|

Getting your Trinity Audio player ready...

|

Introduction to the Sovereign Gold Bond Scheme

Investing in gold has long been a cornerstone of wealth preservation and financial security. However, navigating the physical gold market can be cumbersome and involve storage concerns. Enter the Sovereign Gold Bond Scheme (SGB), a revolutionary initiative by the Government of India that offers a safe, convenient, and government-backed way to invest in gold.

The SGB Scheme, a government-backed initiative, is designed to encourage individuals to invest in gold bonds rather than physical gold. These bonds are available in different series, with Series III being the latest. Investors gain an edge with these bonds, as they offer an attractive combination of security and returns.

Understanding the Features and Benefits of Series III of the Sovereign Gold Bond Scheme 2023-24

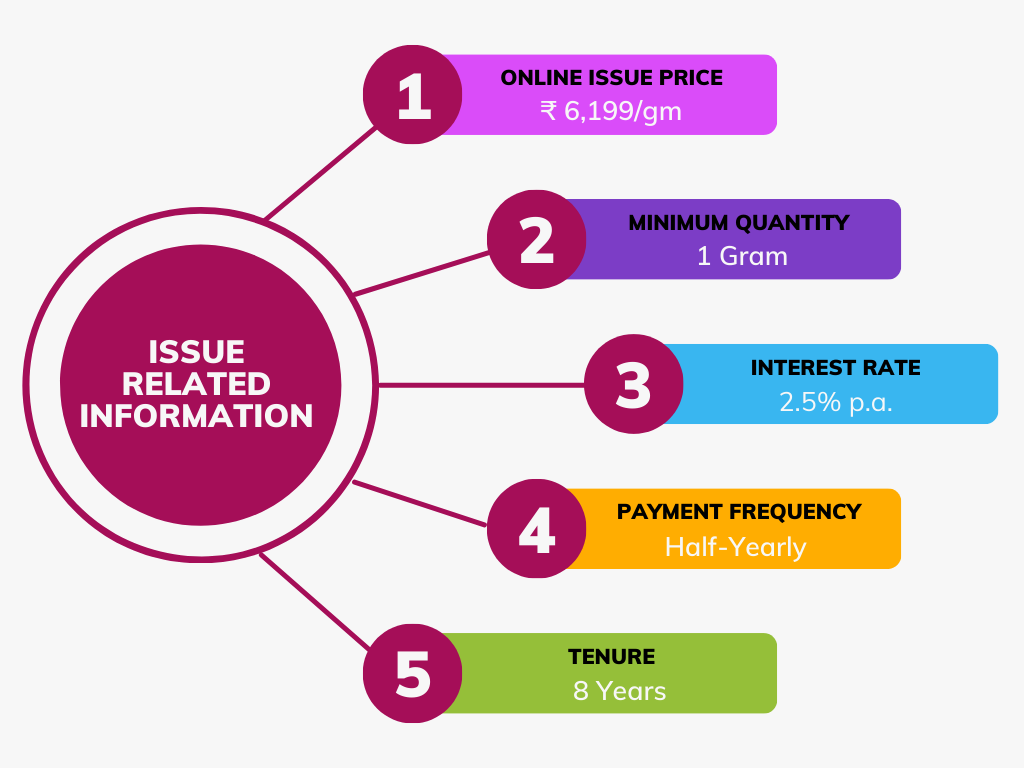

Key Features of Series III SGBs:

- Investment Unit: Each bond represents 1 gram of gold.

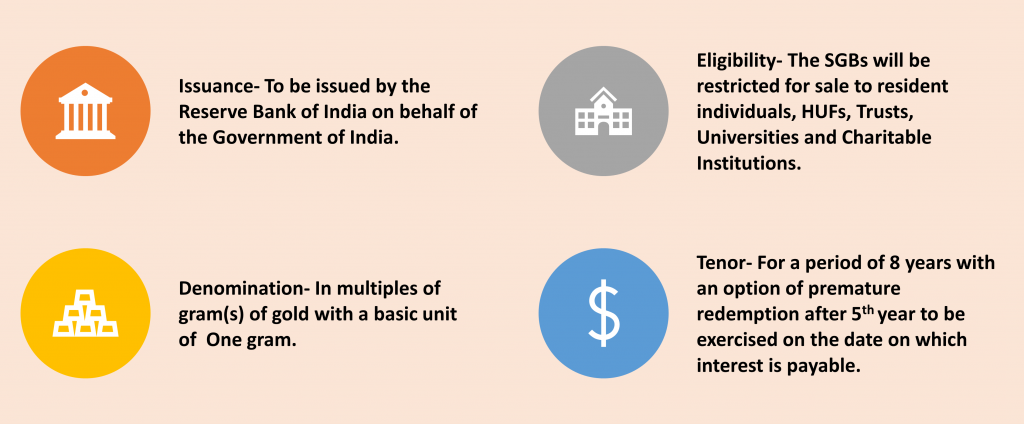

- Subscription Price: The subscription price is determined by the Reserve Bank of India (RBI) based on the average closing price of gold for the preceding week.

- Gold Bond Interest Rate: Series III SGBs offer a fixed interest rate of 2.5% per annum, payable semi-annually.

- Tenure of Investment: The tenure of the bond is 8 years, with an option to prematurely redeem after the 5th year.

- Minimum and Maximum Investment: Individuals can invest a minimum of 1 gram and a maximum of 4 kg of gold per fiscal year.

- Eligibility Criteria: Individuals, Hindu Undivided Families (HUFs), trusts, universities, and charitable institutions are eligible to invest in SGBs.

Subscription and Investment Details

- Investment Limits: An investor can subscribe to a minimum of 1 gram and a maximum of 4 kilograms of gold per fiscal year in the case of HUFs and individuals whereas trusts and similar entities have a higher limit of 20 kilograms. In case of joint holding, the investment limit of 4 Kg will be applied to the first applicant only.

- Tax Treatment: The provisions of the Income Tax Act of 1961 (43 of 1961) apply to the taxation of interest on SGBs. On the redemption of SGB to an individual, there is no capital gains tax due. Long-term capital gains resulting from the transfer of the SGB to any individual shall get the indexation benefits.

- Payment Option- Through cash payment (upto a maximum of ₹20,000) or demand draft or cheque or electronic banking.

Benefits of Investing in Series III SGBs:

- Safety and Security: Backed by the Government of India, SGBs offer unparalleled safety and security, making them a low-risk investment option.

- Guaranteed Returns: In addition to potential capital appreciation linked to gold prices, you receive a fixed interest rate, ensuring steady returns.

- Tax Advantages: Interest income is fully taxable, but capital gains are exempt from tax if the bonds are held until maturity, providing significant tax benefits.

- Flexibility and Liquidity: SGBs can be traded on secondary markets, offering exit options and liquidity before maturity.

- Convenience of Demat Form: Eliminates the need for physical storage and associated costs. SGBs are held electronically in your Demat account, ensuring ease and security.

Tax Implications and Exemption on Investments Made through the Sovereign Gold Bond Scheme

Tax Treatment of Interest Income:

- The fixed interest rate of 2.5% per annum earned on SGBs is fully taxable as income from other sources.

- This income is taxed according to your individual tax slab.

- TDS (tax deducted at source) is not applicable on interest income.

Taxation of Capital Gains:

- Capital gains arising from the redemption of SGBs are exempt from tax if the bonds are held until maturity (8 years).

- This incentivizes long-term investment and capital appreciation.

- If the bonds are redeemed before maturity, capital gains are calculated as the difference between the redemption price and the issue price.

- These gains are taxed as short-term capital gains according to your individual tax slab.

Tax Treatment on Premature Redemption:

- If you redeem your SGBs after the 5th year but before maturity, you will be subject to short-term capital gains tax on the accrued capital appreciation.

- However, no tax is levied on the interest income earned during this period.

Strategies for Optimizing Tax Benefits:

- Hold SGBs until maturity: Maximize tax benefits by enjoying the exemption on capital gains.

- Stagger your investments: Invest in SGBs across different series to spread out your tax liability over time.

- Consult a tax advisor: Seek professional guidance for personalized tax planning strategies.

Risks Associated with Investing in the Sovereign Gold Bond Scheme and How to Mitigate Them

Potential Risks Associated with Series III SGBs:

- Gold Price Fluctuations: Like any commodity, the price of gold is subject to market fluctuations. While SGBs offer a hedge against inflation in the long run, a decline in gold prices could result in capital losses upon redemption before maturity.

- Liquidity Issues: Compared to physical gold, SGBs offer limited liquidity. While they can be traded on secondary markets, the trading volume might be low, potentially leading to delays and price discrepancies.

- Interest Rate Risk: While SGBs offer a fixed interest rate, changes in market interest rates could impact the overall attractiveness of the scheme compared to other investment options.

Strategies to Mitigate Risks:

- Long-term Investment: Invest in SGBs with a long-term perspective (8 years) to benefit from potential gold price appreciation and enjoy the tax exemption on capital gains.

- Diversification: Diversify your portfolio across different asset classes to mitigate the impact of gold price fluctuations on your overall wealth.

- Stagger Investments: Invest in SGBs across different series to spread out your investment risk and ensure exposure to different price levels.

- Monitor Market Conditions: Stay informed about market trends and gold price movements to make informed decisions about your investment.

- Consider Liquidity Needs: If you require immediate access to your funds, SGBs might not be the ideal investment option due to limited liquidity.

Conclusion: The Potential of Returns and Diversification that Investors can gain through Series III of the Sovereign Gold Bond Scheme 2023-24

Investing in Series III Sovereign Gold Bonds presents a unique opportunity to unlock the vast potential of gold. Enjoy long-term capital appreciation, earn a steady income, and benefit from tax advantages. SGBs offer security, convenience, and diversification, making them a valuable addition to any portfolio. Embrace the golden opportunity and invest in Series III SGBs today. Secure your financial future and unlock the path to wealth creation.