While there are bonds available on the market to generate a fixed income, there is one unique thing to consider, and it is referred to as a securitized bond. This is one of the most commonly preferred options as these are backed by a mortgage, and owing to this fact, it is often considered a relatively secure investment.

Although the process is called securitization, there is an entire story behind it! Read on to learn about securitization and why to go for securitized bonds.

What is securitization?

Securitization simply states, “It is a process of pooling the various financial assets in the same category and selling them to other financial services to issue securitized bonds.”

All similar kinds of financial assets are being categorized and converted into market security. The assets are illiquid, such as mortgages, which are converted into liquid cash by the end of the process.

It might still be complicated with a liner to comprehend securitization, but there is groundbreaking ideation behind the entire process that brings about a win-win situation for all the financial institutes that are involved in it. Let’s wrap around it in detail.

The Background Approach

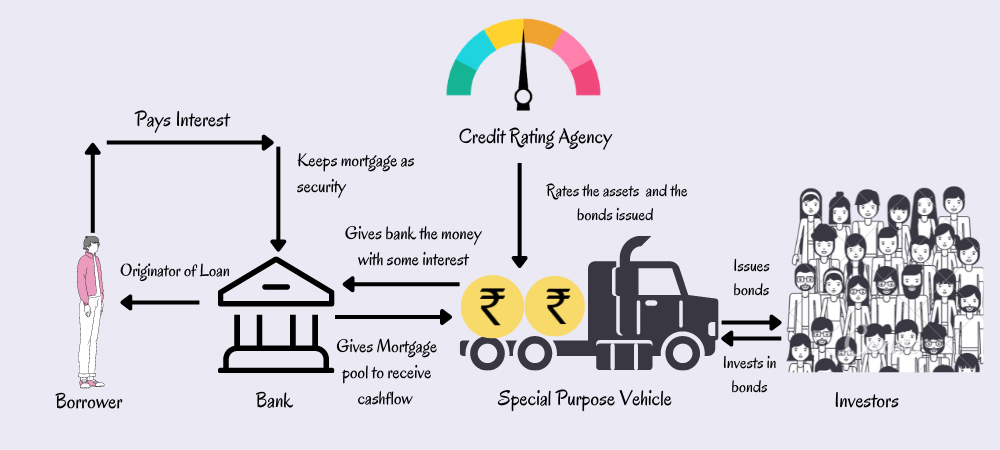

An example in this illustration considers a bank and a credit rating agency as the financial institutes, and the borrowers and investors as the people.

As a borrower, when in need of money, it’s a norm to go to a bank and borrow money in exchange for keeping collateral as security. Collateral, in this case, is a “mortgage.”. That’s something you’re certain to go through as a borrower.

But while the bank lends money to every individual, it runs out of cash flow at some point. To keep lending money to the borrowers, it need to have money. But have you ever encountered a situation where the banks say “no”? Read on to learn about its next approach with the cash flow it arranges to continue with its operations.

The Bank’s Next Approach

At any point in time, the bank is not in a position to say, “No, I can’t lend you anymore!” as the bank’s operations would be badly affected. An alternative way out of this is to leverage the mortgage pool.

What is a mortgage pool?

Collectively accumulated mortgages by the bank from the borrowers as collateral are a mortgage pool. In other words, they are called “title deeds.”

They are illiquid assets that can’t be converted into cash. The “Special Purpose Vehicle” comes into play, which offers extended help to the banks in lending money so that they can continue lending money to the borrowers.

How will special-purpose vehicles (SPV) offer money?

The point is how would SPV (Special Purpose Vehicle) get money? Here’s an interesting catch for the bondholders to know.

The credit rating agency checks the risks of all the assets that the bank has in the mortgage pool, and based on this, the SPV lends money to the bank with some interest. This is the point when the SPV issues bonds against the mortgage.

Bonds that are backed up by securities are called securitized bonds, and the process that goes into issuing bonds by keeping mortgages as securities is called securitization.

A Quick Guide to the Bond Investment Process for Retail Investors

Why would investors buy bonds?

The bonds are categorized accordingly by the CRA (Credit Rating Agency) into AAA, AA, and A bonds. AAA-rated bonds have a lower risk and interest rate, and A-rated bonds are considered high-risk bonds with higher interest rates. The higher the interest rates, the better the returns, but as always, it comes with higher risk, and it is up to one’s risk appetite to opt for it. And most of all, it is backed by a mortgage pool.

How to analyse the creditworthiness of corporate bonds?

These bonds look like an appealing investment for investors, as they can potentially make good returns for them. That is the way for SPV to collect money from the bank. The bank takes the money and pays it back with interest to the SPV over a period of time.

That’s about the concept of securitization and the ones involved in the process made their way to what was awaited.

Closing Thoughts!

The bottom line is that a financial institution and the investors involved in this process make their way to expected cash flow and returns through securitization.