|

Getting your Trinity Audio player ready...

|

High Yield | Crisil AA/Stable & BWR AA+/Stable Rated | Minimum Investment: 10k Only

Bond overview:

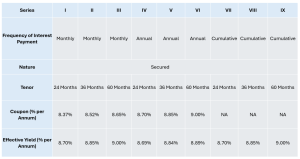

IIFL Finance Limited is issuing the Non-Convertible Debentures. These NCDs are AA/Stable by Crisil Ratings & AA+/Stable by Brickwork Ratings. The NCDs are being issued in nine series: yield ranges from 8.69% to 9.00% p.a. and different tenures of 24 months, 36 months and 60 months. The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series:

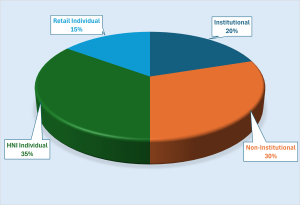

Allocation Ratio:

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for IIFL Finance Limited NCD-IPO.

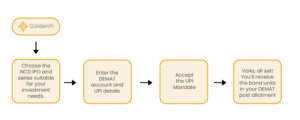

Investment Process for IIFL Finance Limited NCD IPO:

You can invest in IPOs via GoldenPi in 3 easy steps.

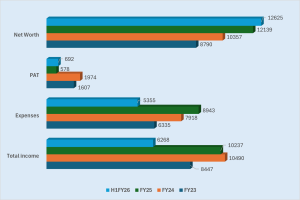

Financial Overview:

Snapshot stating the Total Income, Expenses, PAT and Net Worth ( In Crores):

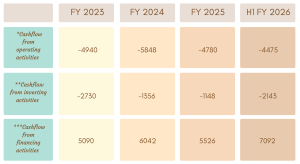

Cash flow for last few years ( In Crores):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

Ratio Analysis:

Issue analysis:

Pros:

- Strong Credit Rating: Rated Crisil AA/Stable and BWR AA+/Stable indicating high degree of safety and low credit risk.

- Secured NCDs: Senior, secured NCDs backed by First-ranking pari-passu charge by way of hypothecation of loan receivables.

- Security Cover: The security cover required must be a minimum of 100% of the total of the outstanding principal balance of the NCDs.

- Competitive yields: up to 9.00% vs bank FDs.

- Wide tenor and payout options: Monthly to cumulative

Cons:

- Exposure to stressed segments: Asset quality pressures persist in micro LAP, unsecured business loans and microfinance, leading to higher provisioning and write-offs.

- Interest Rate Risk: More pronounced in longer tenors (60months).

To get better returns than Bank FDs, invest in NCD-IPOs online.

About IIFL Finance Limited:

IIFL Finance Limited, formerly IIFL Holdings Limited, is a diversified NBFC headquartered in Mumbai that along with its subsidiaries – IIFL Home Finance Limited and IIFL Samasta Finance Limited – provides a diverse range of loan products, including gold loans, home loans, MSME secured loans, MSME unsecured loans, supply chain finance and microfinance loans, through a widespread branch network across India.

Founded by first-generation entrepreneurs Mr. Nirmal Jain and Mr. R.Venkataraman, the Company is backed by prominent institutional investors such as Fairfax Financial Holdings, Capital Group, Bank Muscat India Fund, Vanguard and Blackrock.

The Company operates a well-integrated physical and digital (“phygital”) platform, with nearly 4800 branches supported by robust online and mobile infrastructure. It serves over 46 lakh customers across business segments. As of Dec’25, the Company operates across 32 States/UTs, managing an AUM of nearly Rs 98,335 Cr.

Key Highlights:

Strengths:

-

- Strong Ownership: The promoters of the group held ownership of (24.9%) of the shareholding. The majority of ownership is held by institutional investors (52.1%) including Fairfax (15.2%), Capital group (7.9%), Vanguard (2.2%), Blackrock (1.2%), HSBC MF (2.1%), Abakkus (2%) and Mahindra Manulife MF (1%).

- Experienced management team: The company is spearheaded by a highly experienced leadership team, including Promoter & MD Mr. Nirmal Jain (30+ years in finance) and Co-Promoter & Joint MD Mr. R. Venkataraman (33+ years in finance). They are further supported by a skilled management team possessing significant experience in the financial services sector.

- Asset Light model: The Company operates on an asset-light model, collaborating with banks through direct assignment, securitization and co-lending arrangements. This approach aligns well with banks as most of its assets qualify under the RBI’s priority sector lending (PSL) norms or are zero risk weight for the banks. As of Dec‘2025, off-book assets totalled Rs 34,550 Cr, covering 35% of the total Asset Under Management.

- Strong Debt Partnerships: It maintains strong debt partnership with PSU banks (SBI, Bank of Baroda, Union Bank, Canara Bank), private sector banks (ICICI Bank, Federal Bank) and NBFCs (Bajaj Finance, Aditya Birla Capital).

- Diversified portfolio: The group has a diversified portfolio spread across 32 states/UTs of India consisting of different asset classes. AUM consisted of Gold loans (44.17%), Home loans (32.43%), Microfinance (8.50%), MSME Secured loan (9.26%), MSME unsecured loan (3.62%), Supply chain finance (0.43%), personal loan (0.08%), construction and real estate finance (1%) and Capital Markets financing (0.54%).

- Good growth in AUM: AUM grew by 26% to Rs 98,335 Cr as of Dec ’25 (9M-FY26) from Rs 78,341 Cr (FY25), driven by growth in Gold loan portfolio which grew by 107% to Rs 43,432 Cr in 9M-FY26 from Rs 21,021 Cr (FY25).

- Strong asset quality with consistent low level of NPAs: IIFL Finance Ltd. maintains strong asset quality, supported by a largely secured loan book (87.36% as of Dec ’25). Gross NPAs (GNPAs) improved to 1.60% in Dec’25 from 2.23% in Mar’25 and 2.32% in Mar’24, while net NPAs declined to 0.75% in Dec’25 from 1.05% in Mar’25 and 1.20% in Mar’24, reflecting sustained improvement in credit performance.

- Adequate Capitalisation Matrices: The company’s capitalization has been consistently supported by retained earnings, with the net worth standing at Rs 13,048 Cr. as of Dec’2025. The company-maintained cash and bank balance of Rs. 5,282 Cr, while its CRAR stood at 27.70%.

- Well Diversified Funding: IIFL Finance maintains a well-diversified funding profile with borrowings spread across Term loans (37.74%), NCDs (26.18%), Securitization (8.01%), Subordinated debt (8.01%) and CPs (17.35%).

-

- Strong Liquidity: The company maintained a liquidity buffer of Rs 9,433 Cr (free cash and undrawn lines) as of Dec ’25, with cash and bank balances of Rs 5,282 Cr. on a consolidated basis. As per the Dec ’25 ALM statement, cumulative mismatches remained positive across all buckets up to 5 years, reflecting strong liquidity management and low refinancing risk.

Weaknesses:

-

- Geographic concentration: 51.83% AUM depends on the top 5 states (Maharashtra – 16.38%, Gujarat- 13.19%, W.Bengal- 8.17%, Karnataka- 7.12%, Rajasthan- 6.97% ), exposing business to regional economic & political risks.

- Subsidiary-level asset quality risks: While IIFL Home showed improvement (GNPA 0.9% as of Dec ’25), IIFL Samasta continues to report elevated GNPA (~4.8%) due to industry-wide stress in the microfinance segment.

- Geographic concentration: 51.83% AUM depends on the top 5 states (Maharashtra – 16.38%, Gujarat- 13.19%, W.Bengal- 8.17%, Karnataka- 7.12%, Rajasthan- 6.97% ), exposing business to regional economic & political risks.

Invest in Bond IPO online in just 5 minutes

Source- Tranche I Prospectus February 12, 2026

Disclaimer – The information is published as on date 17/02/2026 based on information available on Tranche I Prospectus February 12, 2026. The information may be subject to change in case of change in terms of prospectus or any other reason as the case may be. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors