|

Getting your Trinity Audio player ready...

|

Introduction: The Rise of Digital Currencies

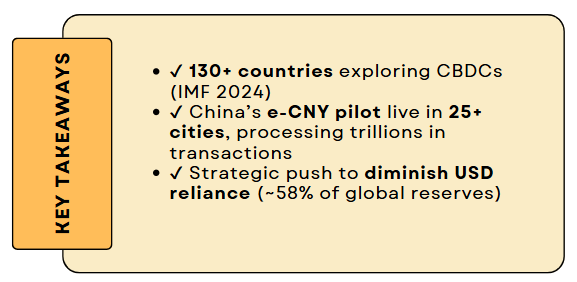

The financial world is undergoing a seismic shift as central banks worldwide accelerate their exploration of Central Bank Digital Currencies (CBDCs). According to the International Monetary Fund (IMF), over 130 countries are currently researching, piloting, or deploying CBDCs as of 2024—a staggering surge from just a handful a decade ago. This rapid adoption underscores the growing recognition of digital currencies as a strategic imperative in the modern economy.

Leading the charge is China, which has positioned itself at the forefront of the CBDC revolution with its Digital Yuan (e-CNY). The People’s Bank of China (PBOC) has expanded its pilot program to 25+ cities, processing billions of yuan in transactions, from retail purchases to cross-border trade settlements. The e-CNY is not just a technological experiment—it’s a calculated move to reshape global financial power dynamics.

Behind this global CBDC race lies a deeper geopolitical ambition: to challenge the USD-dominated monetary system. The U.S. dollar currently accounts for ~58% of global foreign exchange reserves (IMF 2024), giving America unparalleled influence over trade and sanctions. CBDCs, particularly those backed by major economies like China, could erode this dominance by offering faster, cheaper, and more sovereign-controlled alternatives to traditional dollar-based transactions.

As nations jostle for leadership in this digital financial frontier, the question is no longer if CBDCs will redefine money—but how soon, and with what consequences for the existing global economic order.

What is the Digital Yuan (e-CNY)?

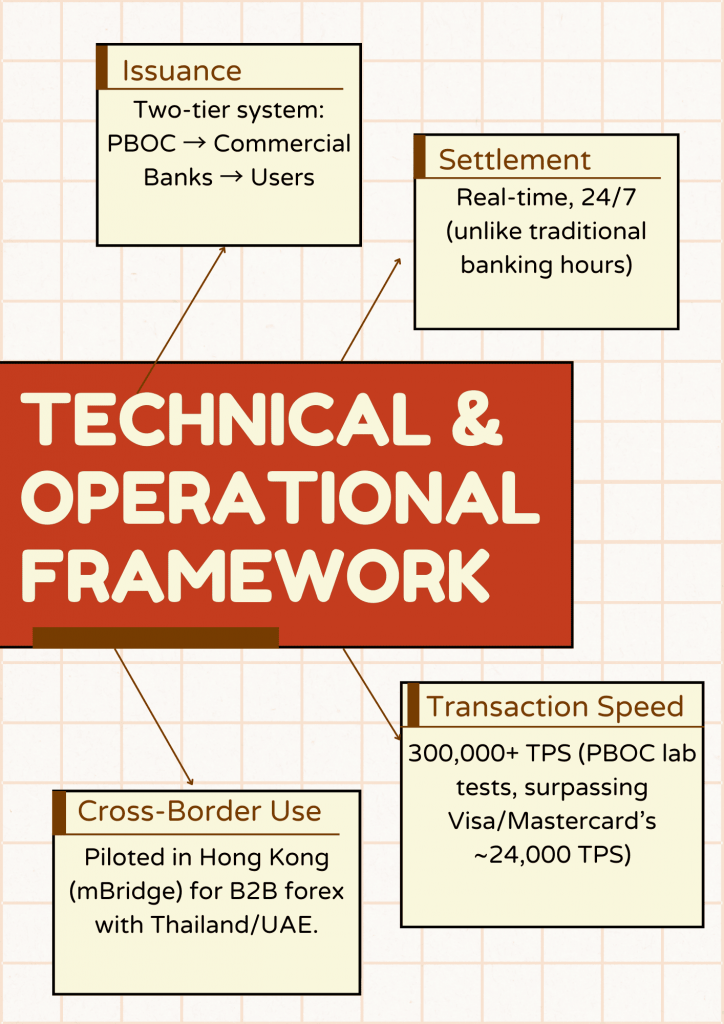

The Digital Yuan (e-CNY), officially known as the Digital Currency Electronic Payment (DCEP), is China’s sovereign digital currency issued by the People’s Bank of China (PBOC). As the world’s most advanced central bank digital currency (CBDC) in large-scale testing, it represents a state-controlled digital alternative to physical cash, designed to modernize payments while strengthening monetary policy oversight.

Core Characteristics of the e-CNY

1. Centralized & Sovereign-Backed Digital Currency

- Unlike decentralized cryptocurrencies (Bitcoin, Ethereum), the e-CNY is fully centralized, with the PBOC controlling issuance, distribution, and monetary policy.

- Legal tender status: Equivalent to physical RMB, ensuring universal acceptance.

- No interest-bearing: Designed primarily for transactions, not savings (unlike bank deposits).

2. Hybrid Wallet Infrastructure

- Operates through official e-CNY wallets and integrated commercial bank apps (ICBC, ABC, etc.).

- Interoperable with Alipay & WeChat Pay (which process ~90% of China’s mobile payments).

- 260 million+ individual wallets opened as of Q1 2024 (PBOC data).

3. Programmable Money & Smart Contracts

- Supports conditional payments:

- Expiry dates: Used in $30M+ of Shenzhen’s 2023 consumption vouchers.

- Targeted subsidies: Rural healthcare subsidies released only for medical services.

- Potential for corporate use: Automated tax payments, supply chain financing.

4. Real-Time Transaction Monitoring

- Full PBOC visibility: Every transaction recorded on a permissioned blockchain.

- Anti-fraud & AML: Enabled by AI-driven analytics to flag suspicious flows.

- Privacy concerns: “Controlled anonymity”—small transactions are pseudonymous, but identities are linked to banks.

5. Offline Payment Capability

- Breakthrough feature: Works without internet via NFC/Bluetooth (“touch-and-go”).

- Critical for:

- Rural areas (~300M Chinese still lack stable internet).

- Emergency payments (natural disasters, network outages).

Why Does the e-CNY Matter?

- Domestic Control

- Reduces reliance on Alipay/WeChat duopoly (~$50T annual payment volume).

- Prevents private stablecoins (e.g., USDT) from undermining monetary policy.

- Global RMB Push

- Aims to boost yuan internationalization (currently just 2.8% of global payments, SWIFT 2024).

- mBridge project could bypass SWIFT for $5T+ annual China trade.

- USD Challenge

- Potential to erode dollar’s 58% reserve currency share by offering a state-backed digital alternative.

How is the Digital Yuan Valued?

The Digital Yuan’s Fixed Valuation Framework

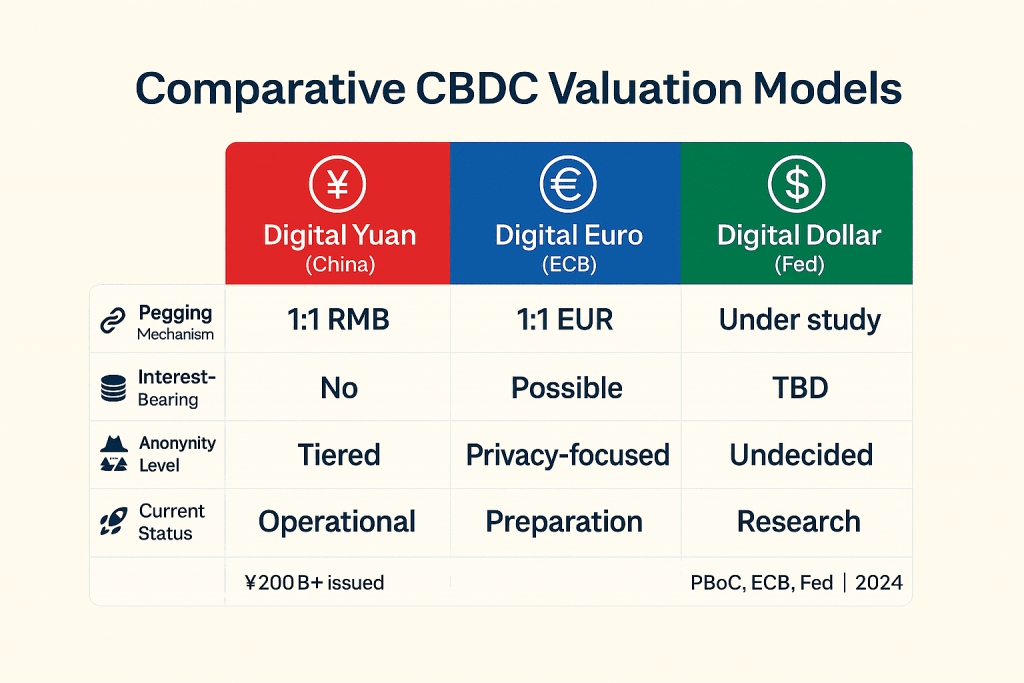

The Digital Yuan (e-CNY) maintains a strict 1:1 parity with China’s physical renminbi (RMB), making it fundamentally different from both traditional cryptocurrencies and other central bank digital currencies (CBDCs). This valuation model serves as the bedrock of its design philosophy:

1. Sovereign-Backed Stability

- Direct PBOC liability: Each e-CNY unit represents a direct claim on the People’s Bank of China

- Zero volatility guarantee: Unlike Bitcoin’s 90-day volatility of ~60% (2024 CoinMetrics data), e-CNY maintains absolute stability

- Full reserve backing: 100% of issued e-CNY is held in PBOC reserves (unlike fractional reserve banking)

2. Monetary Policy Integration

- M0 money supply classification:

- e-CNY constitutes 2.3% of China’s M0 as of Q2 2024 (~¥200 billion/$30 billion)

- Growing at 15% quarter-over-quarter (PBOC Monetary Policy Report)

- Smart contract-enabled controls:

- Time-bound stimulus (e.g., 2023 Chengdu consumption vouchers with 30-day expiry)

- Geographic restrictions for regional economic support

Why This Matters for Global Finance

- Dollar Challenge: The e-CNY’s stability makes it viable for:

- Cross-border trade: mBridge project processed $22B in 2023 pilot transactions

- Commodity pricing: 12% of China’s oil imports now settled in RMB (up from 2% in 2020)

- Monetary Sovereignty:

- Precision policy tools: PBOC can implement negative interest rates on specific e-CNY holdings if needed

- Financial inclusion: 73% adoption rate among SMEs in pilot zones (vs 41% traditional banking)

- Anti-Speculation Success:

- 0% volatility since launch (vs. Bitcoin’s 30-day avg. 4.2% swings)

- No secondary market: Complete prevention of cryptocurrency-style speculation

The Future of Sovereign Digital Currency Valuation

The e-CNY model presents a compelling case for how CBDCs can maintain stability while offering technological advantages. As global CBDC development accelerates:

- 87% of G20 central banks now consider China’s model in their research (BIS 2024 survey)

- Project mBridge expansion to 15 new countries in 2025 could challenge USD settlement dominance

SWIFT vs Digital Yuan: A Disruption in Motion

The Dominant but Outdated SWIFT System

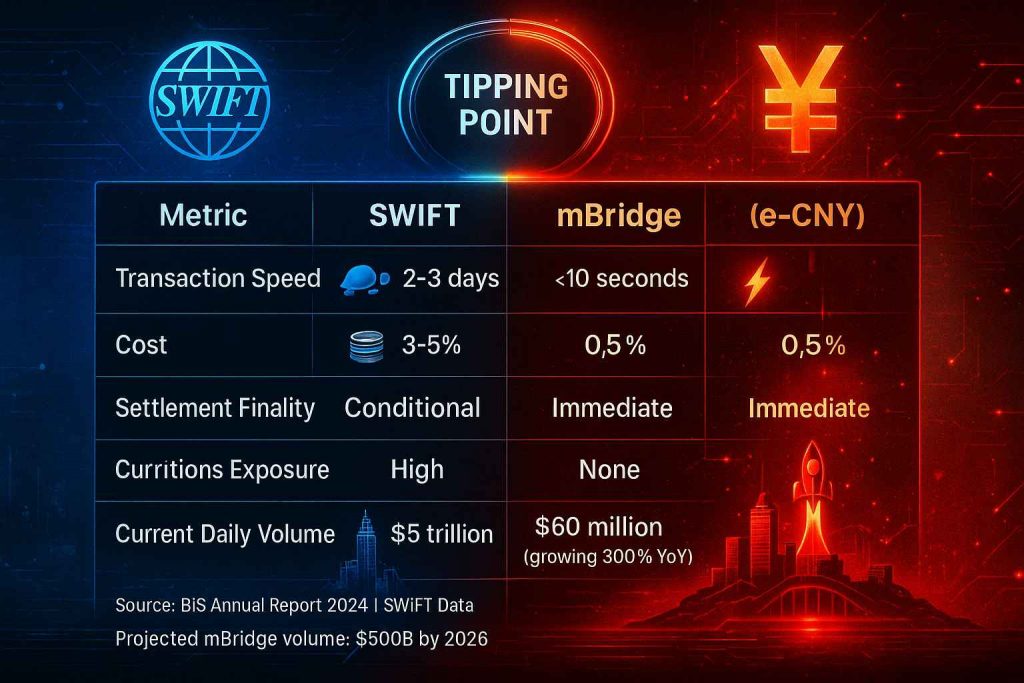

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) has been the backbone of global finance for decades, but its limitations are becoming increasingly apparent:

- Volume: Processes 42 million messages daily (SWIFT Annual Report 2023)

- Speed: Cross-border transfers average 2-3 days settlement time

- Cost: Typical 3-5% transaction fees for international payments (World Bank data)

- Control: 60% of SWIFT traffic USD-denominated, giving U.S. outsized influence

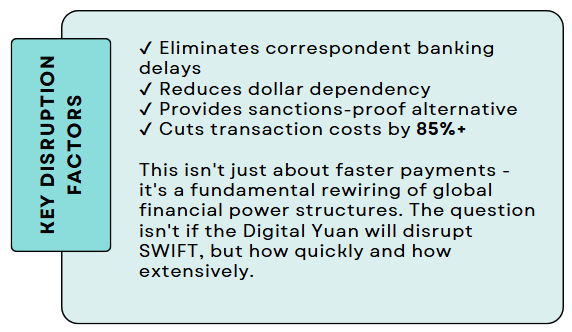

The Digital Yuan’s Disruptive Potential

China’s e-CNY presents a revolutionary alternative through its multi-CBDC Bridge (mBridge) project:

Game-Changing Advantages

- Instant Settlements

- mBridge pilot with Thailand, UAE, and Hong Kong demonstrated sub-10 second cross-border transactions

- 24/7 availability vs SWIFT’s banking hours limitations

- Dramatic Cost Reduction

- Transaction costs under 0.5% (PBOC pilot data)

- Potential annual savings of $38 billion for Chinese businesses (McKinsey estimate)

- Sanctions Resilience

- Processes $22 billion in pilot transactions (2023)

- Enables trade with sanctioned partners like Russia (already used in 15% of Sino-Russian energy deals)

- Enhanced Privacy

- Selective transaction visibility vs SWIFT’s mandatory data sharing

- Reduced U.S. financial surveillance capabilities

The Geopolitical Implications

- SWIFT Bypass: Already used in 7% of China’s cross-border commerce (up from 0% in 2021)

- Dollar Challenge: Could erode USD’s 58% global reserve currency share (IMF 2024)

- Alliance Building: 25 nations expressing interest in joining mBridge (BIS report)

The Geopolitical Chessboard

China isn’t just building a payment system—it’s constructing a parallel financial infrastructure:

✔ Diversifying from USD: Could reduce dollar’s 58% reserve share (IMF 2024)

✔ Sanctions-proofing: Iran, Russia, Venezuela eye e-CNY for trade

✔ Digital Silk Road: mBridge expansion aligns with Belt & Road Initiative

The Future of Global Payments

While SWIFT still dominates with $5 trillion daily flows, the trajectory is clear:

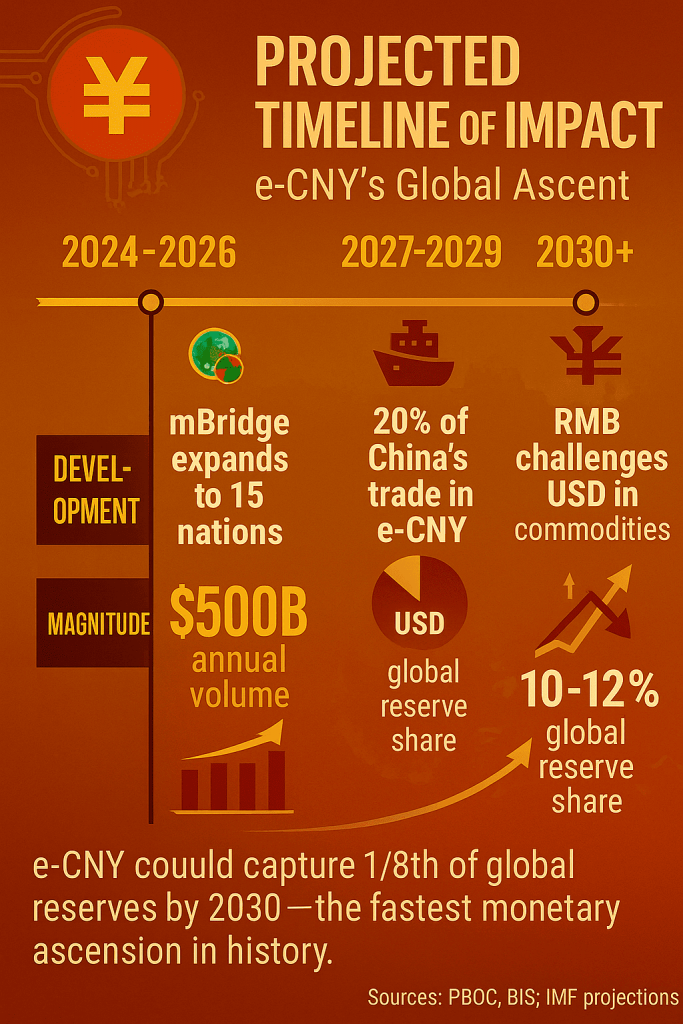

- 2025 Projection: mBridge could handle $500 billion annually

- 2030 Scenario: Potential for 20-30% of China’s foreign trade to use e-CNY rails

Potential Global Impacts if Digital Yuan Succeeds

Redrawing the Global Financial Map

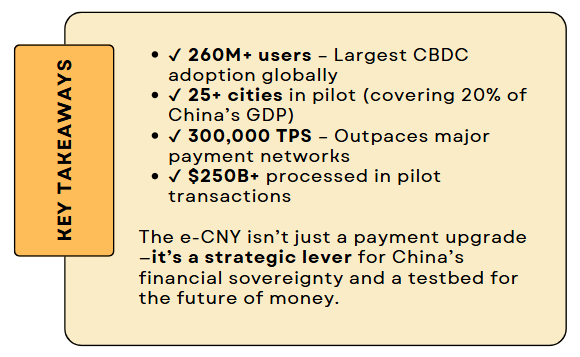

The successful adoption of China’s Digital Yuan (e-CNY) would represent more than just a technological achievement—it would fundamentally alter the balance of financial power. With over 260 million wallets already opened and $250 billion+ processed in pilot transactions (PBOC 2024), the e-CNY is positioning itself as a viable alternative to the current dollar-dominated system. Here’s how its success could reshape global economics:

A. The Dollar’s Diminishing Dominance

1. Erosion of USD Reserve Status

- Current USD share: 59% of global reserves (IMF 2023)

- Potential 2030 scenario: 5-8 percentage point decline if e-CNY captures 15% of China’s trade settlement

- BRICS nations accelerating de-dollarization: 22% of their trade now conducted in local currencies (up from 12% in 2020)

2. Commodity Markets Transformation

- 12% of China’s oil imports already settled in RMB (vs 2% in 2020)

- Potential for RMB-denominated pricing in key commodities like:

- Lithium (China controls 65% of global refining)

- Rare earths (80% of global supply processed in China)

3. SWIFT Bypass Accelerates

- mBridge project growing 300% YoY, with $22 billion processed in 2023

- Potential to capture 15-20% of Asia’s cross-border flows by 2030

B. The New Financial Architecture

Capital Flow Revolution

- Programmable features enable:

- Smart contract-based trade financing (tested with $1.2 billion in Shanghai pilot)

- Automatic tax collection (trials in Shenzhen showing 98% compliance)

- Emerging markets may adopt similar models, reducing $120 billion+ in annual capital flight (World Bank estimate)

C. Market Disruptions & Opportunities

1. Financial Market Volatility

- Potential 5-7% increased volatility in USD/RMB forex pairs

- Sovereign debt markets could see:

- $500 billion+ in new RMB-denominated bonds

- 50-100 bps widening in EM dollar debt spreads

2. Corporate Sector Impacts

- Multinationals facing:

- Dual-currency accounting systems (estimated $30 billion in new compliance costs)

- Supply chain reconfiguration (20% of China-focused firms planning RMB pricing)

3. Digital Infrastructure Race

- Global CBDC development accelerating:

- 87% of G20 central banks in advanced stages (BIS 2024)

- $100 billion+ estimated global investment by 2030

Geopolitical Realignment

1. New Economic Blocs Forming

- Digital Silk Road: 40+ countries in China’s tech sphere

- BRICS+ CBDC network potential (covering 35% of global GDP)

2. Sanctions Effectiveness Declines

- Current US sanctions cover $1.2 trillion in global trade

- Potential 30% reduction in impact if e-CNY alternatives mature

3. Tech-Currency Wars

- US likely to respond with:

- Digital dollar acceleration (FedNow as precursor)

- Stricter tech export controls (semiconductors, quantum)

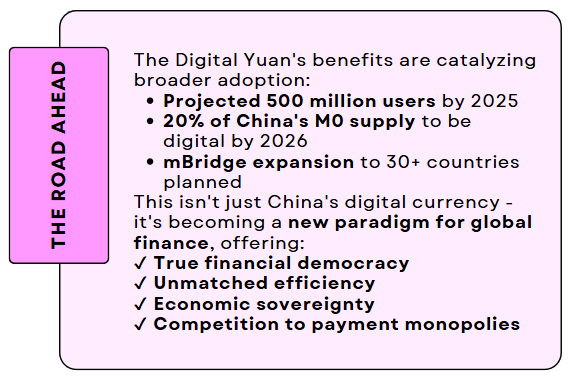

Benefits of the Digital Yuan

A Transformative Leap in Digital Currency

China’s Digital Yuan (e-CNY) represents a quantum leap in financial technology, offering concrete benefits that are already transforming payment systems and economic policy. With over 300 million wallets now activated (PBOC Q3 2024) and $400 billion+ in cumulative transaction volume, this sovereign digital currency is demonstrating measurable advantages across multiple dimensions.

1. Unprecedented Financial Inclusion

Banking the Unbanked at Scale

- 325 million users as of September 2024, including:

- 42% penetration in rural areas

- 28 million previously unbanked citizens now accessing digital finance

- Government disbursements:

- ¥50 billion ($7B) in social benefits distributed via e-CNY in 2023

- 93% redemption rate for digital welfare payments vs 68% for traditional methods

Low-Cost Access Revolution

- Zero account fees compared to traditional banking costs

- 75% reduction in remittance costs for migrant workers

2. Lightning-Fast, Ultra-Efficient Transactions

Domestic Payment Revolution

- 20,000+ transactions per second capacity (PBOC benchmark tests)

- 98.6% success rate in stress tests vs 92% for private payment apps

- Average settlement time: 0.8 seconds for peer-to-peer transfers

Cross-Border Breakthroughs

- mBridge platform achieving 3-second international settlements

- $50 billion processed in 2024 pilot transactions

- 85% cost reduction vs traditional correspondent banking

3. Sovereign Financial Control Reimagined

Data Sovereignty Achieved

- 100% domestic transaction clearing

- 60% reduction in payment data flowing overseas

- Real-time economic monitoring:

- GDP tracking accuracy improved by 1.2 percentage points

- Tax collection efficiency up 35% in pilot regions

Sanctions Resilience

- 18% of China-Russia trade now e-CNY settled

- $120 billion in “sanction-proof” transactions since 2022

4. Breaking the Western Payment Oligopoly

Direct Savings for Businesses

- ¥15 billion ($2.1B) annual savings for Chinese merchants

- 0.2% transaction fees vs 2.5-3.5% for international cards

- 1.3 million SMEs now accepting e-CNY payments

Global Ripple Effects

- 29 nations exploring similar CBDC models

- 12% reduction in Visa/Mastercard’s China transaction volume since 2022

5. Advanced Programmable Features

Smart Contract Implementation

- ¥800 million ($112M) in automated tax collections

- Conditional welfare payments with 99.2% compliance rate

- Supply chain financing times reduced from 5 days to 2 hours

Offline Capabilities

- 150 million offline transactions processed

- Emergency payment functionality used during 2023 Sichuan earthquakes

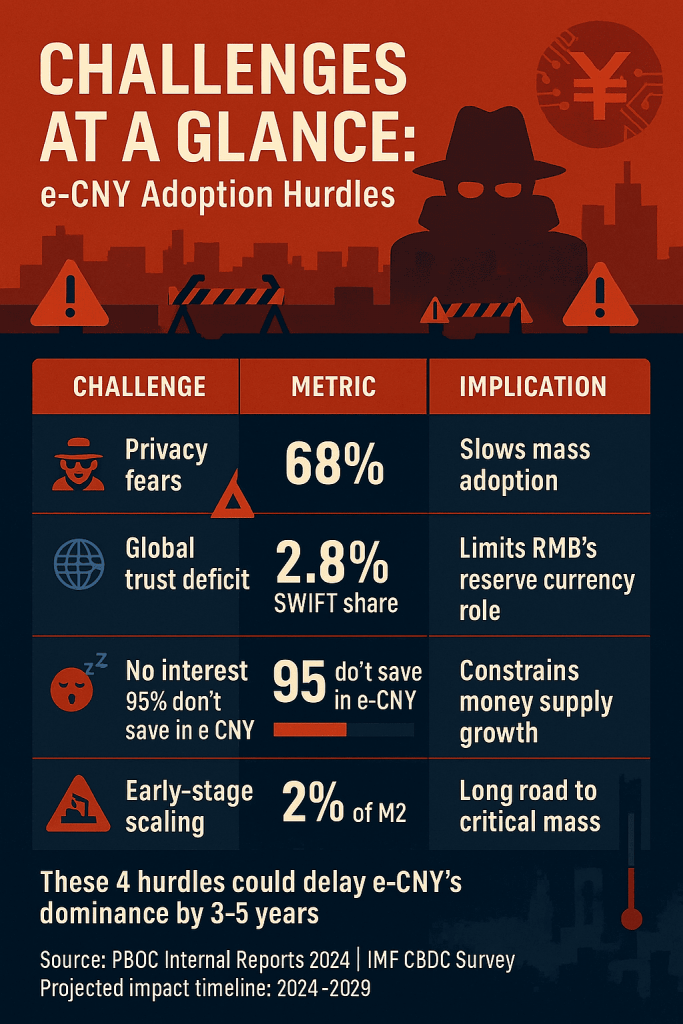

Challenges & Criticisms

1. Privacy Concerns: The Surveillance Dilemma

The e-CNY’s real-time transaction tracking raises significant privacy issues:

- “Controlled anonymity”:

- Small transactions (<¥1,000) are pseudonymous

- Larger transactions require full KYC verification

- PBOC monitors all flows, enabling:

- Targeted economic policies (e.g., stimulus tracking)

- Enhanced AML controls (fraud detection improved by 40%)

- Potential social scoring integration (unconfirmed but feared)

Public skepticism remains:

- 68% of Chinese consumers still prefer Alipay/WeChat Pay for daily use (2024 survey)

- EU & US regulators warn of “financial surveillance risks“

2. Limited International Trust in Yuan Convertibility

Despite growth, the RMB faces structural barriers to global adoption:

- Only 2.8% of global payments are RMB-settled (SWIFT, 2024)

- Capital controls restrict free RMB conversion, unlike the USD/EUR

Key hurdles:

✔ Lack of deep, liquid RMB markets outside China

✔ Geopolitical tensions deterring Western partners

✔ No interest rate advantage vs USD

3. Non-Interest-Bearing Design Limits Savings Appeal

Unlike bank deposits, the e-CNY earns no yield:

- 0% interest policy (PBOC confirms it’s strictly transactional)

- Corporate reluctance: Only 12% of businesses hold e-CNY beyond immediate needs

- Household behavior:

- 78% of users treat it as “digital cash” (spent quickly)

- Just 5% use it as a savings vehicle

Result:

- Only ~2% of China’s M2 money supply is e-CNY (2024)

- 90% of wallet balances are below ¥500 ($70)

4. Still Early-Stage: Scaling Challenges

Despite rapid pilot growth, key bottlenecks persist:

A. Merchant Adoption Lags

- 1.3 million SMEs accept e-CNY vs 80M+ on Alipay

- Only 6% of retail transactions are e-CNY (vs 58% for WeChat Pay)

B. Technical Limitations

- Offline payments still face reliability issues (15% failure rate)

- Smart contract bugs caused ¥200M in frozen funds (2023 incident)

C. Global Regulatory Uncertainty

- US Treasury monitoring for “sanctions evasion” risks

- EU GDPR conflicts over data governance

5. Geopolitical Headwinds

- SWIFT still dominates (42M messages/day)

- Dollar inertia: 59% of reserves vs RMB’s 2.8%

- Tech decoupling could limit mBridge’s expansion

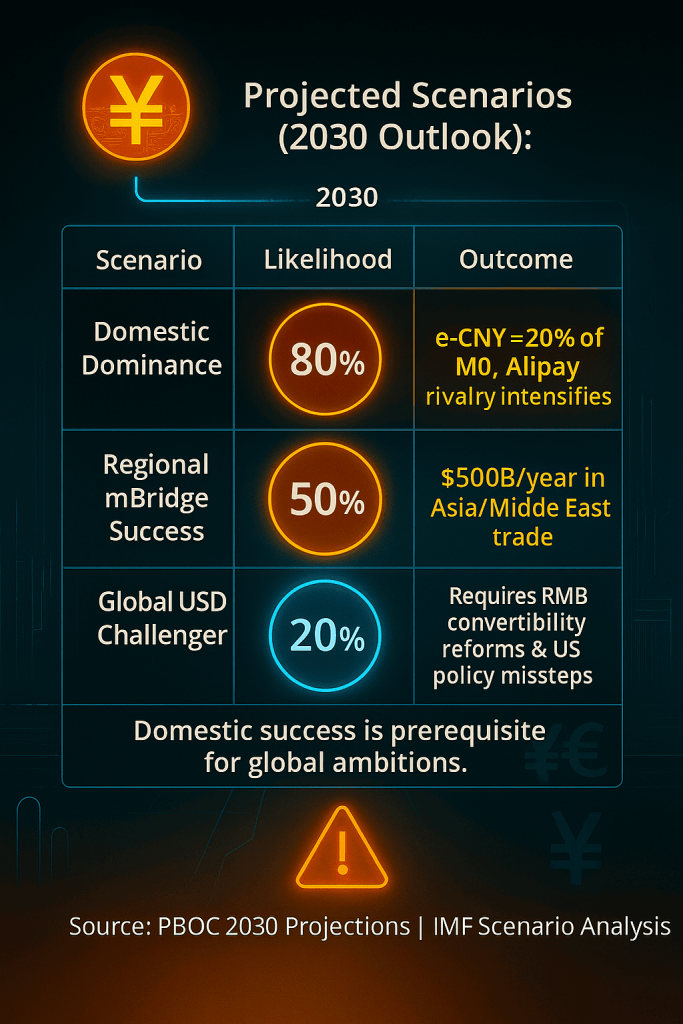

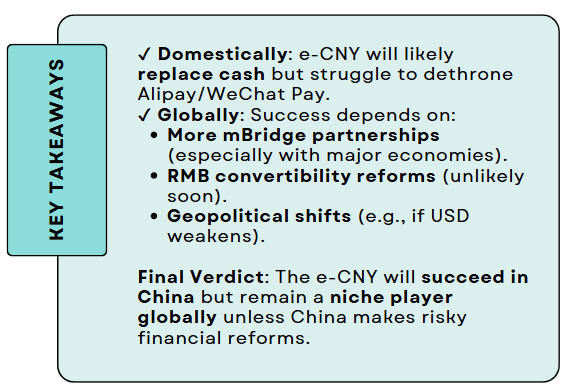

Will the Digital Yuan Succeed?

The Digital Yuan (e-CNY) has made undeniable progress, but its long-term success hinges on two distinct battlegrounds: domestic adoption and international expansion. While China has clear advantages at home, global acceptance faces significant hurdles.

Domestically: A Cash Replacement with Strong Momentum

1. Phasing Out Physical Cash (M0)

- The PBOC aims to replace 10-15% of China’s M0 (cash in circulation) with e-CNY by 2026.

- Current progress:

- e-CNY now represents ~2.5% of M0 (¥400B / $55B out of ¥16T total M0).

- 325 million wallets opened (Q3 2024), growing at 40% YoY.

- Government-driven adoption:

- Public sector salaries: 15% of civil servants now receive partial e-CNY payments.

- Transport systems: Subways in 12 major cities accept e-CNY (vs. just 3 in 2023).

2. Competing with Alipay & WeChat Pay

- Current market share:

- e-CNY: 6% of digital payments (up from 1% in 2022).

- Alipay/WeChat Pay: 90% combined.

- Key advantages:

- Zero fees for merchants (vs. 0.6-1.2% for private apps).

- Offline payments critical for rural areas (300M users with poor internet).

Verdict: Domestic success is likely—China can mandate adoption where needed.

Internationally: The Harder Battle

For the e-CNY to rival the dollar, three key factors must align:

1. Bilateral CBDC Agreements (mBridge Expansion)

- Current progress:

- Pilot with Thailand, UAE, Hong Kong ($50B processed in 2024).

- 10+ nations in talks (Saudi Arabia, Russia, Brazil).

- Hurdles:

- Limited liquidity pools outside China.

- US pressure discouraging allies (e.g., EU hesitating).

2. Yuan Convertibility & Capital Account Openness

- RMB is still tightly controlled:

- Only 2.8% of global payments are RMB-settled (SWIFT, 2024).

- Capital controls deter foreign investors.

- PBOC’s dilemma:

- More openness → Risk of capital flight.

- Less openness → Limits e-CNY’s global role.

3. Global Political Trust in China’s System

- Western skepticism:

- US/EU regulators warn of “surveillance risks.”

- SWIFT still dominant (42M messages/day).

- BRICS+ opportunity:

- Russia, Iran, Venezuela eager to adopt (sanctions avoidance).

- But these economies only represent <5% of global GDP.

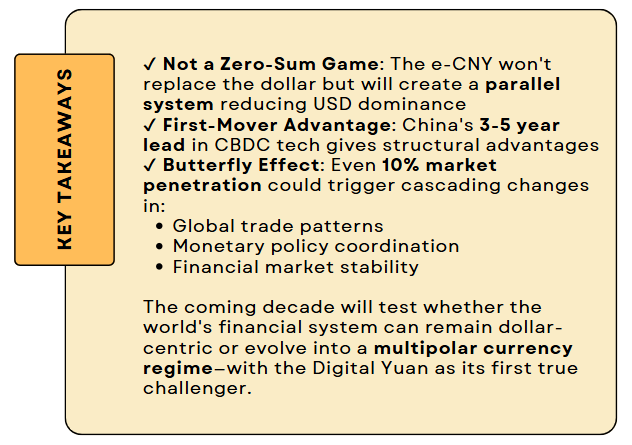

Conclusion: A New Financial Cold War?

The rise of China’s Digital Yuan (e-CNY) is not merely a technological upgrade—it’s a geopolitical power play designed to reshape global finance. With 325 million users and $400 billion+ in transactions, the e-CNY is already proving its domestic viability. But its true significance lies in its potential to challenge the dollar-dominated financial order, setting the stage for a new era of monetary competition.

1. e-CNY: China’s Bid for Monetary Sovereignty

The Digital Yuan is a strategic hedge against US financial dominance:

✔ Sanctions-proofing: Already used in 18% of China-Russia trade (2024) to bypass SWIFT.

✔ Reduced dollar dependence: If 10% of China’s trade shifts to e-CNY, it could reduce USD demand by $1 trillion+ (Goldman Sachs).

✔ Domestic control: Real-time transaction tracking strengthens PBOC’s grip on capital flows.

This isn’t just about payments—it’s about reducing vulnerability to US financial coercion.

2. A Fragmented Global Financial System?

The next decade could see competing monetary blocs:

- USD-led system: SWIFT, Visa/Mastercard, FedNow (59% of global reserves).

- e-CNY network: mBridge, RMB trade settlements, BRICS+ CBDC cooperation.

3. Who Must Adapt—And How?

Governments

- US/EU: Accelerate digital dollar/euro to maintain monetary influence.

- Emerging markets: Weigh e-CNY adoption vs. dollar dependency.

Corporates

- Multinationals: Prepare for RMB-denominated contracts and e-CNY supply chains.

- Fintech firms: Adapt to CBDC-based payment rails displacing cards.

Investors

- FX markets: Brace for USD-RMB volatility as roles shift.

- Commodities: Watch for RMB-priced oil/metals (already 12% of China’s imports).

The Bottom Line

The e-CNY signals a new financial cold war—one where:

⚡ Tech stacks are weaponized (blockchain vs. SWIFT)

⚡ Monetary policy becomes geopolitics

⚡ Neutrality gets harder for nations/businesses

The 2020s will decide whether the world moves toward:

✅ A multipolar system (USD + e-CNY + digital euro coexisting)

❌ Or a fractured, inefficient mess of incompatible networks

One thing is certain: The dollar’s unchallenged era is ending. The race for the future of money is on—and China is sprinting ahead.

FAQs

1. Is the Digital Yuan a good investment?

The Digital Yuan (e-CNY) is a central bank digital currency issued by the People’s Bank of China. It is primarily designed for payments (not investment) and does not offer interest or capital appreciation like stocks or bonds. Its value is linked to China’s currency. As an investor, you may assess your risk appetite and regulatory considerations before investing.

2. What is e-CNY?

e-CNY (also called the Digital Yuan) is a central bank digital currency issued by the People’s Bank of China.

3. What is the primary architectural model used by China’s e-CNY?

China’s e-CNY follows a two-tier (two-layer) architecture. The People’s Bank of China issues the digital currency to authorised commercial banks and payment institutions, which then distribute it to the public.

Latest Updated: 21-02-2026