")

|

Getting your Trinity Audio player ready...

|

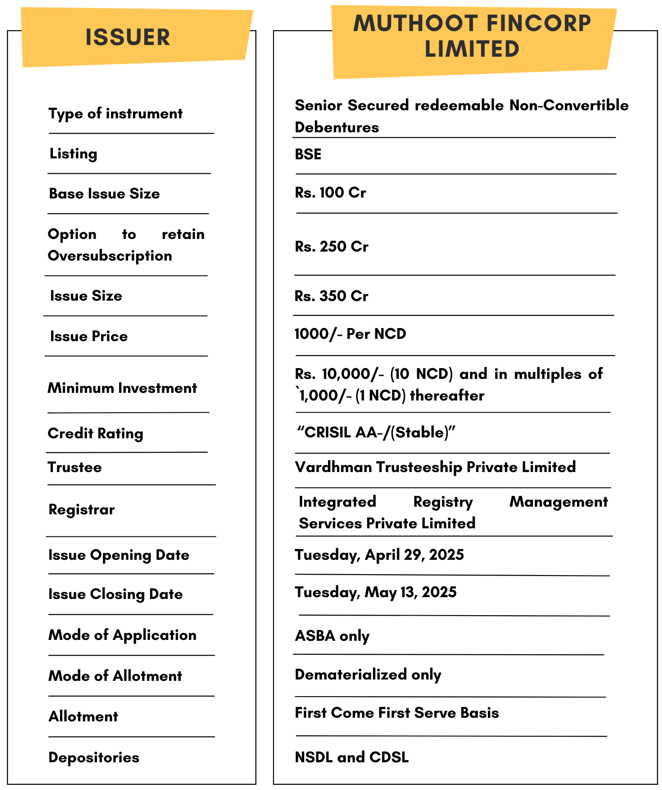

High Yield | AA-/Stable Rated | Minimum Investment: 10k Only

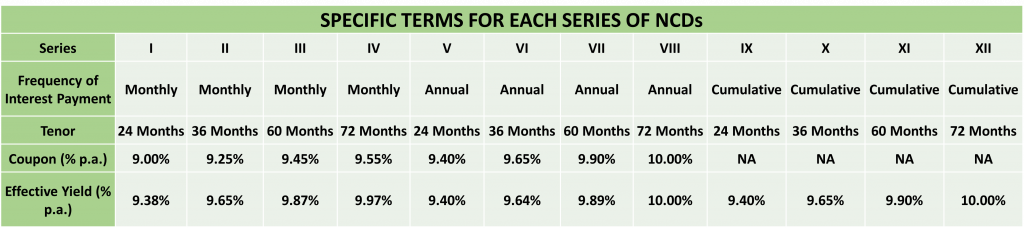

Muthoot Fincorp Ltd is issuing Non-Convertible Debentures. These NCDs are AA-/Stable by CRISIL. The NCDs are being issued in twelve series: yield ranges from 9.38% to 10.11% p.a. and different tenures of 24 months, 36 months, 60 months, and 72 months. The NCDs are secured and redeemable in nature.

Muthoot Fincorp Ltd NCD IPO: Coupon rates and effective yield for each of the series

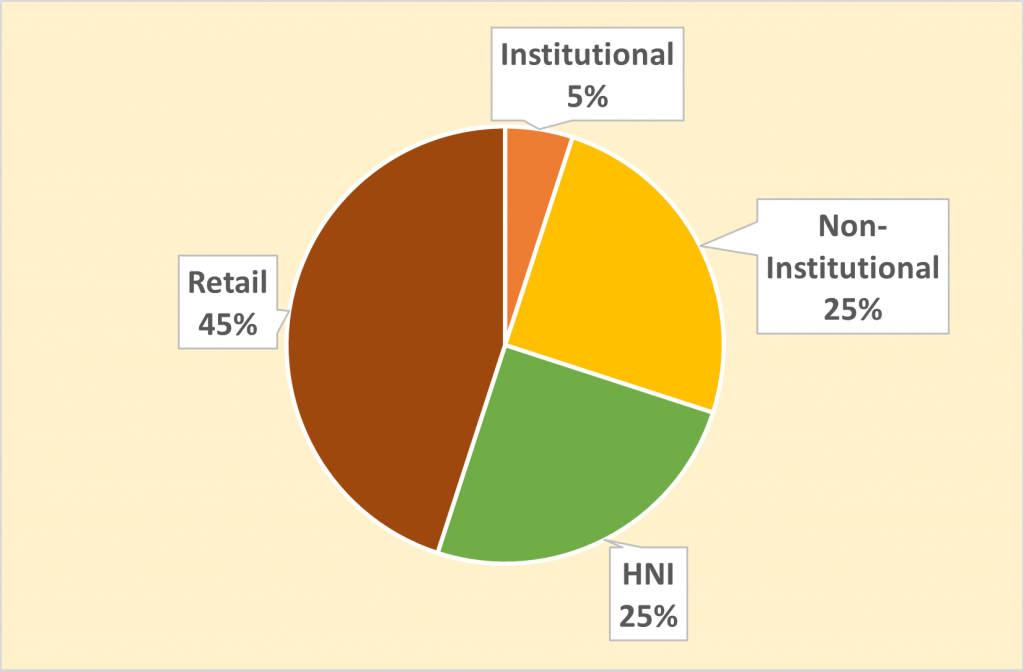

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Muthoot Fincorp Ltd NCD-IPO.

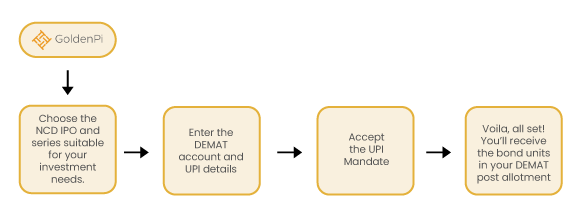

Investment Process for Muthoot Fincorp Ltd NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

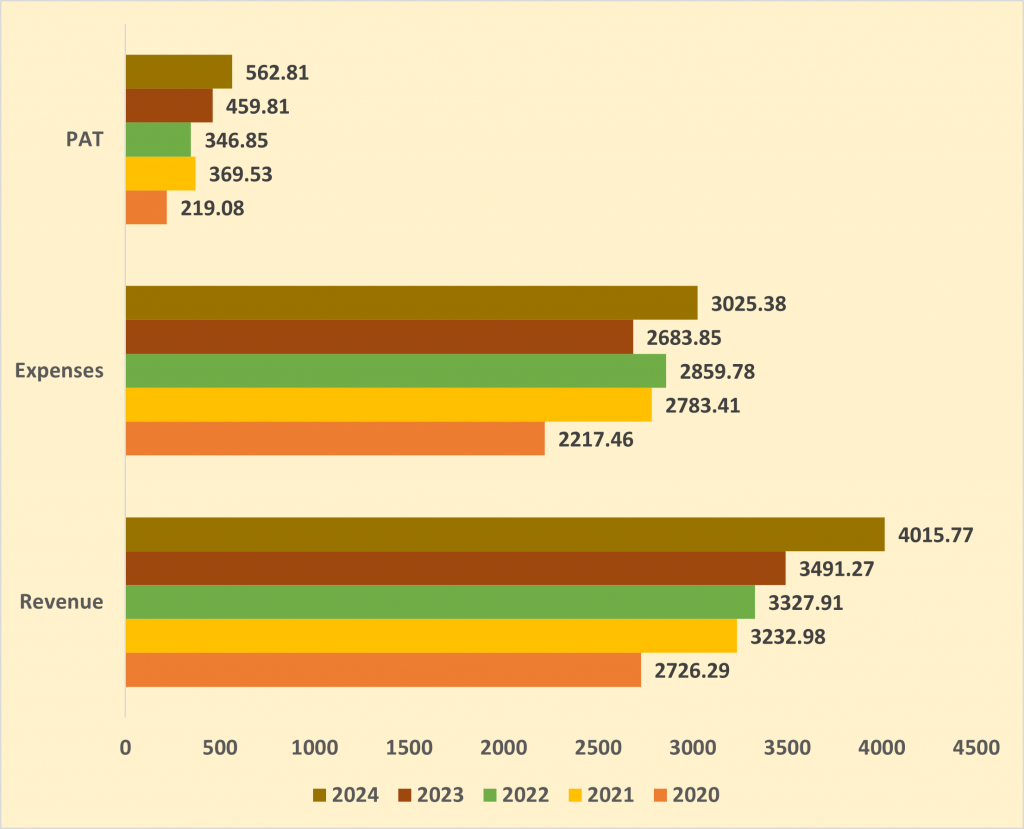

Financial Overview

Snapshot stating the Revenue, Expenses, EBIT, Net Worth and P AT

(Amount in Rs. Cr)

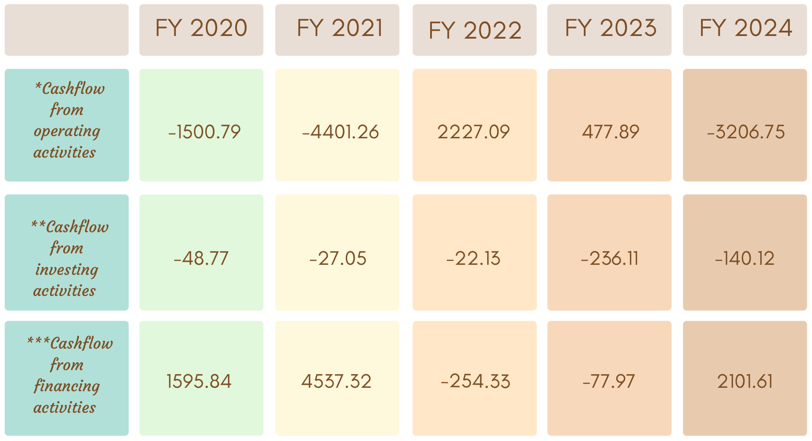

Cash flow for last 5 years

(Amount in Rs. Cr)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

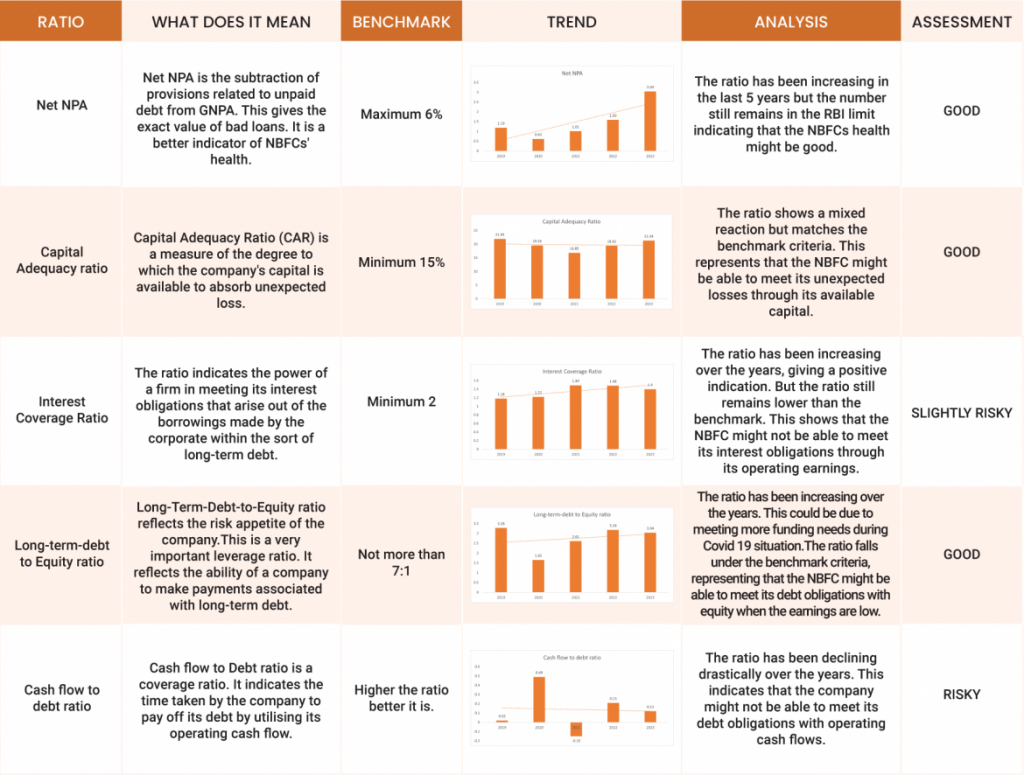

Ratio Analysis

Issue analysis

Pros

- Strong Credit Rating: Rated CRISIL AA-/Stable, indicating high degree of safety and low credit risk.

- Robust Parentage: Part of the Muthoot Pappachan Group, a well-established financial services conglomerate.

- Extensive Reach: Over 3,600 branches across India ensures strong customer base and rural presence.

- Secured NCDs: Backed by a subservient charge on loan receivables and current assets, offering security to debenture holders.

- Reasonable Financial Metrics: FY24 total income of ₹4,294 Cr; PAT of ₹268 Cr; Net Worth of ₹2,726 Cr.

Cons

- Exposure to Gold Loan Volatility: A large portion of business still depends on gold loan pricing and demand cycles.

- Asset Quality Pressure: Any adverse movement in collateral value (especially gold) could impact collections.

- Interest Rate Risk: High interest rate environment could affect borrowing costs and NIM (Net Interest Margin).

- Moderate Capitalisation: While comfortable, the capital adequacy ratio (CAR) needs constant monitoring as business scales.

Liquidity Position

- Healthy Liquidity Buffer: MFL retains daily cash buffers across branches (up to 0.5% of gold loan book or ₹2 lakh) to support disbursements.

- Comfortable Liability Structure: No breach of covenants reported; strong treasury management via centralized fund transfer mechanism ensures fund availability.

- Recent Upgrades in Credit Rating: CRISIL upgraded MFL’s long-term rating to CRISIL AA-/Stable and short-term rating to CRISIL A1+, enhancing its access to capital markets

About MFL

Founded in 1997, Muthoot Fincorp Ltd.(MFL) is a non-deposit taking, one of the leading NBFCs in the country. The NBFC primarily deals into lending against gold jewelry. It is the flagship company of the Muthoot Pappachan Group also popularly known as the Muthoot Blue Group, which has diverse business interests such as hospitality, real estate, and power generation.

Strengths

- Strong Market Position in Gold Loans: One of the largest gold loan NBFCs in India, with a well-established brand presence, especially in South India.

- Healthy Asset Quality: GNPA (Stage 3 assets) improved to 1.40% as of Dec 31, 2024, from 2.88% in FY22, reflecting strong underwriting and collection efficiency.

- Robust Capital Adequacy: CRAR stood at 18.20% as of Dec 31, 2024, well above the RBI-mandated 15%, indicating a strong capital buffer.

- Diversified Financial Services Group: Through subsidiaries like Muthoot Microfin and Muthoot Housing Finance, the company taps into microfinance and affordable housing.

- Widespread Distribution Network: Large physical presence across India, especially in underserved markets, giving it a significant competitive edge.

Weakness

- Asset-Liability Mismatch: The company’s average asset tenor is 4–12 months, while liabilities are longer-term, exposing it to rollover risks in case of funding crunches.

- Brand Dependency & Legal Risks: Trademark registration for “Muthoot Fincorp” and “Muthoot Pappachan” is still pending; any disassociation from the group could impact operations.

- Moderate Exposure Concentration: Top 20 borrower exposure stood at 1.66% of total, and the top 4 NPAs accounted for ₹934 crore, hinting at some concentration risk.

- Reliance on Short-Term Borrowing: High dependency on working capital loans and CPs may pressure liquidity in stressed times.

Source- Tranche V Prospectus April 23, 2025

Disclaimer- The information is published as on date 4/30/2025 based on information available on Tranche V Prospectus April 23, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors