|

Getting your Trinity Audio player ready...

|

High Yield | BBB/Stable Rated | Minimum Investment: 10k Only

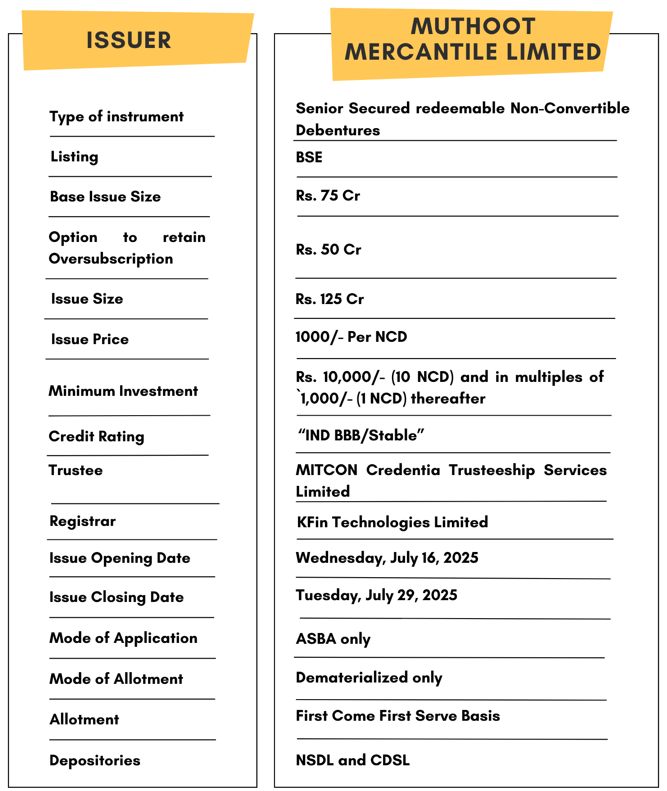

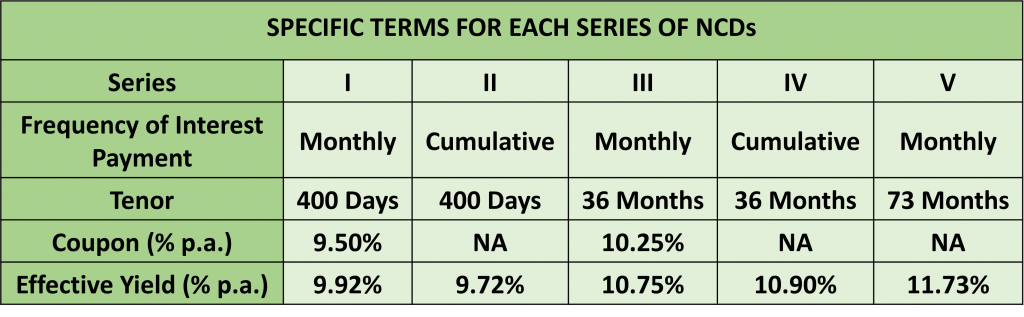

Muthoot Mercantile Limited is issuing the Non-Convertible Debentures. These NCDs are BBB/Stable rated by India Ratings and Research. The NCDs are being issued in five series: coupon ranges from 9.5% to 10.25% p.a. and different tenures of 400 days, 36 months, and 73 months. The NCDs are senior secured and redeemable in nature.

Muthoot Mercantile Limited NCD IPO: Coupon rates and effective yield for each of the series

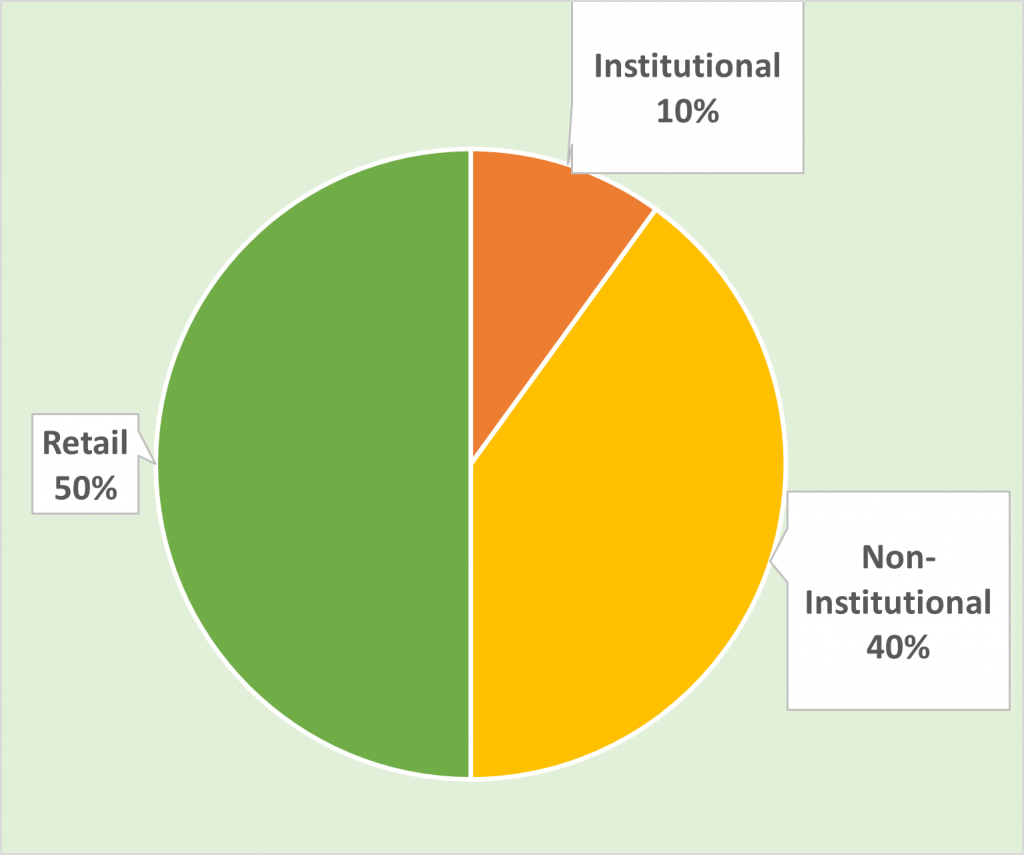

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Muthoot Mercantile Limited NCD-IPO.

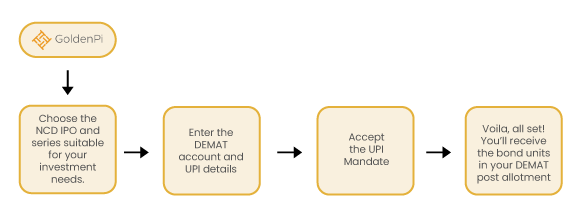

Investment Process for Muthoot Mercantile Limited NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

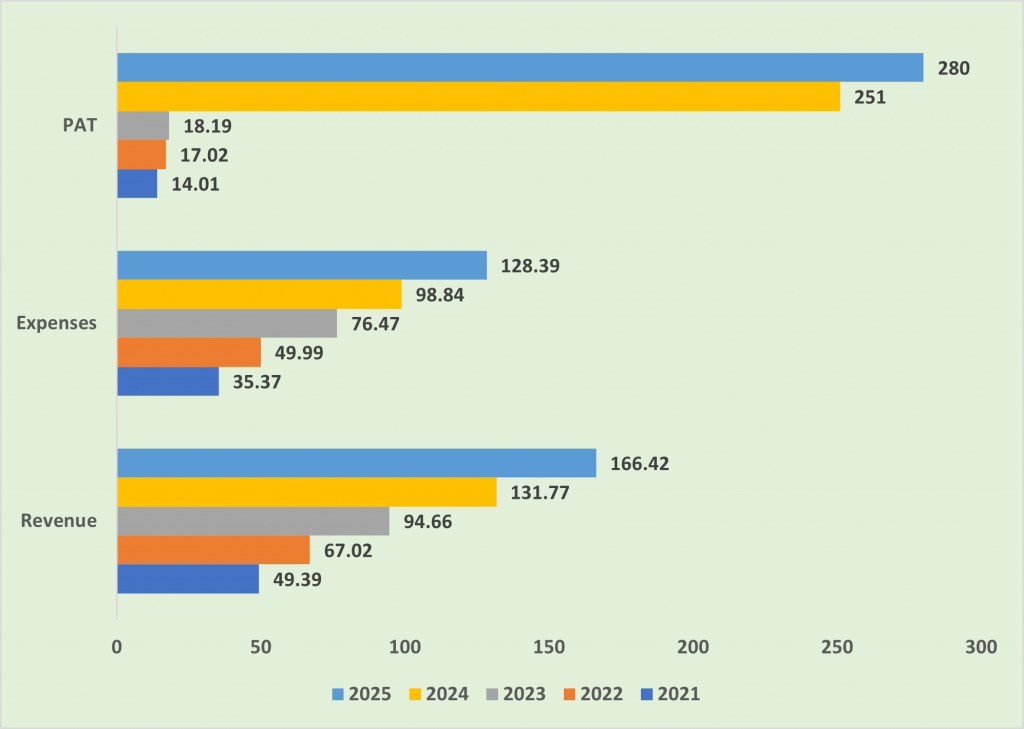

Financial Overview

Snapshot stating the Revenue, Expenses, and PAT (In crores)

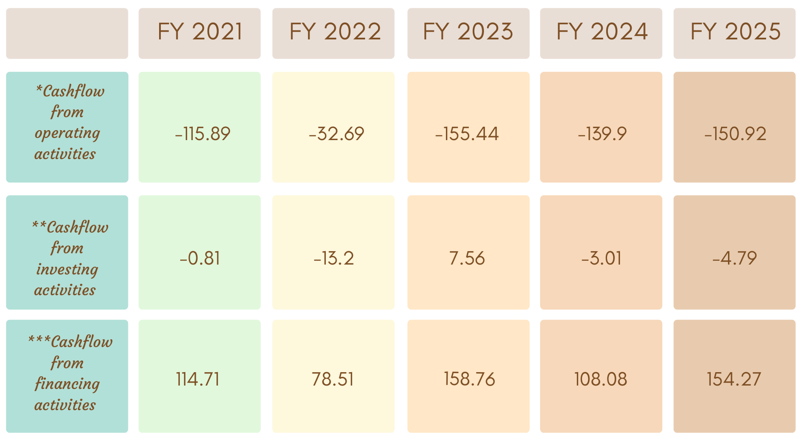

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

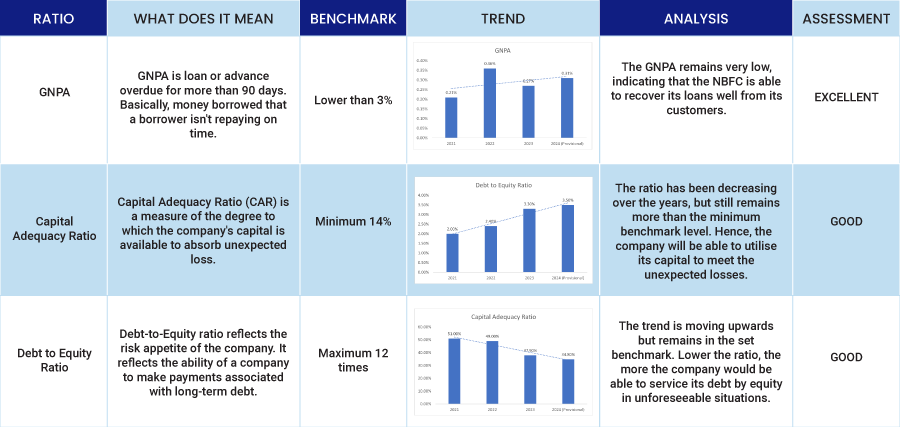

Ratio Analysis

Issue analysis

Pros

- The NCD is BBB rated security with a stable outlook.

- The coupon rate is between 9.5% to 10.25% which is much higher than FDs.

Cons

- High Gold Loan Concentration – Vulnerable to gold price volatility and regulatory changes in gold financing.

- Limited Lender Diversification – Relies on only five major lenders, increasing refinancing risk.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Muthoot Mercantile Limited

Muthoot Mercantile Limited (MML) was established as a Public Limited Company in 1997 and obtained registration as a Non-Banking Finance Company from the Reserve Bank of India in 2002. As a prominent NBFC, Muthoot Mercantile Limited serves as the flagship entity of the Muthoot Ninan Group, founded by the late M. Ninan Muthoot in 1939. The company specializes in providing loans secured against gold.

Strengths

- Robust Capital Base: Muthoot Mercantile Limited (MML) reported a strong capital adequacy ratio (CAR) of 25.4% in FY25, significantly higher than regulatory mandates, ensuring a solid risk cushion.

- Controlled Asset Quality: Gross NPAs stood at 1% and net NPAs at 0.4% by FY25-end, up slightly from FY24 (0.3% and 0.15%). The increase was attributed to a temporary IT-related issue, now resolved.

- Strong Parental Backing: As part of the Muthoot Pappachan Group, MML benefits from established brand credibility and operational synergies.

- Stable Profitability: Despite a dip in net interest margin (NIM) to 10% (FY24: 11.2%) due to higher funding costs (11.4% vs. 10.7%), MML posted a PAT of ₹280.8 million in FY25, with an RoA of 3.14%.

Weakness

- High Funding Concentration Risk: MML’s funding structure remains heavily reliant on a limited number of sources. Bank borrowings declined to 30% of total funding in FY25 (vs. 35.4% in FY24 and 47.4% in FY23), while non-convertible debentures (NCDs) gained a larger share. Notably, the company depends on just five lenders, increasing refinancing risks.

- Exposure to Gold-Linked Risks: Nearly 99.5% of MML’s AUM is tied to gold loans, making it vulnerable to fluctuations in gold prices and potential regulatory shifts in gold financing policies.

- Commodity & Regulatory Vulnerabilities: The heavy dependence on gold loans exposes MML to commodity price volatility and changes in gold lending regulations, which could impact profitability and asset quality.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus July 12, 2025

Disclaimer- The information is published as on date 07/18/2025 based on information available on Prospectus July 12, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors