|

Getting your Trinity Audio player ready...

|

Fixed deposits (FDs) have long been India’s most trusted savings instrument. But in recent years, Small Finance Banks (SFBs) have emerged as a unique category of banks that not only cater to underserved segments but also offer FD rates far higher than large commercial banks.

This blog dives deep into how SFBs operate, why they can afford to pay higher FD rates, what risks investors should keep in mind, and how to make the most of these opportunities.

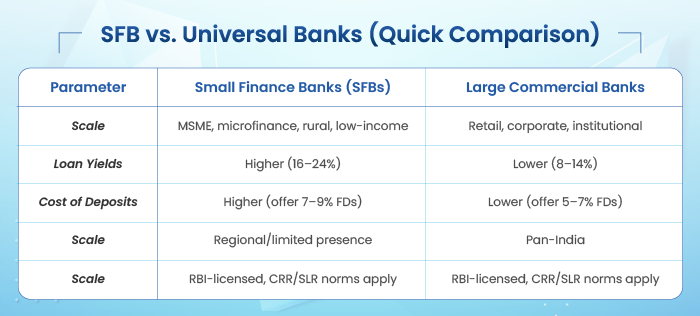

What Are Small Finance Banks?

SFBs were introduced by the Reserve Bank of India (RBI) in 2015 to further financial inclusion. Their mandate is to:

- Provide credit to MSMEs, small traders, farmers, and lower-income households.

- Mobilize deposits from the public like any other scheduled commercial bank.

- Maintain regulatory discipline (CRR, SLR, capital adequacy).

Today, there are 12 licensed SFBs in India, including AU SFB, Ujjivan SFB, Equitas SFB, Jana SFB, ESAF SFB, and others.

Key takeaway: SFBs are like “focused specialists” in banking—serving niche segments and balancing their higher lending yields with higher deposit costs.

Why Do SFBs Offer Higher FD Rates?

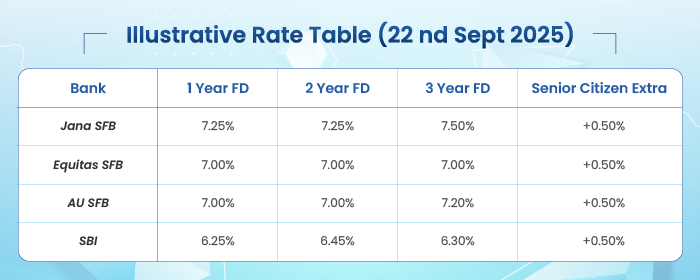

While HDFC Bank or SBI typically offer 6–7% on FDs, SFBs like Jana SFB, Equitas SFB, or ESAF SFB often advertise 8–9.25% for retail depositors, sometimes higher for senior citizens.

Reasons Behind Higher Rates

- Aggressive Liability Growth: As newer banks, they must attract deposits quickly to build balance sheets.

- High-Yield Assets: They lend to MSMEs, gold loans, and microfinance borrowers at 16–24%, allowing them to afford higher deposit payouts.

- Brand-Building Premium: To compete with trusted giants like SBI or ICICI, they offer rate premiums of 100–250 bps.

- Targeted ALM Strategy: Special FD schemes (777 days, 999 days) align with their loan book durations.

For investors, this means better returns but also higher risk compared to large banks.

How the FD Ecosystem Works in SFBs

When you book an FD with an SFB, here’s what happens:

- Products: Range from 7 days to 10 years. Options include cumulative (interest reinvested) or non-cumulative (monthly/quarterly payouts).

- Rates: SFBs often give 0.5–1% extra for senior citizens and “special tenure” schemes.

- Insurance: Deposits are insured by DICGC up to ₹5 lakh per depositor per bank.

- Premature Closure: Allowed but with penalties (~1%).

- TDS: Interest is fully taxable at your slab rate; TDS applies above thresholds unless Form 15G/15H is submitted.

Example:

If you place ₹5 lakh in a 2-year FD at 9% in Jana SFB, you earn:

- Maturity Value (cumulative option) ≈ ₹5,98,600.

- In SBI at 6.8%, the same FD would grow to ≈ ₹5,72,400.

- Extra gain: ₹26,200—just for choosing an SFB.

How SFBs Make Money (Business Model)

SFBs’ business model is simple but high-yield:

Revenue Sources

- Interest Income: Loans to MSMEs, microfinance borrowers, gold loans, vehicle loans (yielding 16–24%).

- Fee Income: Insurance distribution, remittances, payments, loan processing.

Costs

- Interest Expense: High FD and savings rates (7–9%).

- Operating Expense: Smaller branches, digital onboarding.

- Credit Costs: Provisions for defaults (higher than universal banks).

Simplified P&L Bridge (Illustration)

- Loan yield: 18%

- Cost of deposits: 7.5%

- Net Interest Margin (NIM): ~10.5%

- Minus opex & credit costs → RoA of 1.5–2.5%, healthy for a bank.

Benefits to Investors Choosing SFB FDs

- Higher Rates: 8–9.25% vs 6–7% in big banks.

- Flexibility: Multiple payout options, senior citizen add-ons.

- Regulatory Oversight: RBI-regulated; deposits insured up to ₹5 lakh.

- Diversification: Opportunity to spread savings across different banks/tenors.

Risks & Weaknesses

- Geographic/Segment Concentration: Many SFBs have 60–80% loans in 1–2 states.

- Credit Risk: MSME and microfinance loans are riskier—GNPA often 2–4%, higher than large banks.

- Capitalisation Needs: Rapid growth requires fresh capital to maintain CRAR.

- Rate & Liquidity Risk: If rates fall, reinvestment yields drop.

- DICGC Limit: Only ₹5 lakh insured—so don’t put all eggs in one basket.

Solution: Spread deposits across multiple SFBs, keep each deposit ≤ ₹5 lakh.

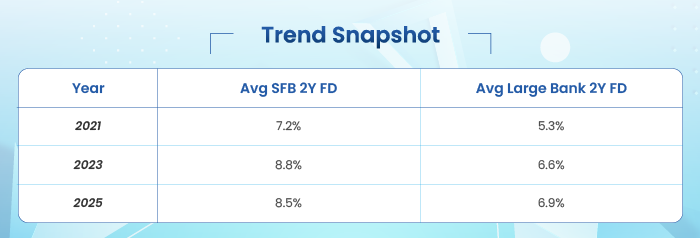

Interest Rate Trends

- 2020–21 (Pandemic): SFBs offered 7–8% even when large banks dropped to 5–5.5%.

- 2022–23 (Tightening): SFBs raised to 8.5–9%; some offered >9.25% special rates.

- 2025 Outlook: As RBI normalizes, expect SFB rates to hover 50–150 bps above large banks, adjusting with liquidity cycles.

Checklist for Investors Before Choosing SFB FDs

- Confirm RBI-licensed Scheduled Commercial Bank status.

- Check CRAR >15%, GNPA <3%, consistent profitability.

- Split deposits across 2–3 banks, ≤₹5 lakh each.

- Prefer short-to-mid tenors (1–3 years) for flexibility.

- Understand penalties for premature withdrawal.

Who Should Invest in SFB FDs?

- Ideal for: Senior citizens, conservative investors, and short-to-mid term savers seeking guaranteed returns.

- Not ideal for: High net-worth individuals with >₹25–30 lakh in FDs (DICGC limit becomes restrictive), or investors who prefer liquidity and tax efficiency of debt funds.

Taxation

- FD interest is fully taxable at slab rate.

- TDS applies above ₹40,000 (₹50,000 for senior citizens).

- Compare post-tax returns vs. debt mutual funds, especially if you’re in the 30% bracket.

Conclusion

Small Finance Banks have added vibrancy to India’s financial ecosystem. Their FDs offer a compelling yield advantage, but investors must weigh returns against risks, and always stay within DICGC limits. With smart laddering across tenors and banks, SFB FDs can be a valuable tool in your fixed-income portfolio.

In short: Higher returns, manageable risks—if you play it smart.