|

Getting your Trinity Audio player ready...

|

Introduction: A Crucial Pillar in the Global Financial Ecosystem

The Indian debt market, valued at $2.59 trillion in 2024, is a cornerstone of the country’s financial system and a key player in Asia. Despite being one of the largest in the region, the market is dominated by highly-rated bonds (AAA, AA+, and AA), with corporate bonds accounting for 16% of India’s GDP, a figure much lower compared to countries like Malaysia, South Korea, and China. This underlines both the untapped potential and the pressing need for reforms.

While corporate bond issuances reached a record ₹10.67 trillion ($124.81 billion) by December 2024, marking a 9% increase from 2023, secondary market trading volumes remained stagnant, averaging ₹5722 crores daily, a trend unchanged since 2018. The “buy-and-hold” approach by institutional investors, along with the dominance of private placements, restricts liquidity and broader market growth. Addressing these challenges is critical for India to unlock the full potential of its debt market and capitalize on global economic trends.

Global Debt Trends and Their Impact on India

As we move into 2025, the global debt landscape has reached unprecedented levels, exceeding $300 trillion, driven by rising interest rates and tightening monetary policies in developed economies like the US and EU. The US Federal Reserve and European Central Bank (ECB) have implemented aggressive rate hikes to combat persistent inflation, creating ripple effects across emerging markets, including India.

(Source: Trading Economics)

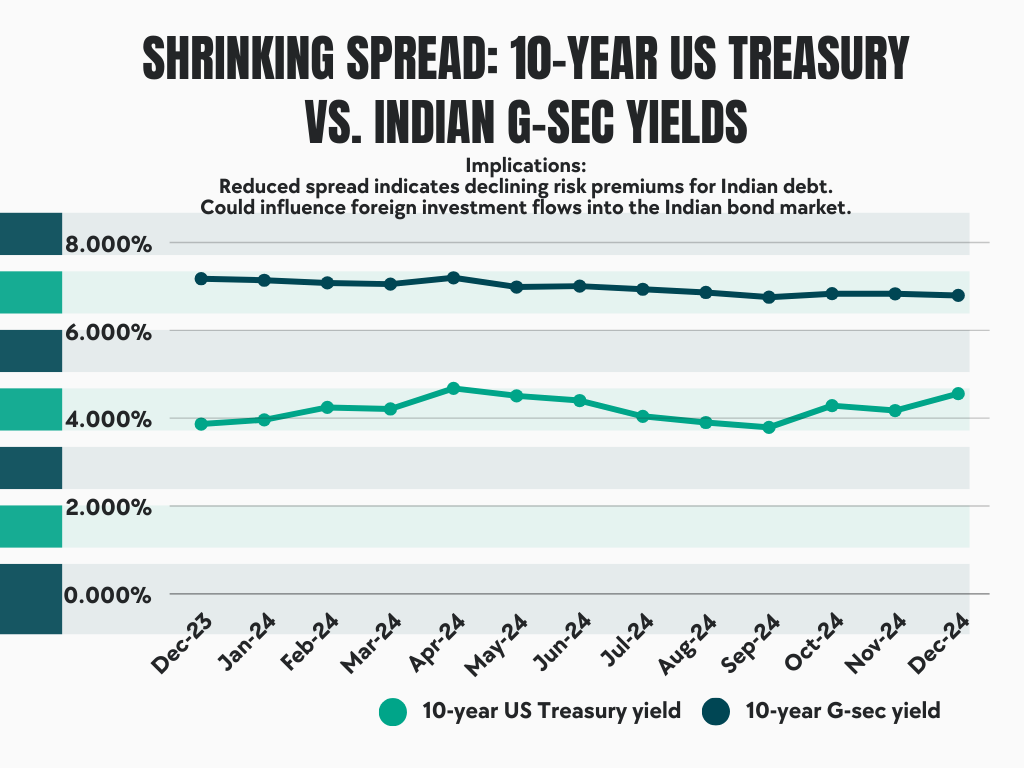

India’s bond market, intricately tied to global monetary trends, has come under significant pressure. The 10-year US Treasury yield rose to 4.52%, while India’s 10-year G-sec yield stood at 6.79%, narrowing the India-US bond yield spread to a 2-decade low of 227 basis points as of December 2024. This shrinking spread has made Indian debt less attractive to foreign portfolio investors (FPIs), who traditionally seek higher returns to balance the risks of emerging markets.

The implications for India are far-reaching. A reduced yield differential has deterred foreign inflows, critical for sustaining market liquidity and financing the fiscal deficit, which stood at 6.4% of GDP in FY2024. Additionally, rising borrowing costs, influenced by global tightening policies, have strained both government and corporate balance sheets, highlighting the challenges of managng external dependencies in a globally interconnected economy.

Understanding these dynamics is essential for policymakers and investors as they navigate an evolving financial environment shaped by the interplay of global debt trends, investor sentiment, and domestic fiscal pressures. The Indian debt market, poised at the crossroads of these challenges, offers a window into the complexities and opportunities of an increasingly globalized financial ecosystem.

Domestic Debt Market Dynamics

India’s domestic debt market in 2024 has emerged as a dynamic and robust financial ecosystem, driven by the interplay of government securities (G-secs) and corporate bonds. G-secs, which constitute over 60% of the total debt market, have maintained their dominance, serving as the benchmark for other fixed-income instruments. Corporate bonds, with an outstanding value of approximately ₹40 trillion, have also seen increased issuance, reflecting rising capital requirements across sectors. The 10-year G-sec yield, averaging 6.79%, highlights investor confidence in India’s financial stability and the Reserve Bank of India’s (RBI) balanced monetary policy stance.

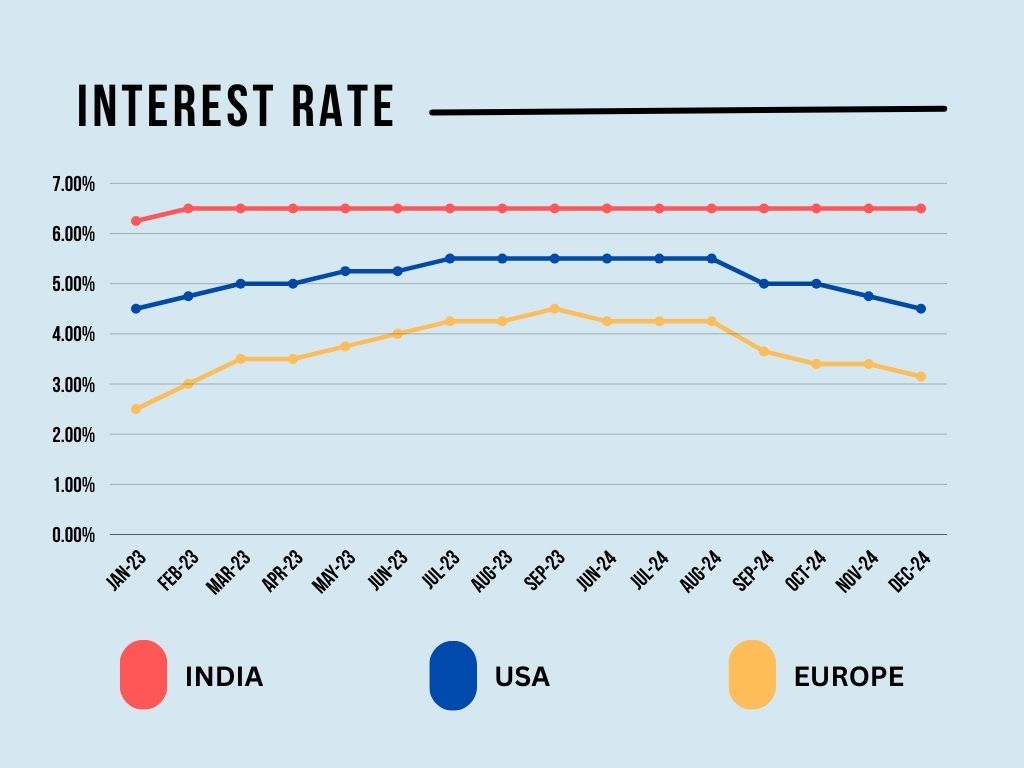

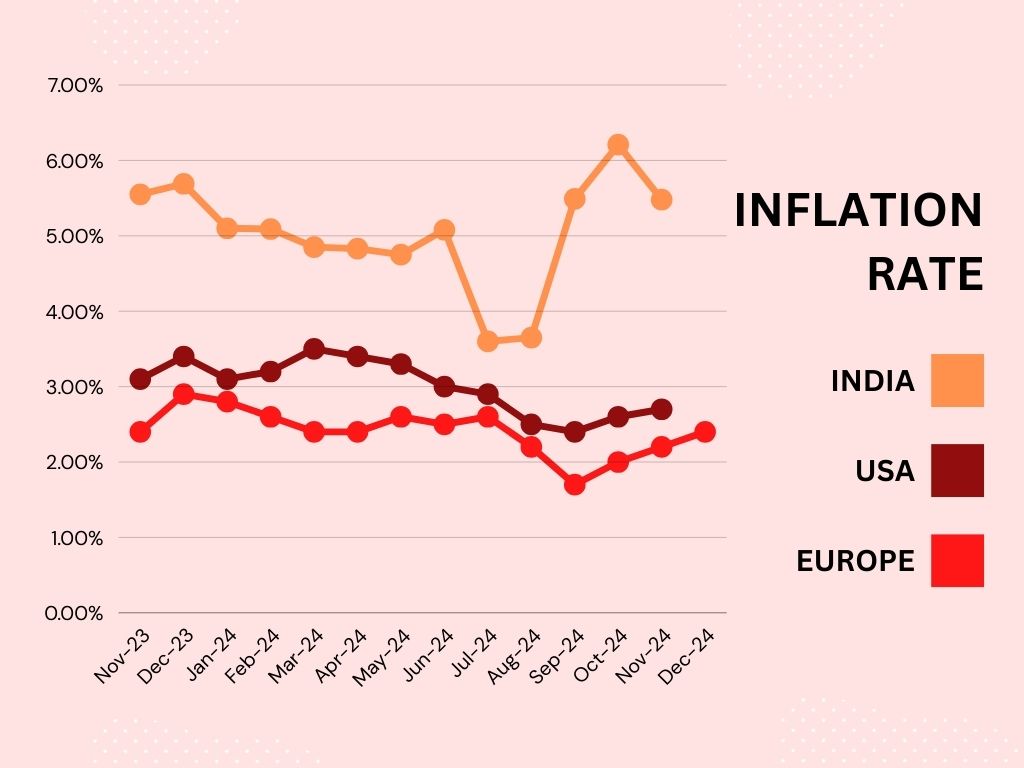

The RBI has played a pivotal role in managing liquidity and stabilizing markets through targeted interventions, including repo rate adjustments, which stood at 6.5% in December 2024. By aligning its policies with the inflation target of 4% +/- 2%, the RBI has ensured price stability while fostering economic growth. These measures underscore the central bank’s commitment to maintaining a stable financial environment amidst global and domestic challenges.

A transformative development in 2024 has been the rise of domestic retail participation in the G-sec market, facilitated by the RBI Retail Direct platform. This initiative, which has registered over 1.5 lakh individual investors by December 2024, has democratized access to government bonds, enhancing market liquidity and promoting financial inclusivity. Retail investors now have greater opportunities for stable returns, contributing to the market’s depth and resilience.

India’s debt market, underpinned by a strong regulatory framework and increasing retail engagement, continues to evolve as a cornerstone of the country’s financial system. Understanding its dynamics, from the RBI’s liquidity management to shifting inflation targets and growing retail participation, is essential for stakeholders navigating this critical segment of the economy. With its dual focus on inclusivity and stability, the Indian debt market is poised to strengthen its position in the global financial ecosystem.

Dependency on Developed Markets

India’s debt market outlook is deeply intertwined with the economic trends of developed economies such as the US, EU, and China. Changes in these regions, particularly in interest rates and inflation policies, directly influence capital flows and investor sentiment toward emerging markets like India. For instance, as of December 2024, the India-US bond yield spread narrowed to a 2-decade low of 227 basis points, making Indian debt securities relatively less attractive to foreign portfolio investors (FPIs) seeking higher risk-adjusted returns.

(Source: Trading Economics)

FPIs, who contributed approximately ₹3.5 lakh crore to India’s debt market in 2024, are especially sensitive to external factors such as geopolitical tensions and the threat of a global recession. The ongoing economic slowdown in China and trade uncertainties in the EU have further increased the volatility of foreign inflows into India. Additionally, tightening monetary policies by the US Federal Reserve and the European Central Bank (ECB) have raised global borrowing costs, influencing the comparative appeal of Indian debt.

India’s debt market is also intricately linked to the global equity market. Strong equity performances in developed markets often divert capital away from Indian debt instruments. Conversely, global equity market corrections can lead investors to reallocate funds to safer fixed-income options, benefiting Indian debt securities. However, this interdependence exposes the Indian debt market to external shocks, impacting liquidity and pricing.

(Source: Trading Economics)

While India’s stable macroeconomic environment and growing economy present attractive opportunities for foreign investment, its reliance on developed markets underscores the need for calibrated domestic policies. These policies must focus on mitigating external risks and ensuring steady debt inflows to sustain market liquidity and financial stability amidst global uncertainties.

Challenges in the Indian Debt Market

Low Liquidity in the Secondary Market

- Daily trading volumes averaged ₹5722 crores in FY2024, stagnant since 2018 despite a 72% growth in outstanding corporate bonds.

- The “buy-and-hold” strategy of institutional investors and dominance of private placements limit market activity.

Barriers to Public Issuance

- Public issuance of corporate bonds has declined from 12% of total issuances in 2014 to 2% in 2024, with ₹838,000 crores raised through private placements compared to just ₹19,000 crores via public routes in FY2024.

- SEBI has simplified regulations, including fast-track issuance, to encourage corporates to opt for public placements.

Debt Recovery Challenges

- Inefficiencies in debt recovery frameworks, including the Insolvency and Bankruptcy Code (IBC) and Debt Recovery Tribunals (DRTs), hinder creditor confidence.

- The introduction of out-of-court restructuring frameworks, modeled after systems in South Korea, could expedite recoveries and reduce judicial burdens.

Dependence on Highly-Rated Bonds

- Regulatory restrictions prevent insurers and pension funds from investing in bonds rated below AA, limiting market diversity.

- Developing credit derivatives and a corporate repo market can help manage credit risks and encourage lower-rated bond issuances.

Microfinance Sector Stress

- Stress in the microfinance sector in India could lead to higher yields in the Indian debt market as heightened credit risks may reduce investor confidence, prompting demand for a risk premium. This can also tighten liquidity and impact borrowing costs for microfinance institutions and related sectors.

Higher Risk Weights on NBFC Loans

- The RBI’s decision to increase the risk weight on loans to NBFCs to 125% will likely raise borrowing costs for NBFCs, reducing their access to credit and impacting liquidity. This could tighten the Indian debt market, particularly in sectors heavily reliant on NBFC funding.

Opportunities and Outlook for India’s Bond Market in 2025

India’s bond market is poised for transformative growth in 2025, driven by opportunities in infrastructure and green bonds, regulatory reforms, and innovative strategies to enhance market participation and liquidity. Here’s a concise outlook:

Infrastructure and Green Bonds: Catalysts for Growth

- The government’s ambitious $1.4 trillion National Infrastructure Pipeline (NIP) has created fertile ground for infrastructure bond issuances, supporting long-term economic growth.

- In 2024, India raised over $10 billion in green bonds, establishing itself as a leading emerging market for sustainable finance. This trend highlights the growing importance of environmentally and socially responsible investments.

Reforming FPI Norms to Boost Liquidity

- Revising restrictive Foreign Portfolio Investment (FPI) norms, such as the 3-year lock-in period and allocation limits under the Voluntary Retention Route (VRR), can attract more global investors.

- Enhanced foreign investment will inject liquidity and depth into the bond market, supporting its expansion and resilience.

Unified Market Operations for Seamless Functioning

- Integrating the trading, clearance, and settlement frameworks of government securities (G-secs) and corporate bonds will improve efficiency and pricing transparency.

- Unified operations will foster a seamless market environment, reduce transaction costs, and enhance investor confidence.

Strengthening Debt Recovery Mechanisms

- Introducing standardized out-of-court restructuring frameworks, inspired by models in South Korea and the Philippines, can expedite debt recovery and improve bondholder confidence.

- The proposed creditor-led insolvency resolution process (CLRP) can reduce judicial delays and attract greater participation from institutional and retail investors.

Encouraging Public Issuance of Bonds

- Despite its potential, public issuance of corporate bonds accounted for only 2% of total issuances in 2024, with private placements dominating at 98%.

- Simplified compliance processes, such as fast-track public issuance of Non-Convertible Debentures (NCDs), can encourage more corporates to choose public routes,improving transparency and price discovery while creating more upcoming bonds in India for investors ensuring better transparency and price discovery.

Developing Complementary Markets for Lower-Rated Bonds

- India’s bond market remains skewed towards highly-rated bonds (AAA, AA+, and AA). Developing credit derivatives and a robust corporate repo market will encourage the issuance of lower-rated bonds by managing credit and interest rate risks.

- Tools like interest rate derivatives and credit default swaps can attract foreign investors by offering effective hedging mechanisms.

Conclusion: Paving the Way for Growth

The Indian debt market in 2025 is at a critical juncture, balancing opportunities for growth with challenges such as low liquidity, high fiscal deficits, and external dependencies. With strategic reforms, including enhanced debt recovery mechanisms, improved public issuance frameworks, and the development of complementary markets, India can foster a more inclusive and robust bond market.

As India aspires to become the world’s third-largest economy by 2027, a well-functioning, liquid debt market will be pivotal in attracting investments, supporting infrastructure growth, and achieving sustainable economic development.