|

Getting your Trinity Audio player ready...

|

Summary: Muthoot Fincorp Limited launches a secured NCD public issue aggregating up to ₹600 crore (base ₹200 Cr + oversubscription ₹400 Cr). These NCDs are rated AA/Stable by Crisil Ratings and AA/Stable by Brickwork Ratings. The NCD issuance is structured across twelve distinct series. The coupon rates provided vary between 8.51% and 9.25% per annum, with available investment periods of 24, 36, 60, and 72 months.

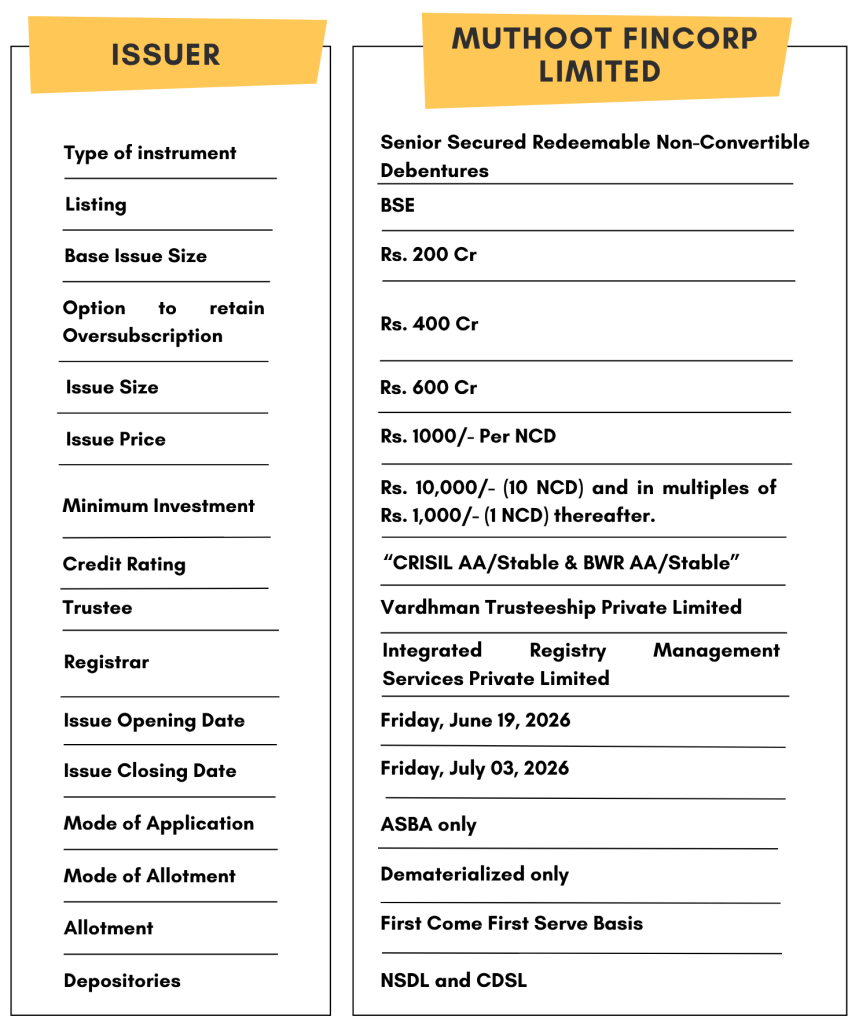

Muthoot Fincorp Limited NCD IPO: Issue Overview

Muthoot Fincorp Limited is issuing Secured, Redeemable Non-Convertible Debentures (NCDs). This issue is a strategic opportunity for investors looking for fixed-income assets with a high degree of safety.

- Credit Rating: AA/Stable (CRISIL) and AA/Stable (BWR)

- Yield Range: 8.84% to 9.25% p.a.

- Tenures: 24, 36, 60, and 72 months.

- Nature: Secured and Redeemable.

- High Yield | CRISIL AA/Stable & BWR AA/Stable Rated | Minimum Investment: 10k Only

Invest in bonds & earn 9-14%* p.a fixed returns

Start investing with just 10K & grow your wealth with fixed-return bond opportunities.

Explore NowMuthoot Fincorp NCD Interest Rates and Effective Yields

The NCDs are being issued in twelve different series to cater to different investor needs, ranging from short-term liquidity to long-term wealth compounding

| Series | Frequency of Interest Payment | Nature | Tenor | Coupon (% per Annum) | Effective Yield (% per Annum) |

|---|---|---|---|---|---|

| 1 | Monthly | Secured | 24 Months | 8.51% | 8.84% |

| 2 | Monthly | Secured | 36 Months | 8.65% | 8.99% |

| 3 | Monthly | Secured | 60 Months | 8.79% | 9.15% |

| 4 | Monthly | Secured | 72 Months | 8.88% | 9.24% |

| 5 | Annual | Secured | 24 Months | 8.85% | 8.84% |

| 6 | Annual | Secured | 36 Months | 9.00% | 8.99% |

| 7 | Annual | Secured | 60 Months | 9.15% | 9.14% |

| 8 | Annual | Secured | 72 Months | 9.25% | 9.24% |

| 9 | Cumulative | Secured | 24 Months | NA | 8.85% |

| 10 | Cumulative | Secured | 36 Months | NA | 9.00% |

| 11 | Cumulative | Secured | 60 Months | NA | 9.15% |

| 12 | Cumulative | Secured | 72 Months | NA | 9.25% |

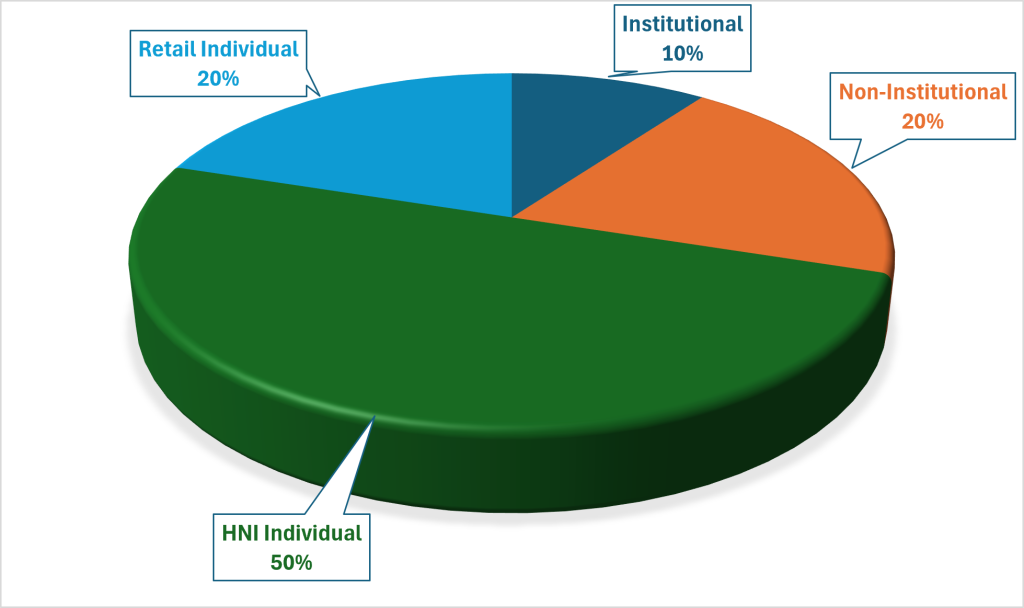

Understanding the Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories.

Recent NCD IPOs Update:

- Muthoot Fincorp Limited NCD IPO

- Edelweiss Financial Services Limited NCD IPO

- Muthoot Fincorp Limited NCD IPO

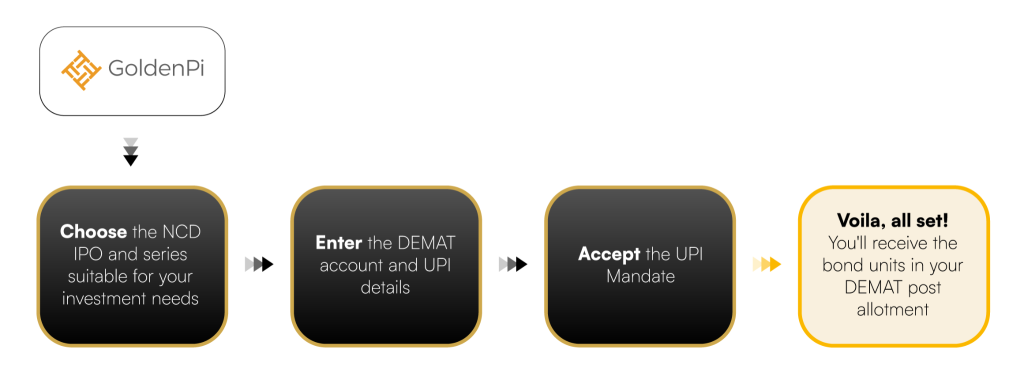

How to Invest in Muthoot Fincorp NCD IPO via GoldenPi

Investing in Bond IPOs is now seamless. Follow these easy steps:

- Log in to GoldenPi.

- Look for the Search option and type Muthoot Fincorp

- Select Muthoot Fincorp NCD IPO

- Choose your series and apply via UPI.

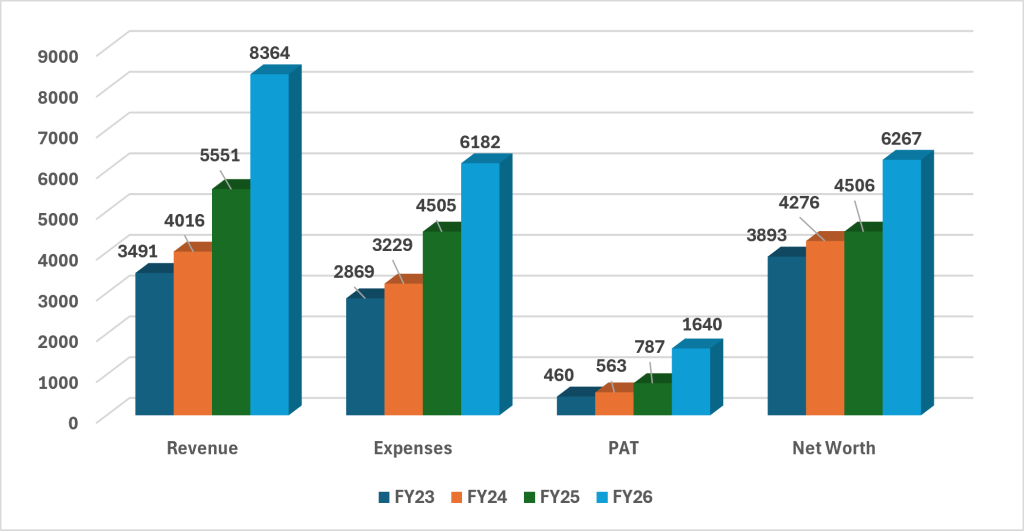

Financial Overview of Muthoot Fincorp Limited

A deep dive into the company’s balance sheet reveals a consistent growth trajectory in revenue and net worth.

Snapshot stating the Revenue, Expenses, PAT and Net-worth (In crores):

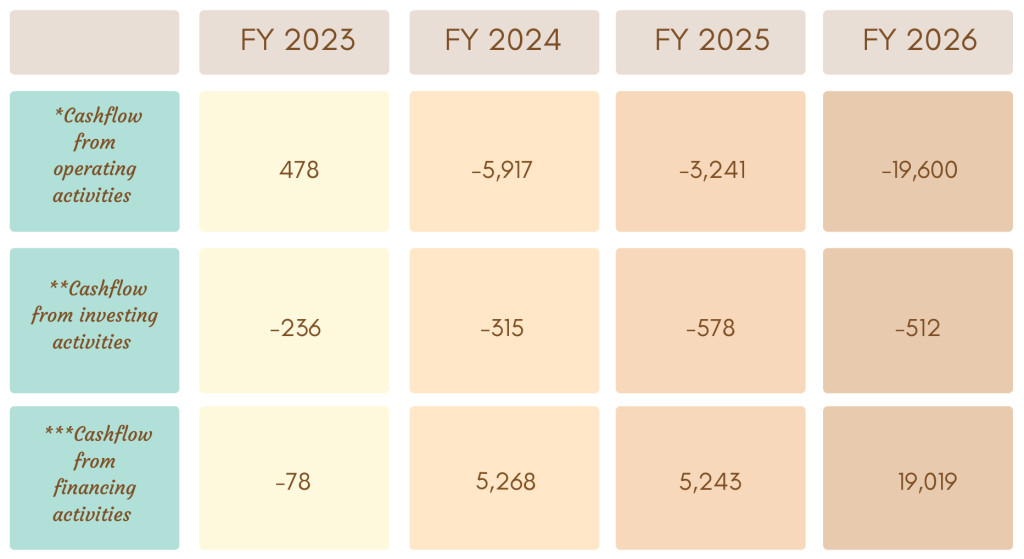

Cash Flow Analysis (In crore):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

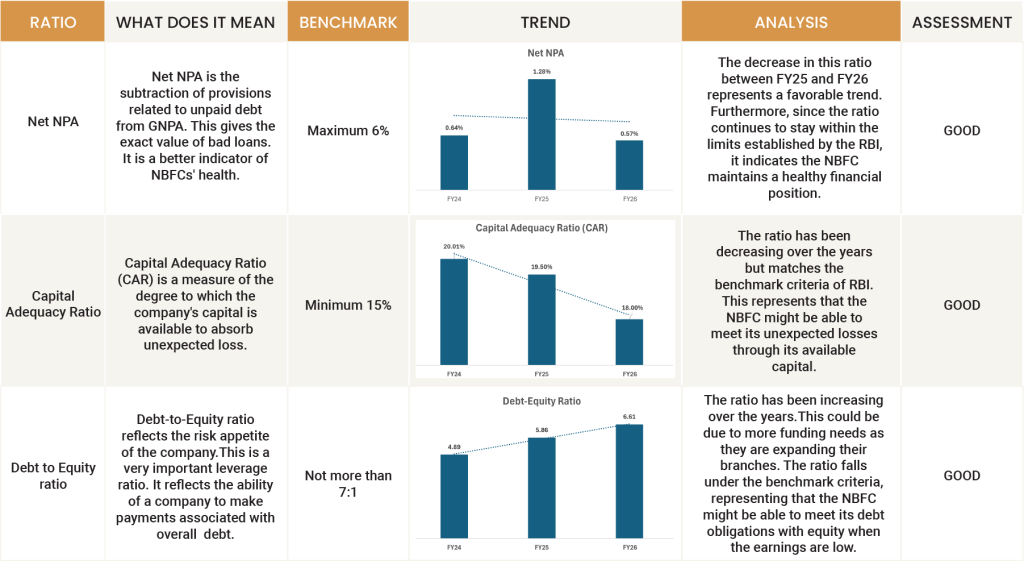

Ratio Analysis:

Should You Invest? Pros and Cons of Muthoot Fincorp NCD

Pros

- Robust Credit Profile: The NCDs are rated AA/Stable by both CRISIL and BWR, reflecting a low risk of default and a high level of safety.

- Positive Rating Momentum: CRISIL recently upgraded the rating from AA-/Positive to AA/Stable showing increased confidence in their business

- Asset Protection: As senior secured NCDs, they offer enhanced protection for investors compared to unsecured alternatives.

- Security Cover: The security cover required must be a minimum of 100% of the total of the outstanding principal balance of the NCDs and any accrued interest.

- Competitive yields: up to 9.25% vs bank FDs

- Wide tenor and payout frequencies: 24/36/60/72 Months and Monthly/ Annual/Cumulative interest payment payouts providing flexibility to investors.

- BSE listed: Provides secondary market liquidity option.

Cons

- Exposure to Gold Loan Volatility: A large portion (approx 88%) of business depends on gold loan pricing and demand cycles. Any adverse movement in collateral value could impact collections.

- Interest Rate Risk: More pronounced in longer tenors (60-72 months).

- Structural Subordination and Security Dilution: These NCDs are “subservient” meaning if the company fails, major secured creditors (like Banks) get paid first and you only get what’s left over; additionally, you must share those remaining assets equally with all other NCD holders (Pari-Passu), which reduces your individual chance of being fully repaid in case company defaults.

Must Check: To get better returns than Bank FDs, invest in NCD-IPOs online.

About Muthoot Fincorp Limited:

Muthoot Fincorp Ltd. (MFL), incorporated in 1997 and registered with the RBI, is a Kerala-based, non-deposit taking NBFC. It primarily offers small-ticket “gold loans” against household gold jewellery, a segment where it has over two decades of experience.

Muthoot Fincorp Ltd, the flagship entity of the diversified Muthoot Pappachan Group (also known as Muthoot Blue Group), also provides secured and unsecured MSME lending. Beyond lending, the company offers mutual fund and insurance distribution, foreign exchange/money transfer services, operates as a Category II Depository Participant of CDSL, and owns wind power assets in Tamil Nadu.

Its three subsidiaries are: Muthoot Housing Finance (affordable housing loans), Muthoot Microfin (micro credit to women entrepreneurs), and Muthoot Pappachan Technologies (IT services). MFL has a strong pan-India presence, operating approx. 3,781 branches (31st March, 2026) across 25 states/UTs, with key presence in Kerala, Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, and Maharashtra.

To support its next phase of growth and strengthen its capital base, the company’s Board of Directors has approved an Initial Public Offering (IPO) aimed at raising up to ₹4,000 crore.

Strengths

- Experienced management & strong promoter commitment: Promoters hold 99.87% equity stake, reflecting high confidence and long-term commitment; Muthoot Fincorp is part of the Muthoot Pappachan (Blue) Group with 138+ years legacy, backed by promoters’ deep, multi-decade expertise in gold loan and retail lending.

- Predominantly secured retail portfolio: ~96% of AUM is secured, with ~88% backed by gold jewellery and ~8% through mortgages (home loans and LAP), supporting a low-risk, small-ticket retail lending model with strong collateral cover and high recoverability.

- Adequate Capitalisation: Net worth stood at ₹6,267 Cr as of Mar ’26, supported by strong internal accruals. Gearing is moderate at 6.61x, while a healthy CRAR of 18.00% (vs. RBI minimum requirement of 15%) provides adequate buffers to support growth and maintain financial stability.

- AUM Growth: AUM rose to ₹46,193 Cr as of FY26 (vs ₹26,031 Cr in FY25 & ₹21,712 Cr in FY24). The efficiency at the branch level also saw a significant boost, with AUM/branch increasing to ₹15.2 Cr in FY26 (vs ₹9 Cr in FY25)

- Improving profitability profile: PAT increased to ₹1640 Cr in FY26 (vs ₹787 Cr in FY25 & ₹563 Cr in FY24), with Return on Managed Assets (RoMA) improving to 3.1% in FY26 (vs 2.3% in FY25 & 2.1% in FY24), driven by strong core gold loan performance.

- Healthy Asset Quality: GNPA improved to 1.03% (Mar ’26) vs 1.98% (Mar ’25), reflecting strong collection efficiency and low delinquencies in the gold loan book.

- Diversified funding profile: Funding is well diversified, with access to a wide network of PSU Banks (SBI, PNB, BoB) and private banks (HDFC, Axis, IndusInd, Federal), alongside capital market instruments (NCDs, ECBs, Subdebt, CP), supporting funding stability and refinancing flexibility.

- Strong liquidity: As of Mar ‘2026, Muthoot Fincorp had liquidity of ₹2,534 Cr (₹1,981 Cr cash & equivalents + ₹553 Cr undrawn CC/WCDL), with positive ALM gaps in the up to 1-year bucket, comfortably covering near-term debt repayments of ₹2,334 Cr over the next two months (June 2026 and July 2026)

Weakness

- Regional Concentration Risk: Around 55% of business comes from just five states (Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, and Maharashtra). This makes the company vulnerable to local economic issues, though this is an improvement from 70% in 2019.

- High reliance on the gold loan segment: While gold loans are a strength, high business concentration limits diversification benefits and makes earnings sensitive to regulatory changes (RBI’s LTV ratio) or sharp volatility in gold prices.

Invest Now: Invest in Bond IPO online in just 5 minutes

Source—Tranche IV Prospectus June 16, 2026

Disclaimer – The information is published as of date 19/06/2026 based on information available on the Tranche IV Prospectus, June 16, 2026. The information may be subject to change in case there is a change in terms of the prospectus or for any other reason as the case may be. Contents that are exclusively for educational information/knowledge sharing on capital market concepts and have no influence on the investment/sale decisions of any investors.