NCB) — no need to quote yield/price

Allotment Price

Weighted average price/yield of that auction

Important Update: The NSE goBID mobile app (Android & iOS) was temporarily discontinued from July 30, 2025. Retail investors can continue to access the platform via the NSE goBID web portal at eipo.nseindia.com. Check NSE’s website for the latest status on the mobile app reinstatement.

How much will you earn if you invest in G-sec?

Let us understand G-Sec returns with a simple example. Every bond has a face (par) value of ₹100, but may be issued at par, at a premium (above ₹100), or at a discount (below ₹100), depending on the auction outcome.

Investor buys 7.00% GS 2026 at a discount price of ₹98 for 120 units

Parameter

Calculation

Value

Bond Name

—

7.00% GS 2026

Face Value per Unit

—

₹100

Purchase Price per Unit

—

₹98 (at discount)

Units Purchased

—

120

Total Amount Invested

$₹98 \times 120$

₹11,760

Annual Coupon Rate

—

7.00% on face value

Interest Per Unit (Half Year)

$₹100 \times 7\% \div 2$

₹3.50

Total Interest Per Half Year

$₹3.50 \times 120$

₹420

Total Interest Per Year

$₹420 \times 2$

₹840

Principal Repaid at Maturity

$₹100 \times 120$

₹12,000

Profit at Maturity (Capital Gain)

$₹12,000 – ₹11,760$

₹240

So the total amount paid by the investor would be 98*120= Rs 11760

Summary of Cash Inflows for the Investor:

As the interest is paid on half yearly basis, the total amount earned is as follow-

Cash Flow Component

Amount

Biannual Interest (per period)

₹420

Total Interest Over Holding Period

Depends on tenure remaining

Principal at Maturity

₹12,000

Capital Gain (Discount to Par)

₹240

Taxation Process for G-sec

Most Government Securities are not tax-exempt. Interest income from G-Secs is classified as “Income from Other Sources” and taxed at your applicable income tax slab rate. There is no TDS deducted on G-Sec interest income. However, taxes must be self-declared and paid accordingly.

Capital Gains Tax on G-Secs

Type of Gain

Holding Period

Tax Rate

STCG — Listed G-Secs

Held for 12 months or less

Taxed at applicable income tax slab rate

LTCG — Listed G-Secs

Held for more than 12 months

12.5% without indexation (Section 112)

STCG — Unlisted Bonds / G-Secs

Held for 24 months or less

Taxed at applicable income tax slab rate

LTCG — Unlisted Bonds / G-Secs

Held for more than 24 months

12.5% without indexation

Key Changes Post–Finance Act 2024 (effective July 23, 2024):

LTCG rate has been rationalised to a flat 12.5% without indexation for bonds and G-Secs (previously 20% with indexation under Section 112).

Indexation benefit has been removed for most non-equity assets transferred on or after July 23, 2024.

No TDS is applicable on G-Sec interest income — but the investor must declare and pay tax as per applicable slab.

Tax-free bonds (e.g., certain infrastructure bonds like NHAI, REC) remain exempt from income tax on interest, but are a separate category from standard G-Secs.

Source: Income Tax Department / Finance (No. 2) Act, 2024 / CBDT FAQs

KYC Process

Photo

Scanned copy of PAN Card

Scanned copy of Voter ID/ Adhaar Card/ Driving License

Canceled cheque/ Bank Statement/ Passbook Copy

Demat Copy- CMR or CML or eCAS Statement of CDSL or NSDL

Bidding Period of NSE

The RBI conducts government securities auctions on a weekly basis. NSE acts as a facilitator for retail investors through the Non-Competitive Bidding (NCB) route. The typical auction and bidding schedule is as follows:

Security Type

Auction Day (RBI)

NCB Bidding Window (NSE goBID)

GOI Dated Securities (G-Secs)

Every Friday

Opens after RBI notification; closes before auction cut-off

Treasury Bills (T-Bills)

Every Wednesday

Opens after RBI notification; closes before auction cut-off

State Development Loans (SDLs)

Every Tuesday

Opens after RBI notification; closes before auction cut-off

Note: The specific dates and bidding windows are confirmed each week by the RBI through auction notifications and are made available on the NSE goBID web platform. Investors should check the live schedule at NSE NCB Portal before placing bids. Auction schedules may vary during public holidays or special market events.

Difference Between G-Sec, Strips and Treasury Bills

Features

Government Securities

Strips

Treasury Bills

Nature of Instrument

Long-term debt instruments issued by the government with fixed or floating interest rates.

Zero-coupon securities created by separating the interest and principal components of a government security.

Short-term money market instruments issued by the government.

Maturity Period

Generally, medium to long-term maturity, ranging from 5 to 50 years.

Maturity period depends on the residual maturity of the underlying security from which Strips are created.

Short-term, with maturities ranging from 91 days to 364 days.

Interest Payments

Pay regular interest payments (semi-annually)

Zero-coupon bonds do not pay periodic interest; instead, they are issued at a discount and redeemed at face value.

Treasury Bills do not pay periodic interest; they are issued at a discount and redeemed at face value.

Yield

Yield is calculated based on the market price of the security and the remaining interest payments

Yield is calculated based on the difference between the purchase price and the redemption value

Yield is calculated based on the discount rate at which the treasury bill is sold

Liquidity

Relatively high liquidity

Lower liquidity than government securities

High liquidity

Trading in the Secondary Market

Traded in the secondary market, providing liquidity to investors.

Strips can be traded individually in the secondary market.

Treasury Bills can be traded in the secondary market.

Face Value Redemption

Redeemed at face value upon maturity.

Redeemed at face value upon maturity.

Redeemed at face value upon maturity.

Risk and Returns

Generally considered low-risk investments with stable returns.

Lower risk due to the guaranteed redemption value; returns depend on the purchase price.

Considered low-risk due to government backing; returns are typically lower compared to longer-term securities.

Issuing Authority

Issued by the Reserve Bank of India (RBI) on behalf of the Government of India.

Created by primary dealers in consultation with the RBI.

Issued by the RBI on behalf of the Government of India.

Primary Market Auctions

Initially issued through auctions in the primary market.

Not issued through auctions; created by primary dealers.

Initially issued through auctions in the primary market.

Denomination

Generally available in multiples of INR 10,000 or INR 100,000.

Denominated in smaller units, facilitating retail participation.

Usually issued in multiples of INR 25,000.

Some Important facts before you invest into Government Securities

FAQs

1. What are Government Securities?

Government Securities (also known as G-Secs) are debt instruments or bonds issued by central or state governments. They represent the government’s debt obligation, and may carry a full or quasi-sovereign guarantee. Usually, such bonds come with a pre-determined interest rate paid half-yearly.

2. Are Government Securities the same as G-Secs?

Yes, Government Securities are commonly called “G-Secs” in India. It includes both short-term 91-Day Treasury Bills (T-bills) and long-term government bonds.

3. How do G-Sec yields look in 2026?

India’s 10-year G-Sec yield is currently hovering near 7.05% as of May 14, 2026. Yields have risen sharply compared to the lows of approximately 6.22% seen in May 2025, driven by a combination of rising crude oil prices, foreign portfolio investor outflows, and geopolitical tensions in West Asia, which have stoked inflation concerns for India’s import-dependent economy

India’s 10-year G-Sec yield moved from 7.17% in April 2024 to a low of 6.22% in May 2025, before rising again to 6.77% by January 2026, and has continued to climb since then. For investors, this current yield environment presents an attractive entry point into G-Secs — locking in sovereign-backed returns at multi-month highs

About GoldenPi Expert

Abhijit Roy | CEO & CO-Founder GoldenPi

With over 15 years of experience across fixed income and debt markets, he brings deep domain expertise along with a strong focus on investor education and transparency. An alumnus of IIT Kharagpur and IIM Calcutta, his views are personal and should not be considered investment advice.