Total Deposits held through Corporate fixed deposits by NBFCs are Rs. 66,443 Cr as reported in September 2021.

What are Corporate Fixed Deposits?

In India, the most popular form of investing is the fixed deposit. Similar to banks, the RBI allows selected corporations and NBFCs to receive deposits with a set interest rate and term. These are referred to as Company or Corporate Fixed Deposits.

Corporate FDs provide investors with stable, predictable returns in these times of high market volatility and uncertain returns, helping them in securing their financial future. Investors have an option between a pay-out option that provides a steady income and a cumulative option that builds money.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowWhat should you keep in mind when choosing a company fixed deposit?

- Safety Ratings

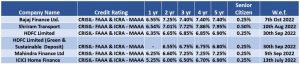

It is important to choose higher-rated corporate FDs depending on their credit rating. Credit Rating shows the credit worthiness of the company i.e. if the company will be able to meet its obligations or not. For instance- If there are 2 companies offering corporate Fixed deposits with different ratings. It is always recommended to choose the one which has a higher rating.

It is recommended to choose Company A, as per the information given in the above table.

- Past Repayment History

Before making any investment decision it is always suggested to look into the company’s repayment history whether the company has made the timely payments or not. This feature influences the company’s credit score, reputation, and stability.

For Instance, if company A has made timely interest or principal payments in the past, whereas company B has defaulted on any of its payments, it is always suggested to opt for Company A, even after paying a lower interest rate. This is because at least there will be an assurity of getting your money back and a less risk attached to it.

- Business Background

Analyze a company’s financial statements, management discussion and analysis(MD&A), and other documentation to determine its commercial viability. Apart from credit ratings and the repayment history it is very important to check the background of the company. Checking the background of the company might help you to analyse the financial standing of the company in the market.

For example, company A has a stronger management but its profits are declining from past 5 years as well as the cash flows, whereas Company B doesn’t have a very strong management but has been growing consistently from past 5 years which is shown in the balance sheet of the company. In such a scenario it is advised to invest in Company B instead of A.

Why to invest in Corporate FDs?

- Get Fixed and Predictable returns – Due to market activities, interest on securities might fall or rise. But with Corporate FDs, interest remains fixed therefore, it would not decrease because of a few factors. For instance, if an investor invested in an corporate FD of 6.25% in 2019 maturing after 2 yrs, would still yield out its interest in 2021. Even After the situation was adverse and the country was hit by covid-19 when all the markets were turning negative.

- Compounding Interest – If an investor has invested in cumulative fixed deposits, he/she can earn upto 9% to 10% by the end of maturity with the help of compounding. With compounding investors can earn interest on the amount invested as well as on the interest received over it.

- Flexible investment tenure and Interest payment frequency – To plan long and short term financial plans, there is a wide range of flexible tenure made available to the investors ranging from 1 to 5 years. For example, Bajaj Finance would have a corporate FD that would mature in 1 yr, 2 yr, 3 yr, 4 yr and 5 yr with different rate of interest, whichever suits the need of an investor, they can subscribe to it.

- Liquidity in times of Emergency – These Corporate FDs can also be used in the times of need to avail loans against it. Also they can be liquidated in times of need.

Taxation process for Corporate/Company FD

It is better to avoid being startled by a high tax bill at the end of the year. It’s important to comprehend your current tax obligations and how your FD will affect them in the future.

In the event that your income exceeds Rs 5,000 in a fiscal year, the interest you earn on Corporate FDs is subject to taxation according to your income tax bracket.

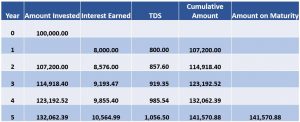

Let’s use an easy example to better grasp this. For instance, if an investor intends to invest Rs. 100,000 in a CFD with a 5-year term yielding 8% cumulatively and he is subject to a 10% income tax rate. The below table shows the earnings as well as the tax deduction made every year.

Investors can request the TDS waiver if they are an Indian resident and have no taxable income overall by filing Form 15G or 15H. (for senior citizens).

There are a few considerations one should make when it’s time to withdraw money from there fixed deposit:

- Interest earned on maturity: Upon Maturity, before 1 year from the date of commencement

- Interest earned on premature withdrawal (before maturity):

Do Corporate FDs carry higher risk?

Many investors are worried about losing money if the company they are investing in defaults because corporate FDs are unsecured. It is crucial to remember that all NBFCs and businesses who want to accept deposits must comply by the strict rules and regulations set by the RBI and the Ministry of Corporate Affairs (MCA). Due to this, only a few out of India’s more than 10,000 NBFCs are permitted to accept public deposits. By complying with these steps, investors’ exposure to risk when investing in corporate Fixed Deposits is minimised.

Credit Rating

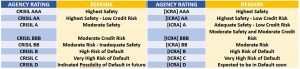

Credit rating organisations including CRISIL, ICRA, and India Ratings & Research regularly rate the safety of NBFCs. Moreover, NBFCs that at least have a BBB rating are authorized to raise funds through Corporate FDs. The table below shows the degree of safety for each rating.

How are Corporate Fixed Deposits different from other Debt Instruments?

What is the basic process of premature withdrawal?

The basic process of premature withdrawal of Corporate fixed deposits on an online basis would require the soft copies of the documents stated below:

- Submit the original FDR Certificate with all holders signature;

- Submit a Canceled cheque;

- Request letter from client for premature withdrawal with reason (All Holders Signature).

When can a client apply for premature withdrawal?

Investors that meet certain requirements can ask for an early withdrawal. Premature withdrawals are not permitted before three months have passed from the date of deposit. The accompanying rates table will be in effect if a request for an early withdrawal is filed after the first three months have expired.

- After 3 months but before 6 months: For individual depositors, the maximum interest due shall be 4% annually; for all other depositor categories, there shall be no interest charged.

- After 6 months but before maturity date: The interest payable is 1% less than the interest rate applicable during the deposit period. If no rate has been set for that time period, it will be 2% less than the minimum rate at which HDFC and other banks will take public deposits.

The Guidelines of RBI that NBFCs Should Follow for Launching Fixed Deposits:

- A fixed deposit must have a minimum duration of one year and a maximum tenure of five years.

- The interest rate on fixed deposits must not be higher than the limit set by the Reserve Bank of India. The RBI occasionally changes this interest rate.

- An NBFC may only collect as many fixed deposits as is permitted by law; however, this again differs among NBFCs.

- An NBFC is required to provide RBI with all pertinent information regarding fixed deposits.

- NBFCs are prohibited from giving their depositors any further gifts or incentives.