|

Getting your Trinity Audio player ready...

|

Introduction: A CRAMS Powerhouse

Dishman Carbogen Amcis Limited (DCAL) is a globally recognized Contract Research and Manufacturing Services (CRAMS) company with over 40 years of expertise in pharmaceutical APIs, high-potent APIs, intermediates, and specialty chemicals. Headquartered in India, DCAL operates 25 manufacturing facilities across India, Switzerland, France, the UK, China, and the Netherlands, serving 250+ global clients, including Novartis, Daiichi Sankyo, and Takeda.

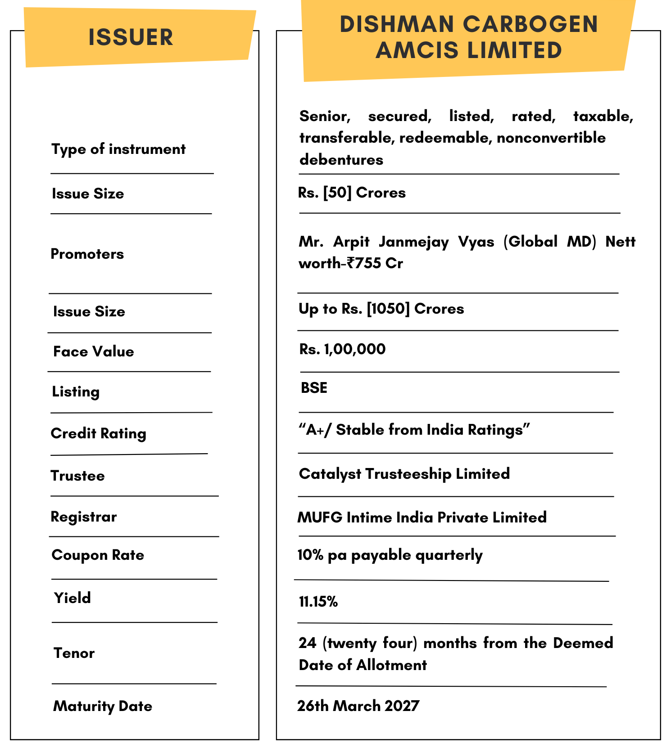

DCAL is now tapping the debt market with a new issuance of ₹50 crore senior secured, rated, listed, redeemable non-convertible debentures (NCDs), offering investors a chance to participate in a well-established yet rapidly evolving global pharma player.

Financial Overview

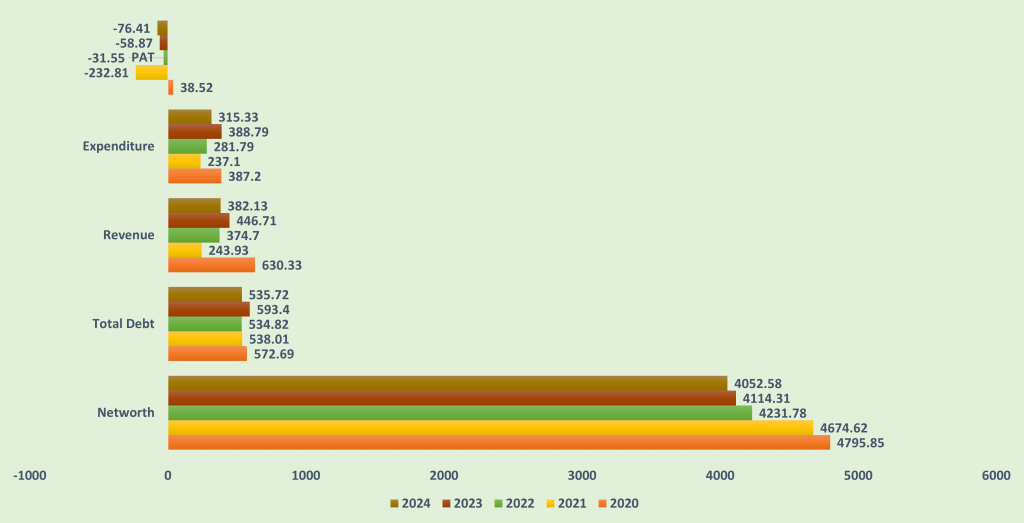

Snapshot stating the Revenue, Expenses, Net Worth, Total Debt and PAT (In crores)

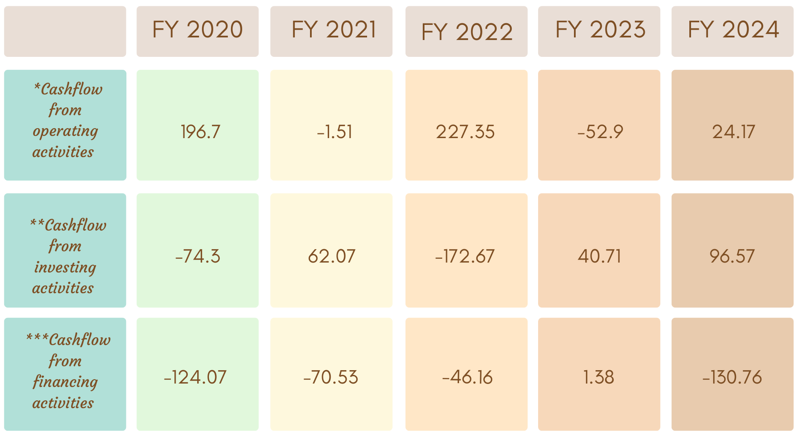

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

Revenue & Profitability

- Consolidated Revenue (FY24): ₹2,616 Cr, up 8% YoY (FY23: ₹2,413 Cr).

- EBITDA (adjusted): ₹444 Cr (FY23: ₹457 Cr); margin at ~17%.

- Net Loss (FY24): ₹153 Cr, impacted by one-time expenses (France plant launch, SAP implementation, EDQM resolution).

- Cash Profit stood at ₹278 Cr (FY23: ₹309 Cr).

Business Segments

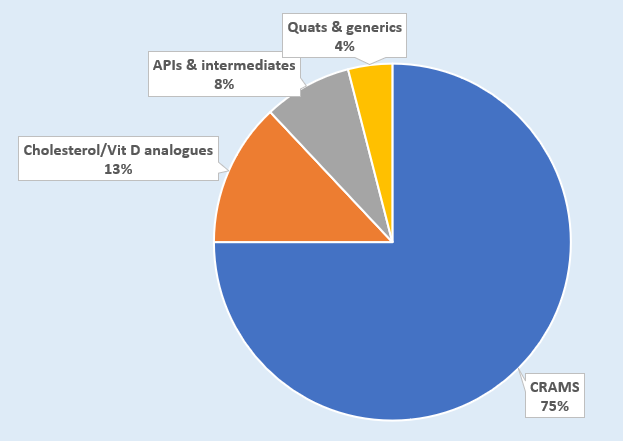

- CRAMS contributes 75% of revenue (₹1,954 Cr); focus on oncology, CNS, and rare diseases.

- Other segments: Cholesterol/Vit D analogues (13%), APIs & intermediates (8%), Quats & generics (4%).

Capex & Growth Investments

- ₹1,555 Cr invested in EU expansion (FY20-FY24).

- Operationalized new injectable facility in France; expected Euro 16.5 Mn in confirmed orders in FY25.

- Bavla facility received regulatory clearances from PMDA (Japan) and EDQM (Europe) in early 2024.

Key Strengths of Dishman Carbogen Amcis Limited

Asset-Backed Security for NCD Investors

- 1.1x value of immovable commercial properties of Dishman Carbogen Amcis Ltd (₹10 Cr loan).

- 1.25x value of Dishman Infrastructure Ltd’s industrial land (₹40 Cr loan).

- First charge on all current and fixed assets of Dishman Infrastructure Ltd, ensuring investor protection.

Strong Promoter Guarantee & Financial Strength

- Unconditional and irrevocable corporate guarantee from Mr. Arpit Janmejay Vyas (Global MD), who has a net worth of ₹755 Cr and drew a salary of ₹8.35 Cr in FY24 from a Swiss subsidiary.

- Cash Collateral of ₹3 Cr maintained as a Debt Service Reserve Account (DSRA), placed as an interest-free deposit ensuring liquidity for interest payments.

Stable Revenue Growth & Improving Profitability

- Consolidated revenue grew by 8% YoY, from ₹2,413 Cr in FY23 to ₹2,616 Cr in FY24.

- EBITDA improved from ₹332 Cr (FY23) to ₹396 Cr (FY24), despite regulatory and operational challenges.

- Order book of CHF 120 Mn (₹1,000+ Cr), with expected inflows of CHF 18-20 Mn (₹150-160 Cr) into India over the next 2-3 years.

Global CRAMS Leader with Strong Infrastructure

- 25 manufacturing facilities & 28 R&D labs across 6 countries, approved by USFDA, EDQM, PMDA, Swiss Medic, and WHO.

- 40+ years of experience in CRAMS, APIs, and specialty chemicals.

- 2,200+ employees, 950+ scientists in R&D, with 50% holding Ph.D. degrees, ensuring innovation-driven growth.

Regulatory Clearances & Business Stability

- Bavla (India) facility cleared EDQM & PMDA audits (Jan & Feb 2024), enabling new business from Europe.

- No customer loss despite regulatory hurdles, demonstrating high client stickiness (switching suppliers takes 24-36 months).

Strong Market Presence & Liquidity

- Listed on NSE & BSE with a market cap of ₹4,231 Cr (Dec 2024).

- 95% revenue from exports, primarily from Europe (major share) and the US.

- Cash & equivalents: ₹392 Cr (1H25), supporting short-term obligations.

Geographic Reach & Revenue Sources

- Over 95% revenue from exports

- Major markets: Europe, US, Japan

- CHF 120 Mn order book (Dec 2024), a testament to long-term CRAMS demand

Key Risks & Weaknesses

High Debt Levels & Leverage

- Consolidated Net Debt/EBITDA at 5.9x (FY24), indicating elevated leverage.

- Short-term borrowings (₹923 Cr in 1H25) could pressure liquidity if EBITDA growth slows.

Margin Pressure Due to Rising Costs

- EBITDA margin declined to 17% in FY24 (vs. 19% in FY22) due to:

- Higher raw material costs.

- One-time expenses (SAP implementation, EDQM compliance).

- Initial losses from new French injectable facility (₹46 Cr impact in FY24).

Pending Tax Litigation (Contingent Liability)

- Income tax demand of ₹346 Cr (₹180 Cr related to goodwill amortization dispute).

- ₹56 Cr paid under protest; appeal filed with CIT/ITAT.

Working Capital Challenges

- Long working capital cycle (~390 days) due to:

- Raw material lead time (75-120 days).

- Manufacturing & shipping delays (270-300 days).

- Customer credit period (75-120 days).

Concentration in Oncology

- ~50% of CRAMS revenue is oncology-focused, exposing the business to therapeutic segment-specific risks

Capacity Utilization Still Ramp-Up Mode

- Indian facilities:

- Bavla: 50% utilization (FY24)

- Naroda: Dropped from 85% (FY23) to 70% in FY24

- Some overseas facilities (e.g. Shanghai) remain underutilized (35%)

Debt Servicing Ability

Liquidity Position

- Cash & equivalents: ₹392 Cr (1H25).

- DSRA of ₹3 Cr ensures interest payment security.

- Short-term debt: ₹923 Cr (1H25) vs. operating cash flow of ₹59 Cr (1H25) – needs monitoring.

- Listed on NSE & BSE, with public holding of 40.68%

- Business is cash-generating with strong export receivables; however, working capital cycles remain elongated due to the nature of CRAMS operations

- Expected cash inflow of INR 150-160 Cr to standalone entity over 2–3 years from the CHF 120 Mn orderbook

Debt Repayment Schedule

- Major repayments due in FY26 (₹258 Cr) & FY27 (₹974 Cr).

- Bullet repayment of CHF 100 Mn (₹913 Cr) in FY27 (Swiss loan).

- Market-linked debentures (₹58 Cr) due in FY26 – refinancing risk exists.

Interest Coverage Ratio (ICR)

- ICR at 2.6x (1H25), down from 6.6x in FY21, but still manageable.

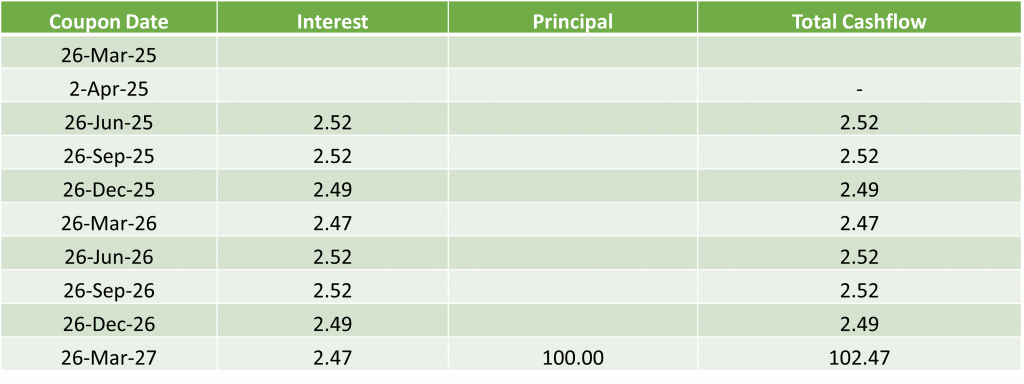

Cashflow for 10.00% Dishman Carbogen Amcis Limited 2027

Investment Verdict: Should You Invest in DCAL’s NCDs?

✅ Reasons to Invest

✔ Secured NCDs backed by real estate & promoter guarantee.

✔ Stable revenue growth (8% YoY) & improving EBITDA.

✔ Strong global CRAMS business with high entry barriers.

✔ Regulatory clearances (EDQM, PMDA) to drive future orders.

⚠️ Caution Points

- High leverage (Net Debt/EBITDA at 5.9x).

- Working capital delays & tax litigation risks.

- FY26-27 debt repayments need refinancing/strong cash flows.

Final Takeaway

DCAL’s NCDs offer a moderate-risk, asset-backed investment with stable cash flows from a globally diversified CRAMS player. However, investors must monitor debt repayment schedules, margin recovery, and regulatory risks.

For risk-averse investors, the asset security and promoter guarantee provide comfort, while aggressive investors may look for higher yields if DCAL’s growth trajectory improves.

Disclaimer: This is not investment advice. Conduct your own due diligence before investing.