|

Getting your Trinity Audio player ready...

|

High Yield | CRISIL A+/Stable | Minimum Investment: 10k Only

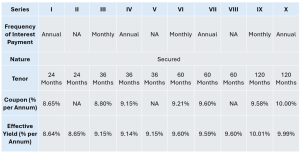

Edelweiss Financial Services Limited is issuing the Non-Convertible Debentures. These NCDs are A+/Stable rated by CRISIL. The NCDs are being issued in ten series: coupon ranges from 8.65% to 10.00% p.a. and different tenures of 24 months, 36 months, 60 months and 120 months . The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series:

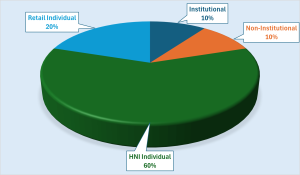

Allocation Ratio:

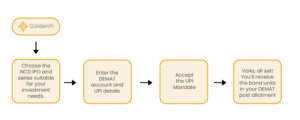

Investment Process for Edelweiss Financial Services Limited NCD IPO:

You can invest in IPOs via GoldenPi in these easy steps.

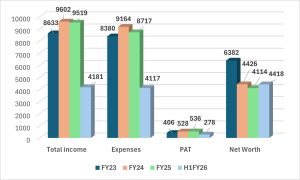

Financial Overview:

Snapshot stating the Total Income, Expenses, PAT and Net Worth (In crores):

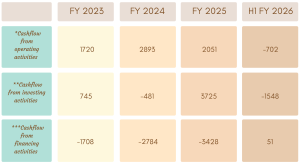

Cash flow for last few years (In crores):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

Issue analysis

Pros:

- Strong Credit Rating: Rated Crisil A+/Stable indicating high degree of safety and low credit risk.

- Secured NCDs: Senior, secured NCDs backed by pari-passu charge on loan and advances, receivables, investments, stock in trade, current & other assets, immovable property / fixed assets.

- Security Cover: The security cover required must be a minimum of 100% of the total of the outstanding principal balance of the NCDs.

- Competitive yields: up to 10.01% vs bank FDs (6-7.8%).

- Wide tenor and payout options: 24/36/60/120 Months and Monthly/ Annual interest payment option providing flexibility to investors.

Pros:

- Interest Rate Risk: More pronounced in longer tenors (60 and 120 months).

- Profitability Pressure: Core profitability revival has been slower than expected; high monitorable loan portfolio adds risk.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Edelweiss Financial Services Limited:

Edelweiss Financial Services Limited is one of India’s leading financial services conglomerates, offering a robust platform to a diversified client base across domestic and global geographies. The company has mainly four business verticals namely Retail Credit, Asset Management, Asset Reconstruction and Insurance services. Apart from that the company has also been providing Merchant Banking services since 1995. Edelweiss Financial Services Limited is listed on the stock exchange having a market capitalization of more than ₹10,800 Crores as of Feb ‘2026.

Strengths:

- Strong Edelweiss Brand and Pan-India distribution network: Edelweiss possesses a robust brand presence within the financial services sector, built upon a reputation for consistent execution and innovation. The company operates across India with a total of 260 offices nationwide.

- Experienced management team: leadership is stable, characterized by extensive experience. Chairman & MD, Rashesh Chandrakant Shah ( 35+ yrs in financial services), and Vice Chairman & Director, Venkatchalam A Ramaswamy (30+ Yrs). Senior Management also has substantial, long-tenured expertise in the BFSI industry.

- Strong Institutional Backing: Promoters hold 33%, FIIs hold 18.3% and DIIs & Non Institutions hold 48.3%. Marquee investors include TIAA CREF funds (3.6%), LIC (2.6%), Vanguard group (2.4%), Blackrock (1.3%), and Barclays (0.9%).

- Strong funding partners and Network: JP Morgan, HSBC, Bill & Melinda gates foundation, Bank of Baroda, TATA Trusts, HCL, WIPRO, ICICI Prudential.

- Diversified business model : Presence in Asset reconstruction (ARC), asset management (Alternate asset & Mutual Funds), Credit (MSME & Mortgages ), Insurance (Life & General) – mitigates reliance on lending alone.

- Adequately capitalised: Edelweiss group NBFCs – ECL Finance (30.13%), Nido Home Finance (29.52%), and Edelweiss ARC (85.21%) – are well-capitalized, with CRAR significantly above the RBI’s 15% minimum.

- Stable asset quality: The Net-NPA for the three credit entities (ECL Finance, Nido Home Finance, Edelweiss Retail Finance Limited) remained controlled: 1.70% (FY25), 1.29% (FY24), and 1.36% (FY23).

- Meaningful deleveraging over medium term: Net debt reduced materially from ₹18,550 crore (Mar’22) to ₹11,170 crore (Mar’25), reflecting balance sheet repair through recoveries, stake sales and fee-led earnings; debt rose marginally to ₹11,334 crore by Sep’25 due to corporate borrowings.

- Asset management franchise has scaled steadily: AUM increased from ₹45,310 crore (Mar’25) to ₹47,670 crore (Sep’25); mutual fund AUM scaled from ₹38,192 crore (Mar’24) to ₹54,600 crore (Sep’25), supporting recurring fee income.

- Wholesale lending risk meaningfully reduced: Wholesale loan book declined sharply from ₹4,879 crore (Mar ’23) to ₹307 crore (Sep’25), materially lowering tail risk compared with earlier cycles.

- Strong liquidity and positive ALM: Expected inflows of ~₹11,300 cr along with cash and bank balance of ~₹5,600 cr comfortably cover ~₹11,500 cr of outflows over Jan-Dec 2026, supported by positive ALM gaps across all tenors (≤1 year: +₹900 cr; 1-3 years: +₹300 cr; 3+ years: +₹4,700 cr), indicating low refinancing risk.

Weaknesses:

- Profitability improving but still modest for scale: RoA improved from ~1.2% in FY24 to ~1.3% in FY25; however, earnings remain below large diversified peers and are partly supported by fair-value gains and deferred tax assets.

- Stressed asset overhang persists despite reduction: Gross Stage III assets declined from ~10.2% (Mar’23) to 8.0% (Sep’25), but remain elevated; net monitorable portfolio reduced from ₹6,018 crore (Mar’24) to ₹3,892 crore (Sep’25), still high by sector standards.

- Insurance businesses still drag consolidated returns: Life and general insurance arms remain loss-making, though losses have reduced versus prior years; breakeven expected only over the next 1-2 fiscals.

- Declining net worth: Drop to ₹ 5,866 Cr crore as of Dec ’2025 vs ₹ 6,381 crore Mar ‘ 2023) after dividend distributions and mark-downs in Security receipts (SRs).

- Slow growth in retail/AM lending: Retail and MSME lending growth has been relatively muted.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus February 23, 2026

Disclaimer – The information is published as on date 27/02/2026 based on information available on Prospectus February 23, 2026. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors