The mayhem about whether to invest in Physical Gold or Sovereign Gold Bonds is absolutely intelligible. Holding Physical Gold might seem enticing to Indians for their auspicious sentiment. Yet reaping the benefits from Sovereign Gold Bonds is mostly something that the investors are unaware of. Finish the read to learn about Sovereign Gold Bond in this article!

How did the Sovereign Gold Bond come into existence?

The fact being the fact that India is the highest importer of Gold. It isn’t even a stunning fact because of the high demand for Physical Gold by consumers for the reasons we know, such as jewelry! While that made India import Gold heavily for its increasing demand, the country’s finance is at stake.

The impact is on the increase in the expenditure on imported goods and services compared to the national income received on exported goods and services. Which is termed a current account deficit in financial terminology. Meaning we are spending more money on importing than making money from exporting. Also for reasons like GDP, fluctuations in the value of the currency, and so on are as well influenced due to the Gold import. In general, the economy is adversely affected.

Does the Government have control over the demand from consumers? Well, they have no choice but to restrain the Gold import. Concerning that two schemes came into the act “Sovereign Gold Bond” and “Gold Monetization Scheme”.

After all, it’s a matter of curbing 12% of the gold import from the total import bill in India!

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowWhen did the Sovereign Gold Bond come into the act?

It was in 2015 when the Government of India brought the Sovereign Gold Bond to the attention of investors in India under the Gold Monetization Scheme. Investors generally lean on the physical yellow metal “Gold” but aren’t aware that it can also be bought through Sovereign Gold Bond which is offered by the Reserve Bank of India on behalf of the Government of India.

While Physical Gold storage needs some additional cost to be paid to the banks, the safety of the precious metal is another big concern. The Sovereign Gold Bond Scheme makes investment in Gold easier while having to carry paper as your investment security rather than the Physical Gold itself.

The current trend of being invested in Physical Gold

Indian householders have amassed with 23,000 tonnes of Gold altogether and thus get its name as “The largest holders of the gold metal” as per WGC (World Gold Council). Regardless of the benefits of the Sovereign Gold Bond Scheme, people are invested in Physical Gold. Though with multiple efforts to reduce import bills through schemes, the possession of this commodity or an asset isn’t decreasing anytime soon. Currently, the Global Gold Market size is $163.9 billion and the Indian Gold Market size is at the US $15 billion and is expected to grow!

What is Sovereign Gold Bond?

As per the Government Security Act 2006, Sovereign Gold Bonds are delivered as commodities being offered with holding certificates. That being said, Sovereign Gold Bonds are Sovereign Guaranteed which means, in case of default by the primary obligor, one can rest assured that your investment is safeguarded by the Government.

The Sovereign Gold Bonds are issued with multiple units of gold starting with a minimum investment of 1 gram and going up to a maximum of 4 kgs of investment for an individual in the fiscal year. It offers an interest of about 2.50% which is paid semi-annually having a tenure of 8 years.

It can be sold on the dates of interest paid during the 5th or 6th or 7th year as you choose to exit. So with lower market volatility and fluctuations, this is said to be a secured investment to make. With a minimum investment of the price of 1 gram of gold as in the current market, the Sovereign Gold Bond can be yours. The point to be noted is that interest gained on the Sovereign Gold Bond is taxable under Income Tax Act. The locking period of the bond is 5 years after which you are free to sell them in the secondary market but before which it is taxable.

The redemption price of the Sovereign Gold Bond is such that it considers the average price of the 999 Gold purity in the last 3 working days and that’s the price which will be redeemed on selling the bond.

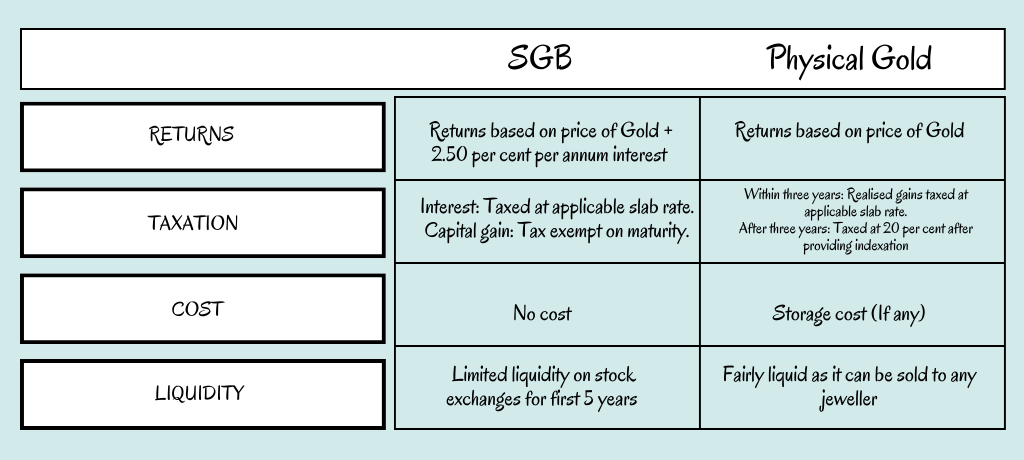

Check the comparison table to know the differences between Sovereign Gold Bonds and Physical Gold.

What is the difference between Corporate Bond and Government Bond?

Why consider investing in Gold bonds?

1. Interest Payment

Regardless of the price shooting up or falling, the interest is assured by the RBI to all the investors who have invested in the Sovereign Gold Bond. So one is likely to be paid two times a year for this investment.

2. Tax Benefits

While all the bonds are susceptible to tax deductions, the sovereign bonds have some benefits to offer in that regard. Sovereign Bonds are free from TDS. This means the tax you pay on every interest is not applicable. And in case of redeeming it before maturity, one can transfer it and even gain benefits of indexation where the capital gain can be adjusted for the inflation rate.

And in case of redeeming it after maturity then the gains are exempted from the tax. The point to consider is that the income tax needs to be filed though.

3. Low Risk and convenience

Since the security is backed by the Reserve Bank of India, there is zero probability that the issuer defaults. Though Physical Gold is a choice of investors, the convenience of investing in Gold and digitizing the process of owning it is more convenient than holding Physical Gold. The holding certificate ensures that you own the securities (Gold) involved in the investment.

4. Capital Appreciation

The demand for Gold metal is growing increasingly regardless of the economic crisis and market fluctuations. Thus the market volatility seems to be very minimal and with that being said the investment value can manifold over time.

5. Hedge against inflation

To accumulate wealth, Gold investments are the safest investment to make as the demand for it is excessively high, it can even beat the inflation rates when invested in it for a longer time. As known when the inflation rate increases, the value of the currency depreciates while the Gold value on the other hand works inversely. Meaning the value of Gold increases. That’s the reason why being invested in Gold is a savior at times when there is an economic crisis.

6. Long-term investment

The Sovereign Gold Bond is great to be invested in for a longer time as it is for 8 years. While it assures the investors of returning the principal amount, it as well gives capital gains.

7. A means of portfolio diversification

In an investment portfolio having a set of instruments is a norm but the sentiments of the market are always unknown. While the equity or the stocks are at the peak of downward movement, the gold commodity appears to play a positive trend. Thus, when the stocks aren’t in favor, Gold can turn the portfolio either by nullifying the losses or by keeping the portfolio on the positive side.

8. Loan facility

When in need of money, the Sovereign Gold Bond can aid in availing it. While you are invested in this bond, getting a loan isn’t difficult at all by approaching the concerned financial institution. So up to 75% of the market value of the bond can be leveraged as collateral to issue a loan against it.

How does inflation affect the bond price?

Features of Sovereign Gold Bond

1. Eligibility

To invest in Sovereign Gold Bonds, one needs to be a resident of India, which is the primary requirement of the bond scheme. If that’s so, continue to read on.

2. Interest Payout

During the issue of the Sovereign Gold Bond, the interest rate would be made clear by the RBI. It is generally 2.5% per annum paid semi-annually that is twice a year.

3. Fixed Tenor

The tenor is for 8 years and in case of selling before maturity, it is made available to investors after 5 years of the locking period. So it is not possible to sell before 5 years and the redemption of the bond after the locking period is done during the dates of interest payments hence redemption must be informed well before the dates.

4. Reselling in the stock market

Having held the digitized holding certificate of the subscription to the Sovereign Gold Bond, one can resell it by trading in the secondary market after 14 days of investing in it. Although the price of gold price depends on the supply and demand in the market as well as on the price at which the gold rate is on the day of selling.

5. Limit of Subscription

An individual can invest in as minimum as the price of 1 gram of gold and a maximum of up to 4 kg for a fiscal year, which is as well applicable to Hindu Undivided Families. And in the case of trusts and corporations, they can hold up to 20 kgs of gold.

Risk of investing in Gold Bonds

The risks in SGB are the bare minimum and hardly something to consider as a risk. Yet it is contemplated so that the investors know.

1. Loss of capital

It is known that the price of these bonds is related to the price of gold. The investment might seem viable when the market is bullish and the capital invested gets appreciated but it’s riskier when the market is on a downtrend which indicates that the capital depreciates and that’s when you lose the money from the capital as the selling price is lesser than the buying price. But RBI ensures that the price of the commodity is stable and is not fluctuating more. Hence the probability of capital loss is not the usual case and is mostly rare, unlike stocks.

2. Long maturity

The time for sovereign gold bond maturity is 8 years which is quite a long time to be invested in and until the lock-in period, the bond is not redeemable. It is indeed a frustrating thing to be in but 5 – 8 years is kept so that the volatility of the gold price is in control during that time to avoid incurring losses.

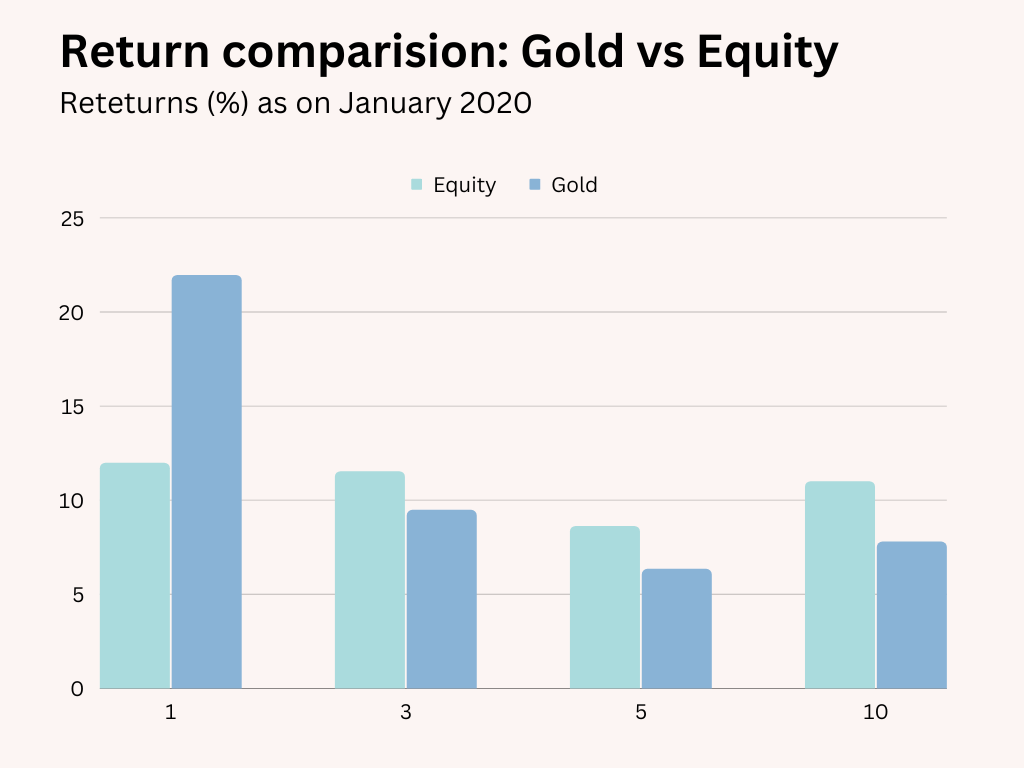

Comparison between gold and equity

The chart below shows the return on a longer time frame for a greater understanding.

If the thought process is such that Gold is a permanent wealth and has aided in passing troubles in history, conclusively a savior at the bad times, then investing a portion in Sovereign Gold Bonds must be an ideal thing over carrying physical gold.

If the thought process is such that Gold is a permanent wealth and has aided in passing troubles in history, conclusively a savior at the bad times, then investing a portion in Sovereign Gold Bonds must be an ideal thing over carrying physical gold.

In the longer term, Gold doesn’t really perform as well as equity. Though for the short term it seems attractive as the investment seems worthy only when there is someone else to pay you more when you are selling. In the long run, it might not work the same where the returns will be lesser than that of the equity. That is a fact that gold as an asset isn’t adding any value to economic activity. So, for wealth creation gold is definitely not the right investment.

In a nutshell!

In times of financial stress in the economy, Gold has served as an alternative to currency. Generally, the perspective exists amongst the population that Gold is as equivalent to stocks for getting higher returns, however, which is not. Gold is an unproductive asset that has no impact on the growth of the economy and hence perceiving it as currency makes more sense to be invested in it.

Back in time, Gold was used like money before even paper currency came into play. And considering it as a currency still holds good as it doesn’t influence the economy in any way.

To make significant returns in short term it is still a good investment. With that being said, including 5-10% of your portfolio with Gold investment is a good way to stay up with inflation risks, as known when money loses its value, gold makes its stride to keep you in a better position, financially. So why not consider investing in Sovereign Gold Bond than just purchasing the Physical Gold to keep it in the locker?