|

Getting your Trinity Audio player ready...

|

When you invest in a bond, you look at the yield, check the credit rating, and then decide whether to go ahead. That process makes sense. But there’s one document most investors skip: the term sheet.

A bond term sheet is a summary of all the key terms of a bond. It tells you exactly how the bond works, when you get paid, what happens if the issuer wants to repay early and what your rights are if something goes wrong. Some of these terms can change your actual returns in ways you may not expect.

Here are five things to check in a term sheet before you invest.

Red Flag 1: A Call Option in the Redemption Section

When you buy a bond, you expect the issuer to repay your money on the maturity date. But some bonds include a call option, which gives the issuer the right to repay your principal early, before the bond matures.

Look for phrases like “call date,” “callable at par,” or “issuer’s right to redeem.” If these appear in the term sheet, the company can return your money whenever it suits them, usually when interest rates in the market have fallen.

Start investing with just 10K & grow your wealth with fixed-return bond opportunities.

Explore NowHow reinvestment risk affects your returns

Say you invest in a bond at 9.5% for seven years.

Two years later, interest rates fall to 7%.

The issuer calls the bond and returns your principal.

Now, you have to reinvest that money at 7% instead of 9.5%.

So instead of earning 9.5% for seven years, you earned it for only two years, and the rest at a lower rate.

This is called reinvestment risk.

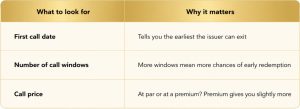

Call option details to verify in the term sheet

Call option

Red Flag 2: YTM Is Shown, But YTC Is Not

Most platforms show you the Yield to Maturity (YTM) of a bond. This is the return you earn if the bond runs till its final maturity date. It’s the most commonly advertised number because it tends to be the higher figure.

But if the bond has a call option, there is another number you should ask for.

Yield to Maturity vs Yield to Call: Key differences

Yield to Maturity

If the issuer is likely to call the bond early, YTC is the more realistic number to plan around. The term sheet won’t always highlight this. You may need to ask your broker for it directly, or calculate it using the call date and call price.

Red Flag 3: “Secured” Without the Details

Term sheets describe bonds as either secured or unsecured. A secured bond is backed by a specific asset like property, receivables, or equipment. An unsecured bond, also called a debenture, relies only on the issuer’s general ability to repay.

If the term sheet says “secured,” don’t stop reading there. You need to check what kind of charge the bond carries.

Bond charge types and their impact on recovery

| Type of Charge | What it means for you |

| First charge | Your claim on the asset comes before other creditors |

| Second charge | At least one other lender gets paid before you |

| Pari passu | You share recovery equally with other bondholders in the same class |

Why does this matter? If the issuer defaults, the type of charge determines how much of your money you can recover. A first-charge bondholder and an unsecured bondholder in the same company can end up with very different outcomes. The credit rating alone won’t tell you this. The security section of the term sheet will.

Red Flag 4: The Credit Rating Does Not Tell You About the Sector

Credit ratings from agencies like CRISIL, ICRA, CARE, and India Ratings show the likelihood of the issuer repaying its debt. They are based on the company’s financials at the time of the review.

What ratings don’t automatically tell you is how the issuer’s industry is doing.

Credit rating scope: what it measures and what it misses

| What ratings tell you | What ratings don’t tell you |

| Issuer’s financial strength at the time of review | Whether the issuer’s sector is under stress |

| Historical repayment track record | Whether industry conditions are worsening |

| Debt levels and cash flow quality | How long before a downgrade reflects ground reality |

A company rated AA in a stable, predictable business is a different kind of investment from a company rated AA in an industry going through stress. Ratings take time to catch up with changing conditions. By the time a downgrade officially comes out, bond prices in the secondary market have often already fallen.

So when you read a term sheet, also look at what business the issuer is in. Ask yourself: does this company earn money in a stable, predictable way, or does its income depend on market conditions or raising fresh capital?

Red Flag 5: Listed on an Exchange Does Not Always Mean You Can Sell It

Many corporate bond term sheets mention that the bond is listed on the BSE or NSE. Being listed means the bond can be bought and sold on the exchange. It does not mean buyers are always available when you want to sell.

Secondary market liquidity for corporate bonds in India

- The secondary market for corporate bonds in India is relatively thin

- Many institutional investors buy bonds at issuance and hold them to maturity

- After listing, trading activity on a lot of these bonds is very low

- Some bonds have a specific lock-in period of up to 12 months, during which you cannot sell at all

If you need to exit before maturity, you may find very few buyers, and those available may offer a lower price than you expected. Check the “Transferability” or “Listing and Trading” section of the term sheet for lock-in conditions.

For bonds rated below AA, or from sectors under stress, plan as if the money will stay locked in for the full tenure.

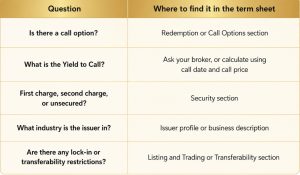

5 Things to Check in a Bond Term Sheet Before You Invest

Before putting money into any bond, use the term sheet to answer these questions:

Things to check before invest in Bond Term Sheet

The term sheet is not a formality. It is the actual contract between you and the issuer. Taking 15 minutes to read it before investing is one of the simplest ways to make a more informed decision.

FAQs on Bond Term Sheets

Q1. What is a bond term sheet?

A: A bond term sheet is a document that summarises the key terms of a bond, including the interest rate, maturity date, call options, security details, and payment structure. It gives you the important details of what you are investing in before you commit your money.

Q2. What is the difference between YTM and YTC?

A: The primary difference between YTM and YTC is what each measures. Yield to Maturity (YTM) is the return you earn if you hold the bond till its final maturity date. Yield to Call (YTC) is the return you earn if the issuer calls the bond early. On callable bonds, YTC is usually lower than YTM and is the more realistic return to plan around.

Q3. How do I know if a bond is a first charge or a second charge?

A: Look for the “Security” section in the term sheet. It will tell you the type of charge and what asset backs the bond. If it says “second charge” or “pari passu with existing lenders,” at least one other lender is ahead of you in the repayment queue.

Q4. Can a bond be called even when interest rates have not fallen?

A: Yes. Issuers can call a bond for reasons beyond interest rate changes, including refinancing decisions or changes in their capital structure. The term sheet will specify when and under what conditions the issuer can exercise the call option.

Q5. If a bond is listed on BSE or NSE, can I sell it at any time?

A: Listing means the bond is eligible for trading on that exchange. But it does not guarantee buyers will be available at a fair price. Many listed corporate bonds have low trading volumes. Before investing, check whether the bond trades regularly if you think you may need to exit before maturity.

Disclaimer: Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities, municipal debt securities/securitised debt instruments are subject to credit risks, market risks and default risks including delay and/or default in payment. Read all the offer related documents carefully.