")

|

Getting your Trinity Audio player ready...

|

High Yield | A+/Stable | Minimum Investment: 10k Only

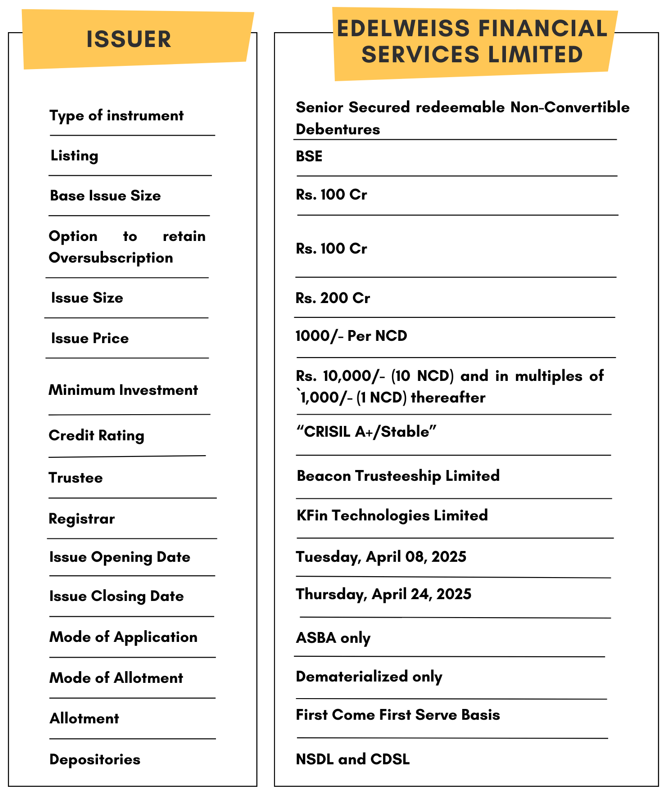

Edelweiss Financial Services Limited is issuing the Non-Convertible Debentures. These NCDs are A+/Stable rated by CRISIL. The NCDs are being issued in twelve series: coupon ranges from 9.5% to 11% p.a. and different tenures of 24 months, 36 months, 60 months and 120 months . The NCDs are secured and redeemable in nature.

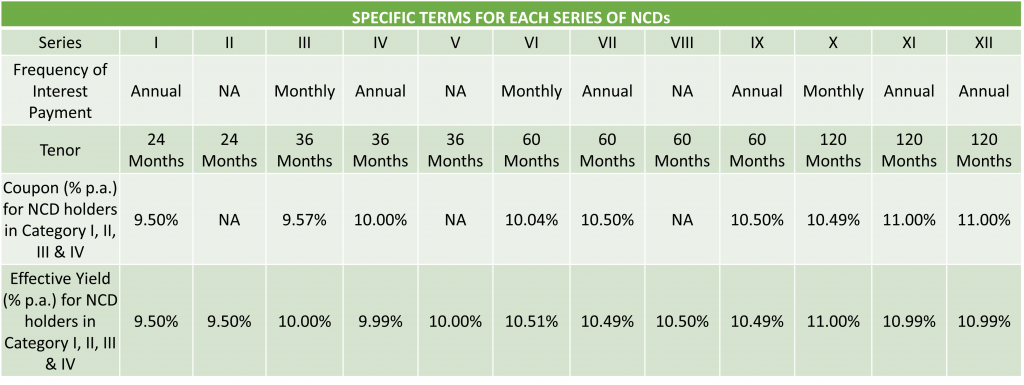

Edelweiss Financial Services Limited NCD IPO: Coupon rates and effective yield for each of the series

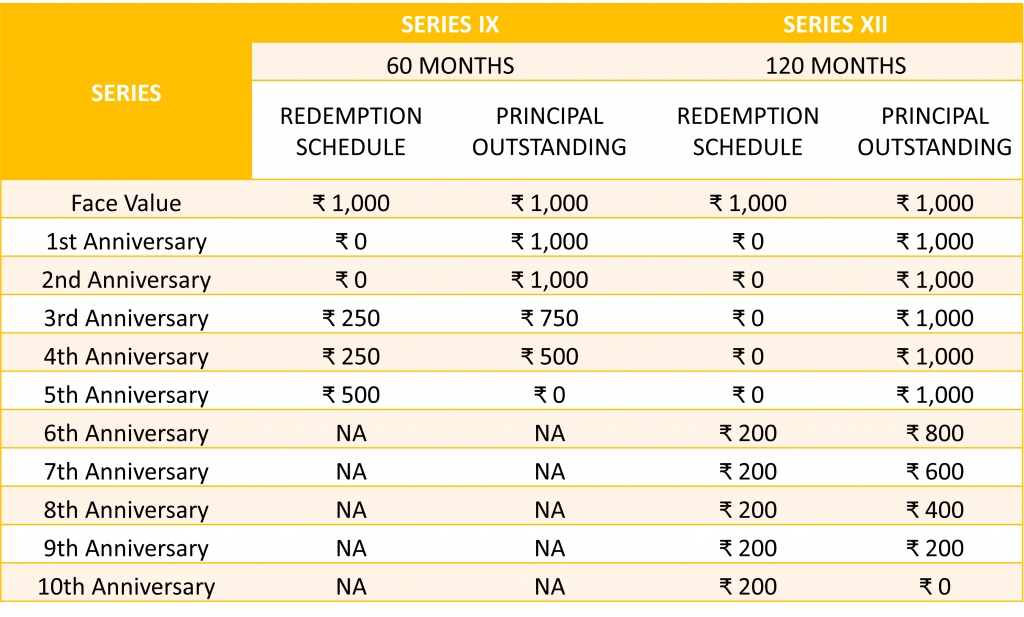

Redemption Schedule

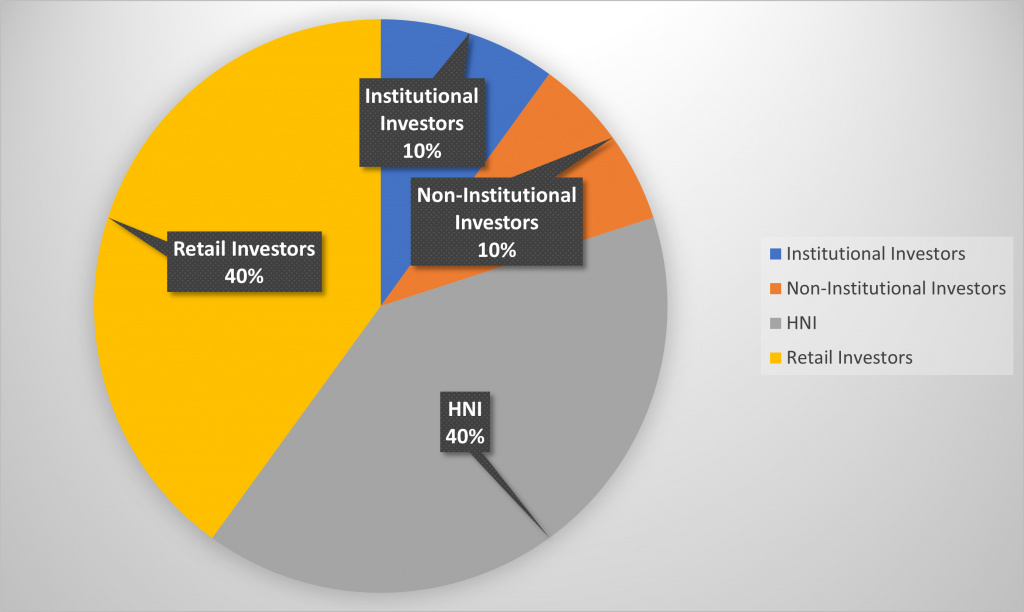

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Edelweiss Financial Services Limited NCD-IPO.

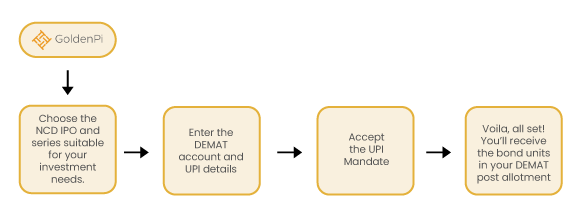

Investment Process for Edelweiss Financial Services Limited NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

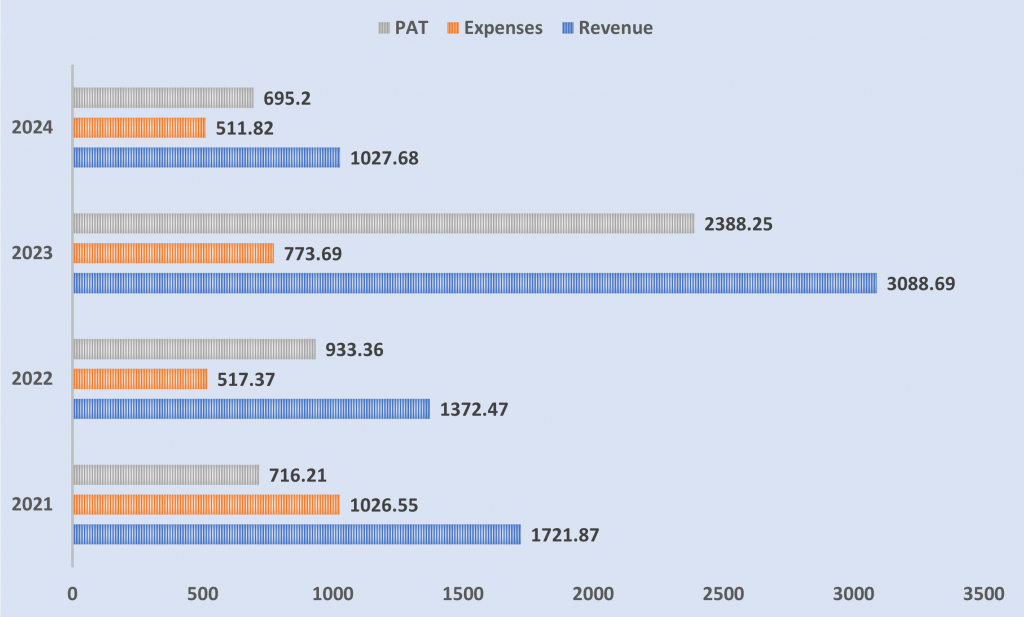

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

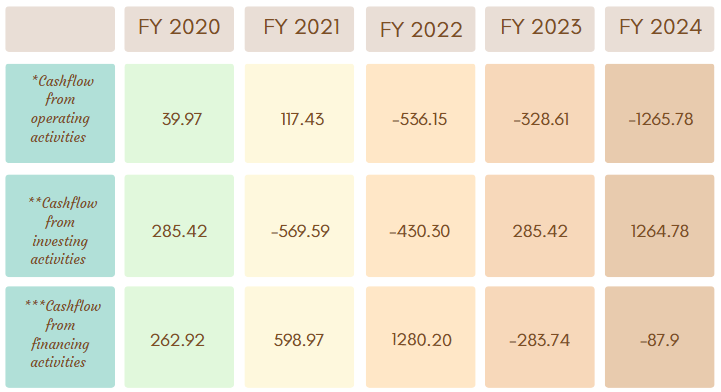

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

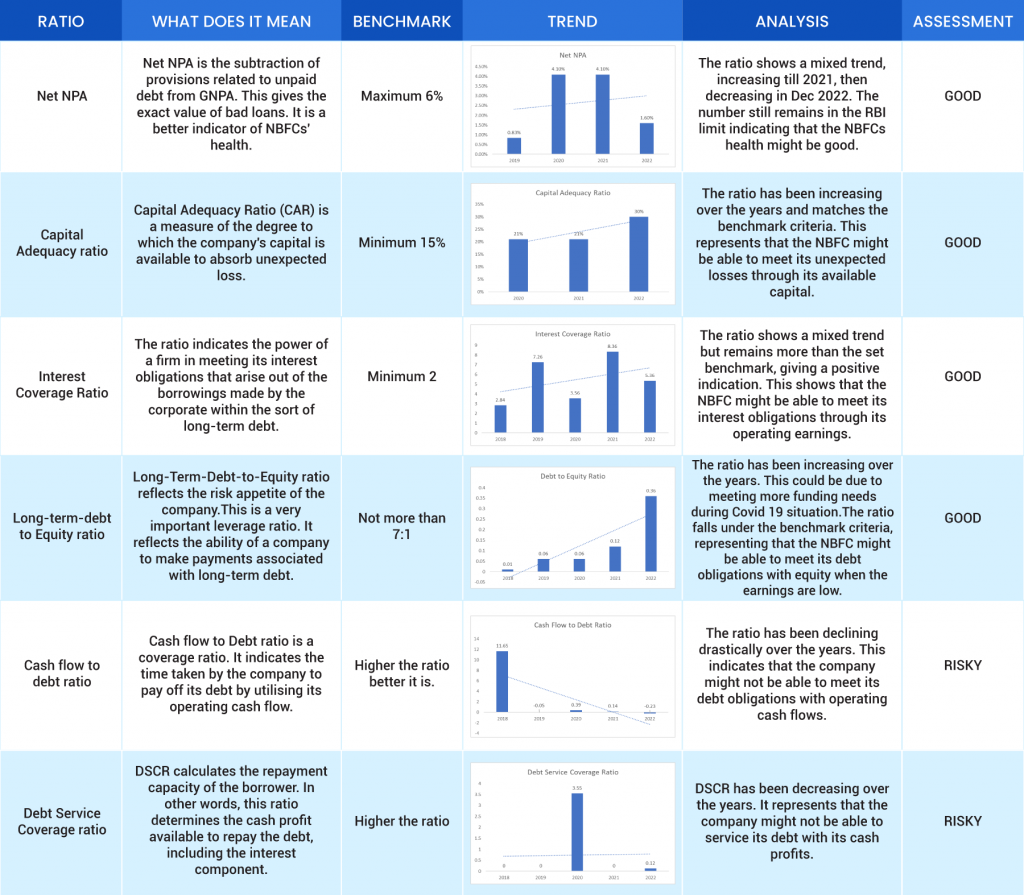

Ratio Analysis

Issue analysis

Pros

- Attractive Coupon Rates: Offers up to 11.00% per annum depending on series and tenure, providing strong returns for fixed-income investors.

- Strong Diversification: Edelweiss Group operates across credit, insurance, asset management, and ARC businesses, reducing dependence on a single income stream.

- Adequate Capitalization: Net worth stood at ₹6,386 crore as of Sep 2024, with a moderate gearing ratio of 3.0x, reflecting a reasonably managed capital structure.

- High Liquidity Buffer: Maintains ₹29 billion in available liquidity (~14% of borrowings) through unencumbered assets and bank lines.

- Leading ARC Position: Edelweiss ARC is the largest in India, managing ₹28,910 crore in securities receipts as of Sep 2024, showing dominance in distressed assets.

Cons

- Declining Net Worth: Dropped from ₹8,581 crore in FY23 to ₹6,386 crore in Sep 2024, largely due to Nuvama demerger payout.

- High Gearing Level: Although manageable, a 3.0x gearing level is on the higher side, which could pose risk in a stressed scenario.

- Credit Risk from ARC Exposure: Heavy presence in asset reconstruction could face headwinds during economic downturns or regulatory tightening.

- Group Restructuring Ongoing: Plans to exit housing, alternate assets, and general insurance may bring execution risks and transitional uncertainty

Liquidity

As of December 15, 2024, EFSL maintained a strong liquidity buffer of ₹4,040 crore, comprising:

- ₹2,458 crore in bank balances, fixed deposits, and mutual funds

- ₹1,323 crore in unencumbered short-term loans and exchange margins

- ₹259 crore in available credit lines

This buffer is sufficient to cover 6 months of debt obligations and operational expenses without relying on new inflows or fundraising.

Additionally, the group raised:

- ₹1,841 crore in H1 FY25

- ₹764 crore in Q3 FY25 (till December)

via NCDs, term loans, CPs, and structured products—demonstrating continued access to diverse funding sources.

EFSL also monetized assets by selling a 7.14% stake in Nuvama Wealth Management for ₹1,769 crore, expected to be used for high-cost debt repayment, further boosting liquidity strength.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Edelweiss Financial Services Limited

Edelweiss Financial Services Limited is one of India’s leading financial services conglomerates, offering a robust platform to a diversified client base across domestic and global geographies. The company has mainly four business verticals namely Retail Credit, Asset Management, Asset Reconstruction and Insurance services. Apart from that the company has also been providing Merchant Banking services since 1995. Edelweiss Financial Services Limited is listed on the stock exchange having a market capitalization of more than 6,000 Crores as of July,2024.

Strengths

- Capital Raising Capability:

- Since 2016, the Edelweiss group has successfully raised approximately ₹6,000 crore across various businesses, including lending, wealth management, and asset management.

- This consistent ability to attract capital has bolstered the group’s capital position, enabling it to absorb asset-side risks effectively.

- Asset Monetization:

- In December 2024, the group divested a 7.14% stake in Nuvama Wealth Management, generating ₹1,769 crore.

- The proceeds from this sale have enhanced liquidity and are expected to be utilized for repaying high-cost debt, thereby improving financial flexibility.

Weaknesses

- Regulatory Restrictions:

- In May 2024, the Reserve Bank of India (RBI) imposed restrictions on ECL Finance Ltd (ECLF) and Edelweiss Asset Reconstruction Company Ltd (EARC), both subsidiaries of EFSL.

- ECLF was directed to cease structured transactions related to wholesale exposures, and EARC was restricted from acquiring financial assets, including security receipts.

- These actions have impacted the group’s operational flexibility and are key rating sensitivity factors.

- Elevated Monitorable Portfolio:

- As of September 30, 2024, the group’s monitorable portfolio stood at ₹8,750 crore, including gross stage III accounts in the lending book (₹738 crore), security receipts held by the group (₹6,517 crore), and loans sold down to Alternative Investment Funds (₹1,495 crore).

- While this represents a reduction from ₹12,097 crore as of March 31, 2022, the portfolio remains substantial, indicating ongoing asset quality concerns.

- Profitability and Capitalization Risks:

- Potential incremental provisioning requirements on the monitorable book could adversely affect profitability and capitalization.

- The group’s ability to manage these risks and restore fund-raising capabilities for its lending business remains a critical rating sensitivity.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus March 27, 2025

Disclaimer- The information is published as on date 04/07/2025 based on information available on Prospectus March 27 , 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors