|

Getting your Trinity Audio player ready...

|

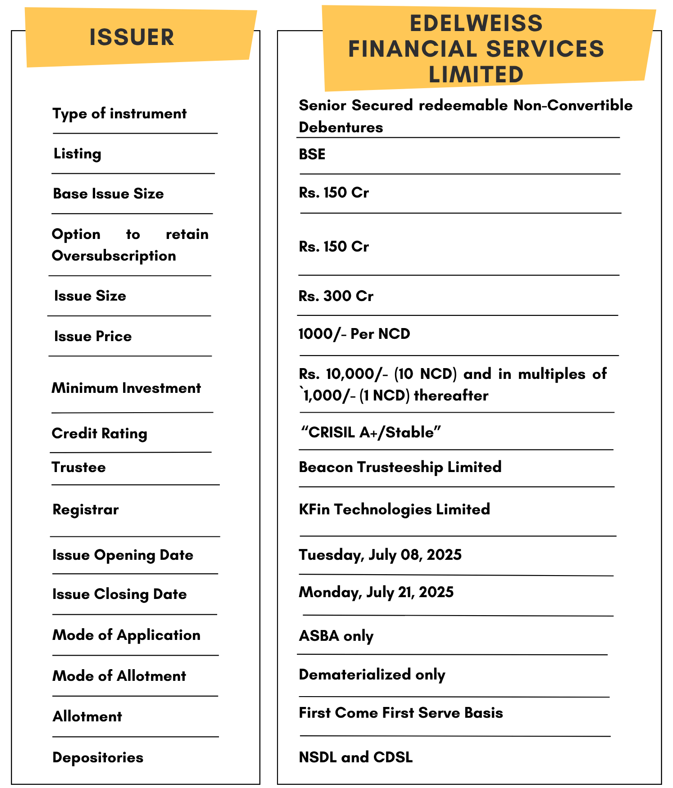

High Yield | A+/Stable | Minimum Investment: 10k Only

Edelweiss Financial Services Limited is issuing the Non-Convertible Debentures. These NCDs are A+/Stable rated by CRISIL. The NCDs are being issued in twelve series: coupon ranges from 9% to 10.5% p.a. and different tenures of 24 months, 36 months, 60 months and 120 months . The NCDs are secured and redeemable in nature.

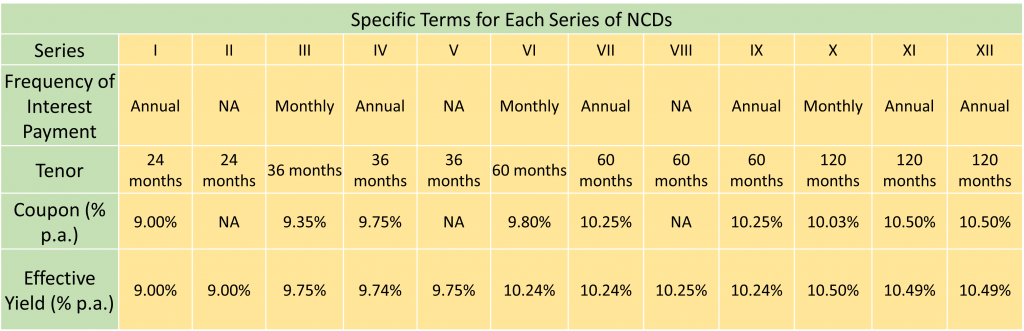

Edelweiss Financial Services Limited NCD IPO: Coupon rates and effective yield for each of the series

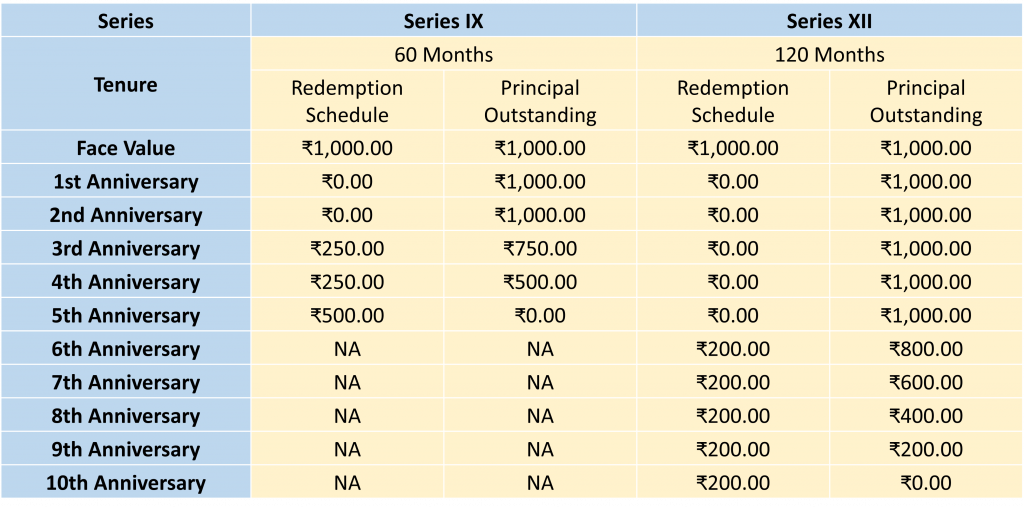

Principal Redemption Schedule and Redemption Amounts

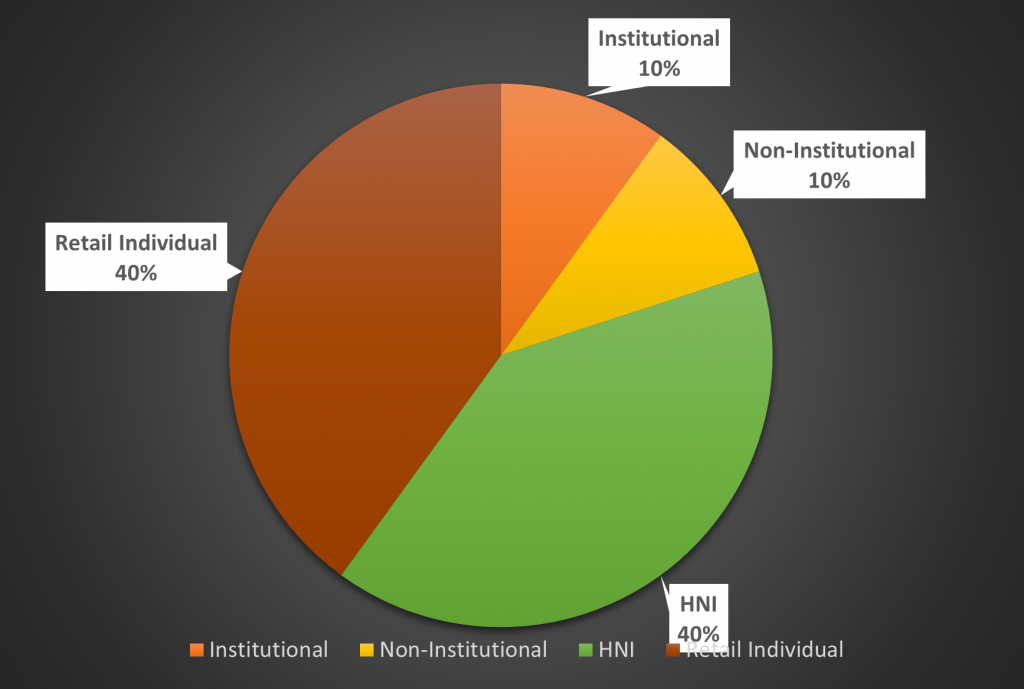

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Edelweiss Financial Services Limited NCD-IPO.

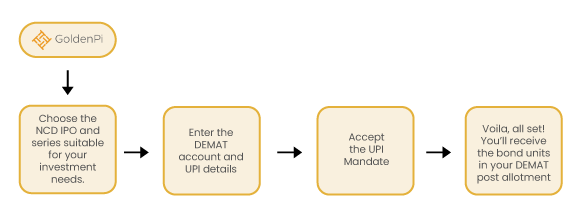

Investment Process for Edelweiss Financial Services Limited NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

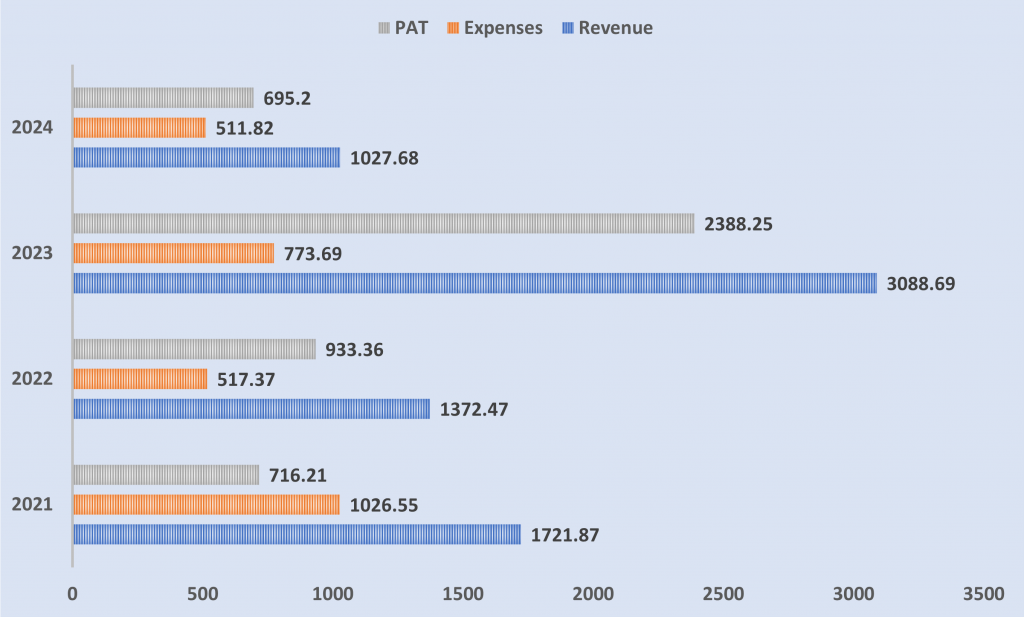

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

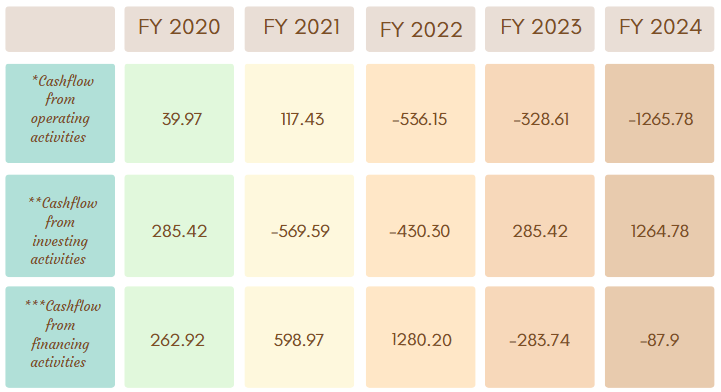

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

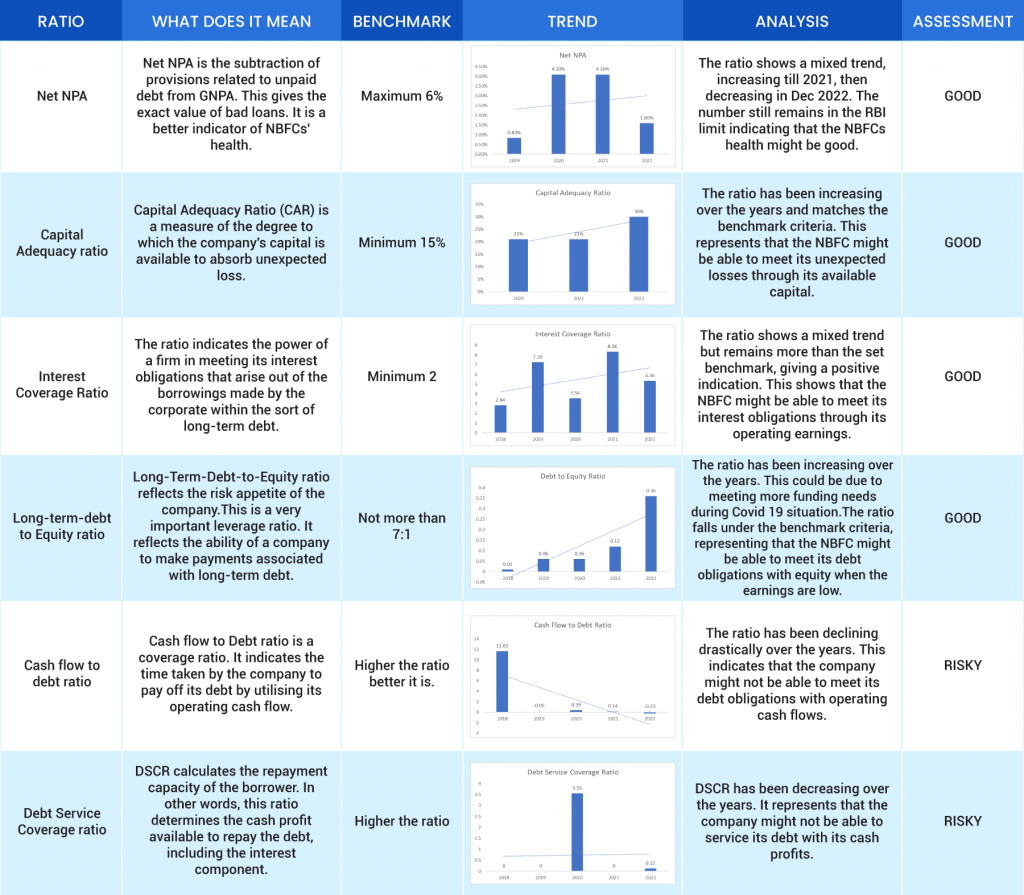

Ratio Analysis

Issue analysis

Pros

- Attractive Interest Rates

Offers interest rates ranging from 9% to 10.50%, with options for monthly, annual, and cumulative payouts—ideal for income-seeking investors. - Secured Instruments

The NCDs are secured by receivables and offer higher safety compared to unsecured products. - Listed on BSE/NSE

Enhances investor liquidity through secondary market trading. - Wide Tenor Options

Flexibility to invest across 24, 36, 60, and 120 months, catering to different investment horizons.

Cons

- Lower Credit Rating Compared to Peers

CRISIL has rated the NCDs ‘CRISIL A+/Stable’, which is investment grade but lower than AA or AAA offerings in the market. - Limited Upside from Group Synergies

Unlike larger diversified NBFCs, Edelweiss’ NCDs don’t provide exposure to high-growth lending segments like MSME or consumer durable loans. - Thin Trading Volumes

Historical NCD issues by EFSL have witnessed low liquidity on exchanges, possibly limiting exit options before maturity. - Volatility in Group Financial Performance

Despite improving risk profile, the group has gone through multiple restructuring phases, which may deter conservative investors.

Liquidity

- Cash and Liquid Investments stood at ₹1,355 crore as of March 31, 2025.

- Unutilized Bank Lines: ₹1,400 crore, offering an additional buffer.

- Debt Repayment Capacity: EFSL has adequate liquidity coverage for the next 12 months, supported by scheduled collections and refinancing plans.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Edelweiss Financial Services Limited

Edelweiss Financial Services Limited is one of India’s leading financial services conglomerates, offering a robust platform to a diversified client base across domestic and global geographies. The company has mainly four business verticals namely Retail Credit, Asset Management, Asset Reconstruction and Insurance services. Apart from that the company has also been providing Merchant Banking services since 1995. Edelweiss Financial Services Limited is listed on the stock exchange having a market capitalization of more than 6,000 Crores as of July,2024.

Strengths

- Diversified Business Mix

EFSL operates across retail credit (via ECL Finance and Nido Home Finance), wealth management, and asset reconstruction, reducing segment concentration risk. - Shift Toward Retail Lending

Retail loan book constitutes over 85% of total lending portfolio as of March 2025. This provides granularity and lowers concentration risk in large exposures. - Strong Capitalization

EFSL reported a Capital Adequacy Ratio (CAR) of 35.49% as of March 31, 2025, which is well above regulatory norms and reflects strong solvency buffer. - Robust Risk Management

The company has implemented structural risk containment by exiting wholesale lending and scaling secured retail loans like LAP and loans against securities

Weaknesses

- Modest Profitability

EFSL reported a net profit of ₹18 crore on a consolidated basis for FY2025, which is low relative to its scale, reflecting muted return ratios. - Legacy Asset Quality Risks

Despite derisking, the company still carries exposure to legacy wholesale loans, which may pose challenges in resolution and provisioning. - High Funding Cost Sensitivity

As a non-deposit taking NBFC, EFSL is heavily reliant on market borrowings, making it sensitive to interest rate cycles and credit spreads. - Complex Group Structure

Multiple group entities operating in ARC, wealth, and insurance businesses result in structural and regulatory complexity in consolidated management.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus June 26, 2025

Disclaimer- The information is published as on date 10/07/2025 based on information available on Prospectus June 26 , 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors