|

Getting your Trinity Audio player ready...

|

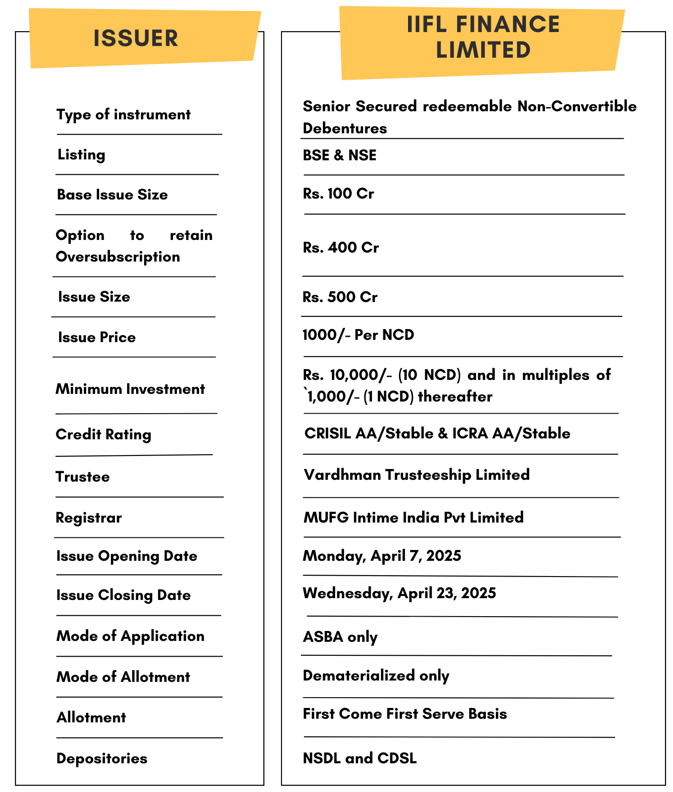

High Yield | AA/Stable Rated | Minimum Investment: 10k Only

Bond overview

IIFL Finance Limited is issuing the Non-Convertible Debentures. These NCDs are AA/Stable rated by CRISIL and ICRA. The NCDs are being issued in seven series: coupon ranges from 8.35% to 9% p.a. and different tenures of 24 months, 36 months and 60 months. The NCDs are secured and redeemable in nature.

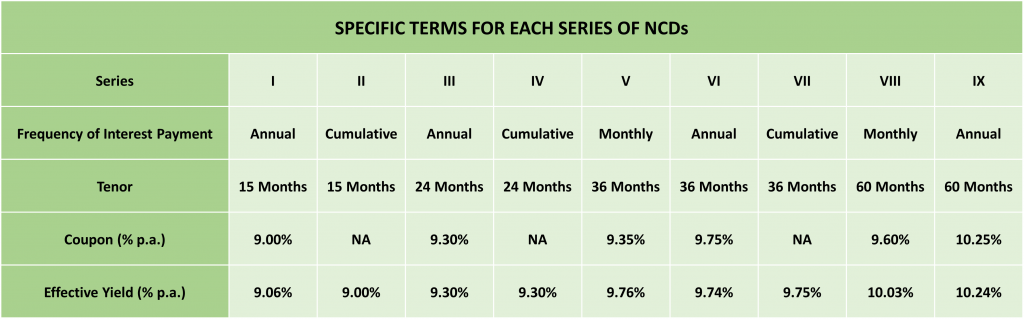

Coupon rates and effective yield for each of the series

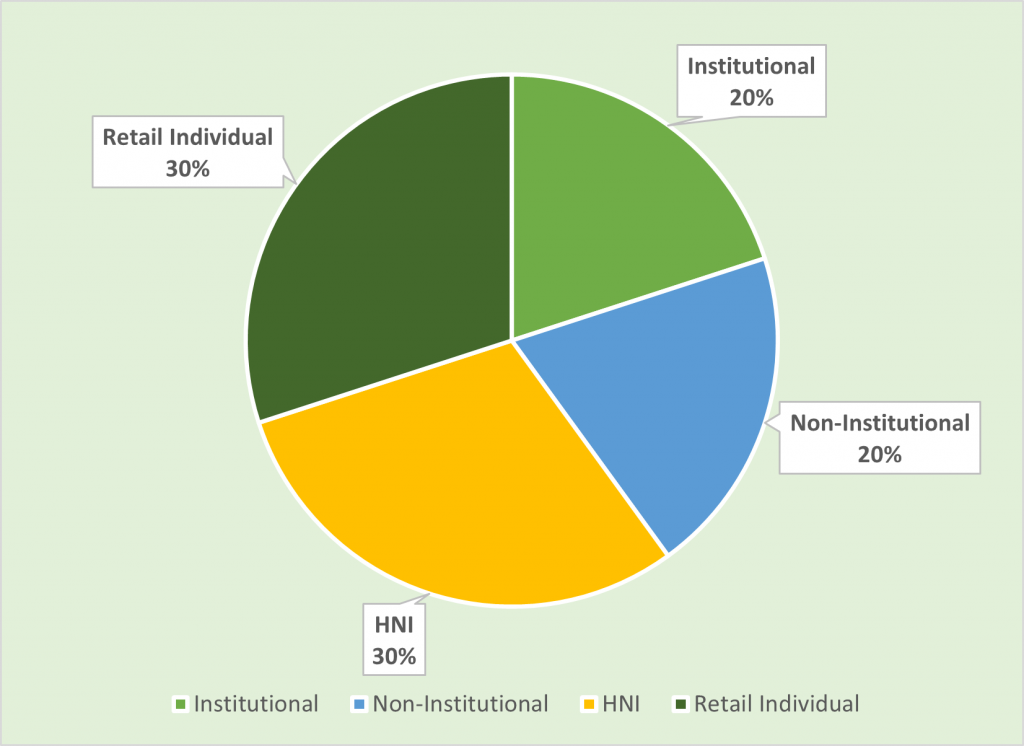

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for IIFL Finance Ltd NCD-IPO.

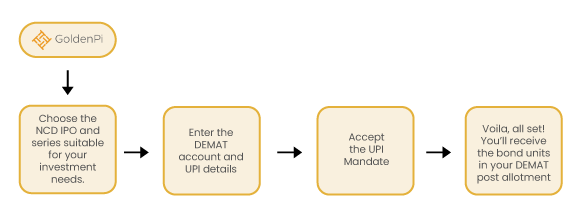

Investment Process for IIFL Finance Ltd. NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

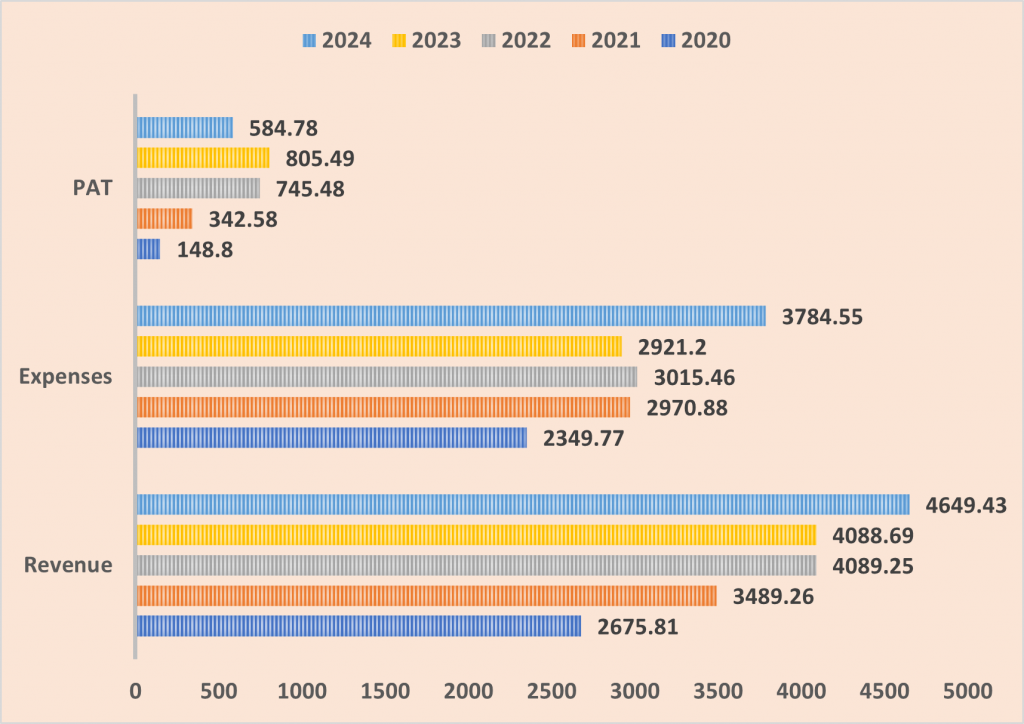

Financial Overview

Snapshot stating the Revenue, Expenses, PAT (In crores)

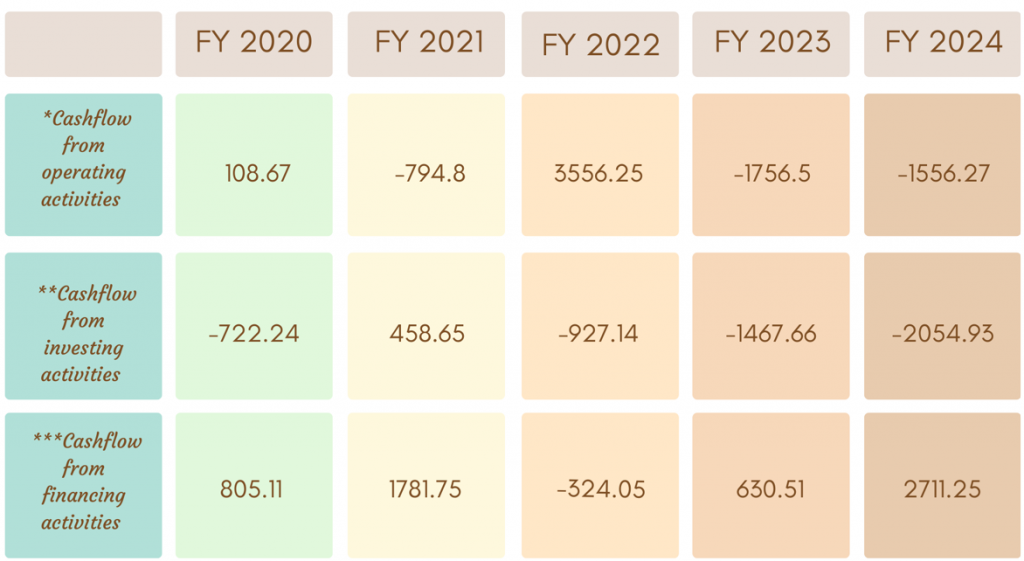

Cash flow for last 5 years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

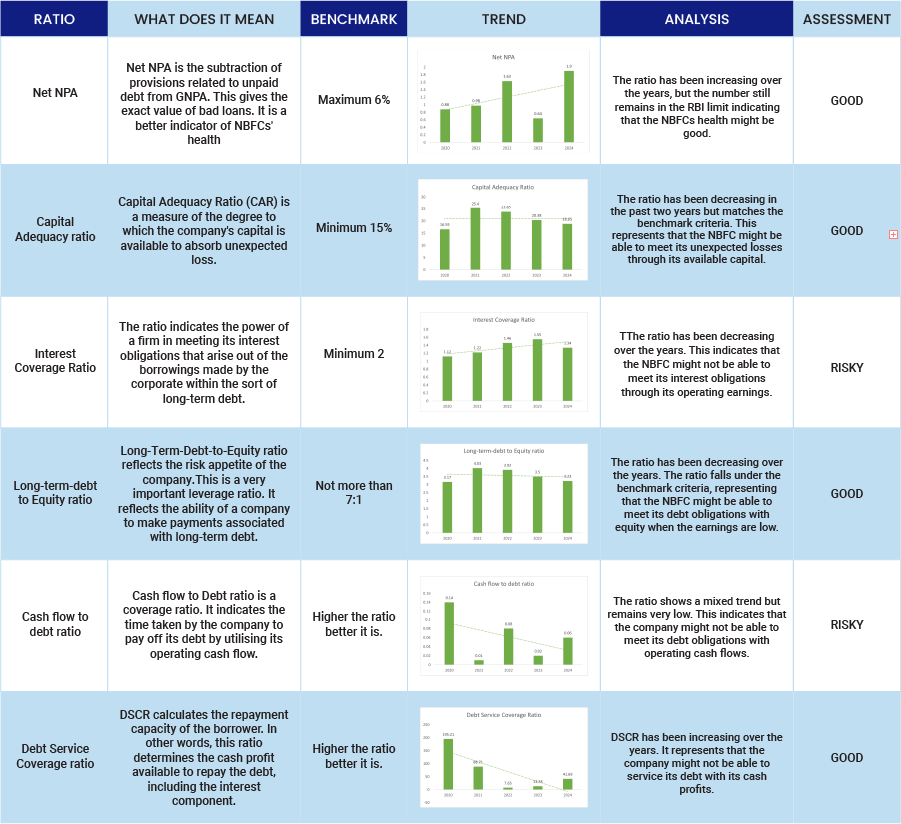

Ratio Analysis

Issue analysis

Pros

- Attractive Coupon: Offers interest rates up to 10.5% p.a., higher than most bank FDs and many NCDs in the market.

- High Credit Rating: Rated CRISIL AA/Stable, ICRA AA (Stable), and CARE AA/Stable, indicating strong creditworthiness.

- Strong Consolidated Financials: FY24 revenue of ₹9,429 crore, with a net profit of ₹1,692 crore, reflecting healthy business performance.

- Diverse Product Mix: Exposure to secured products like gold loans, mortgage loans, and MSME lending strengthens asset quality.

- Extensive Reach: Operates in 27 states with over 4,400 branches, enabling strong customer acquisition and loan growth.

Cons

- Exposure to Retail & MSME Risk: While diversified, 74% of the loan book is retail, and 22% is MSME—segments vulnerable to economic shocks.

- Moderate Capitalization: Capital adequacy ratio (CAR) at 20.6% as of Dec 2023, adequate but not industry-leading.

- Secured NCDs, Not Guaranteed: While backed by company assets, repayment still depends on IIFL’s financial discipline.

- Taxable Returns: Interest earned is fully taxable as per investor’s income slab, reducing post-tax yield for higher income groups.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About IIFL Finance Ltd.

IIFL Finance Limited is one of India’s leading non-banking financial companies (NBFCs), established in 1995, with over 25 years of operational track record. Headquartered in Mumbai, the company offers a diversified portfolio that includes gold loans, business loans, personal loans, housing loans, and microfinance.

As of FY24, IIFL Finance operates through a vast network of 3,700+ branches across 25+ states, and serves over 80 lakh customers, supported by a workforce of more than 30,000 employees.

The company is part of the IIFL Group, known for its presence across wealth management, securities, and financial services. Listed on NSE and BSE, IIFL Finance had a consolidated loan book of ₹71,468 crore and reported a PAT of ₹1,607 crore in FY24.

Backed by marquee investors like Fairfax Group and CDC Group, IIFL Finance combines a strong digital backbone with physical presence, offering competitive, last-mile credit access across India’s urban and semi-urban markets.

Strengths

- Comfortable Capitalisation: The group maintains a robust capital structure, supporting its growth and operational stability.

- Established Track Record: IIFL Finance has a proven history in the home loans and microfinance sectors, indicating strong market presence and operational expertise.

- Sustained Profitability with Stable Asset Quality: The company has consistently reported healthy profitability metrics, underpinned by stable asset quality.

Weaknesses

- Limited Resource Profile Diversity: The group’s funding sources are not as diversified as some peers, leading to a moderately higher cost of funds.

- Regulatory Impact on Gold Loan Business: A prior embargo by the Reserve Bank of India (RBI) on the gold loan segment led to a reduction in the gold loan portfolio to approximately ₹10,797 crore as of September 30, 2024, down from ₹23,354 crore on March 31, 2024. Although the embargo was lifted on September 19, 2024, the time required to regain market share and profitability in this segment remains a consideration.

Invest in Bond IPO online in just 5 minutes

Source- Tranche 1 Prospectus March 29, 2025

Disclaimer- The information is published as on date 04/08/2025 based on information available on Tranche 1 Prospectus March 29, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors