")

High Yield | A-/Stable Rated | Minimum Investment: 10k Only

Bond overview

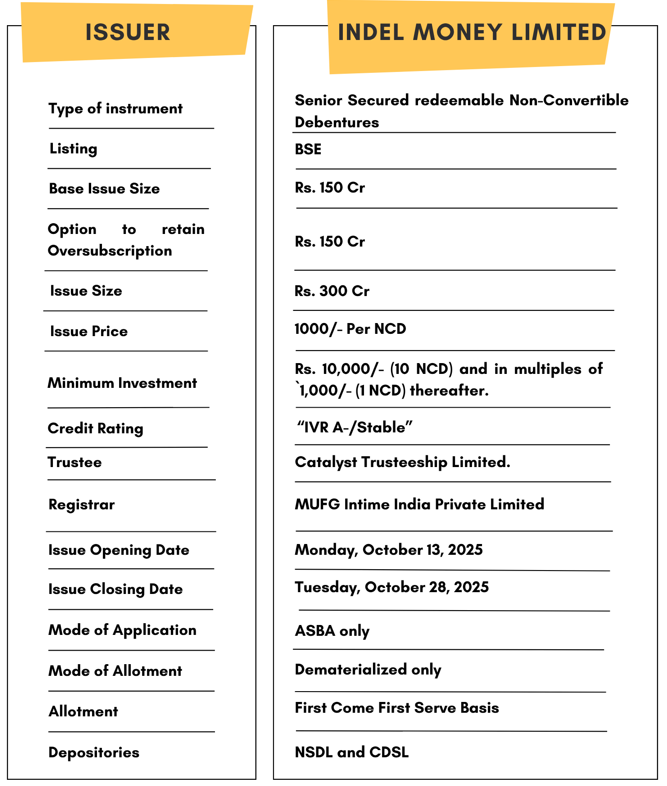

Indel Money Limited is issuing the Non-Convertible Debentures. These NCDs are A-/Stable rated by Infomerics Valuation and Rating Limited. The NCDs are being issued in seven series: coupon ranges from 9% to 11.25% p.a. and different tenures of 366 days, 24 months, 36 months, 60 months and 72 months . The NCDs are secured and redeemable in nature.

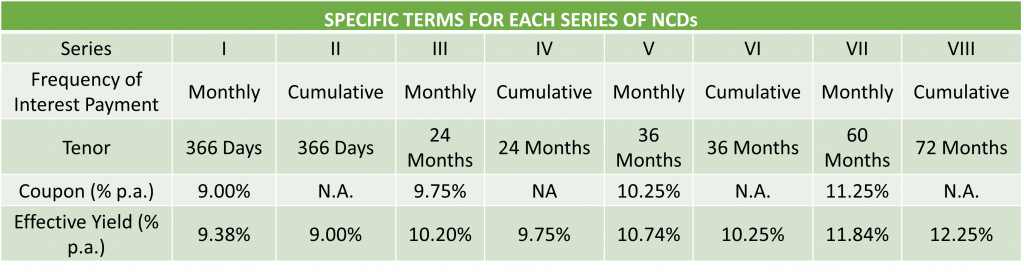

Coupon rates and effective yield for each of the series

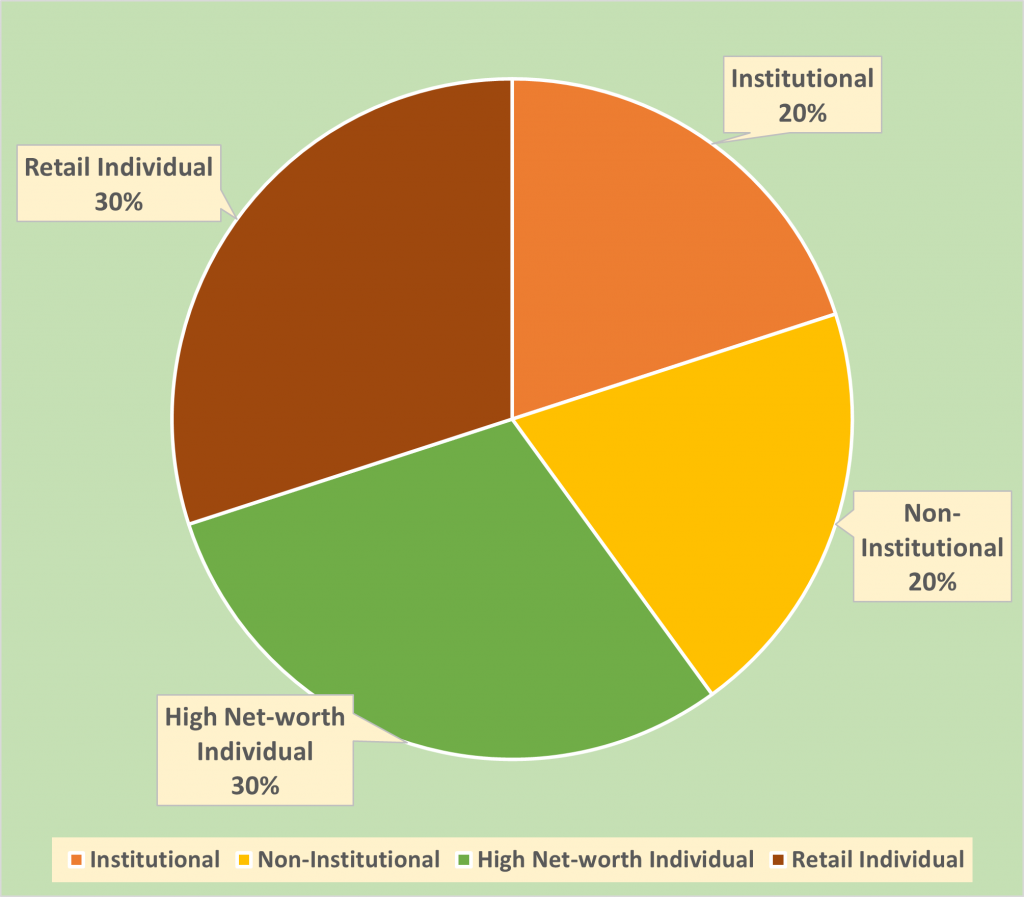

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Indel Money Limited NCD-IPO.

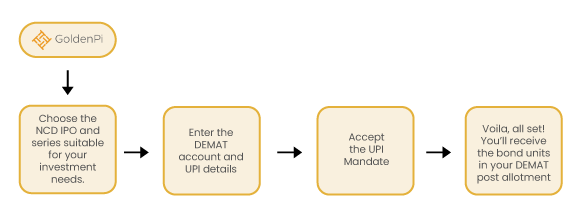

Investment Process for Indel Money Limited NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

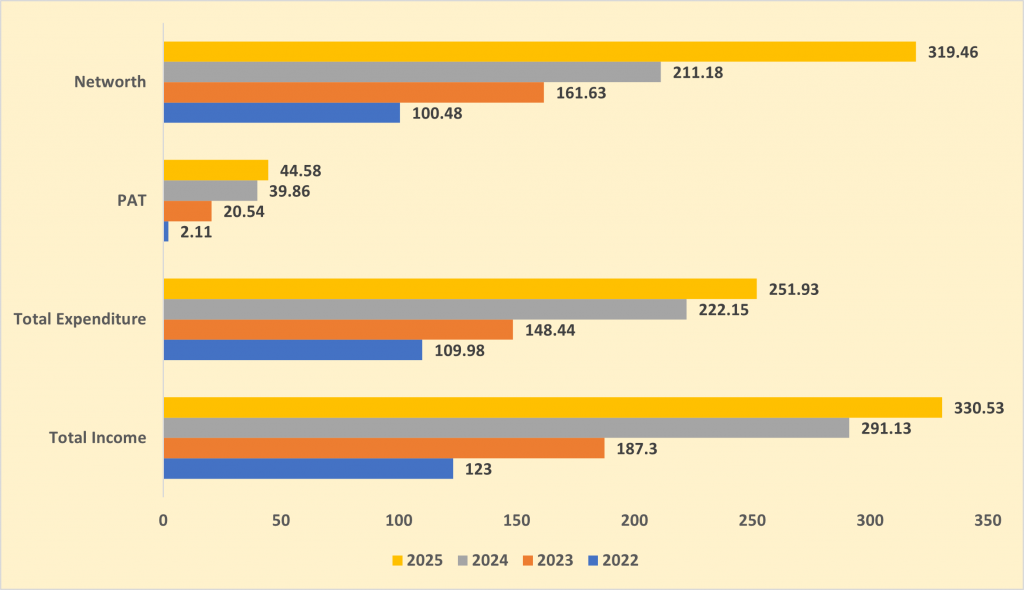

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

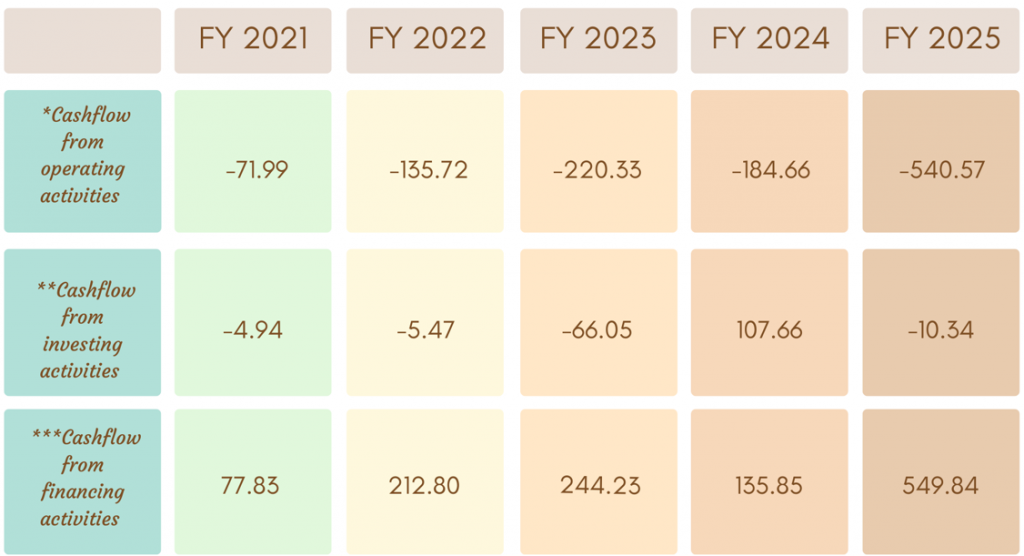

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

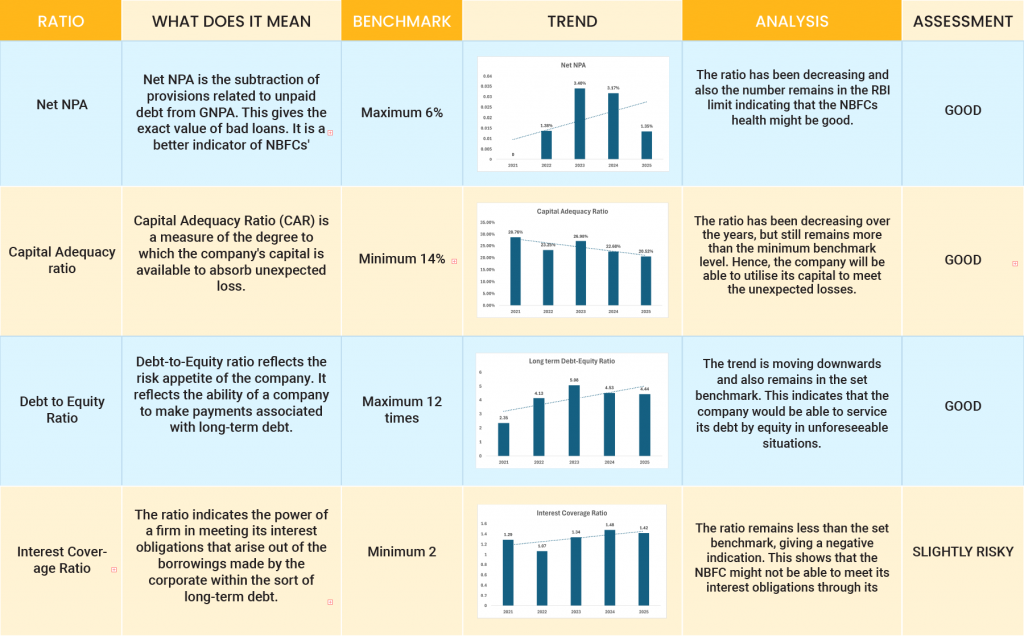

Ratio Analysis

Issue analysis

Pros

- Secured paper: First-ranking pari-passu charge on current assets with minimum 1.00x security cover; listed on BSE for liquidity.

- Rated issue: IVR A-/Stable (Infomerics) — indicates moderate degree of safety; regular public NCD track record (multiple prior public issues).

- Attractive yield choices: Tenors 366d/24/36/60/72 months with effective yields up to ~12.25% (series-wise options).

- Sized for scale: ₹150 cr base + ₹150 cr green-shoe (₹300 cr overall) supports growth and market depth.

Cons

- Security cover cushion: Minimum 1.00x asset cover (pari-passu on current assets) offers limited extra cushion vs. some peers with higher covers.

- Sector & ALM sensitivity: NBFC funding/ALM, cost-of-funds cycles, and portfolio performance are ongoing risks; issue is not underwritten.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Indel Money Limited

Indel Money Limited, established in 1986 and rebranded in 2013, is a non-deposit-taking NBFC primarily focused on gold loan financing. Acquired by its current promoters in 2012, the company has expanded its offerings to include business loans, loans against property, and vehicle loans. With a strong management team led by industry veterans and consistent capital infusion, Indel Money has demonstrated solid asset quality and a growing asset base, reaching ₹1,788 crore in assets under management as of June 2024. The company has maintained a CRISIL BBB+/Stable rating, reflecting its financial stability and robust growth

Q1 FY26

Strengths

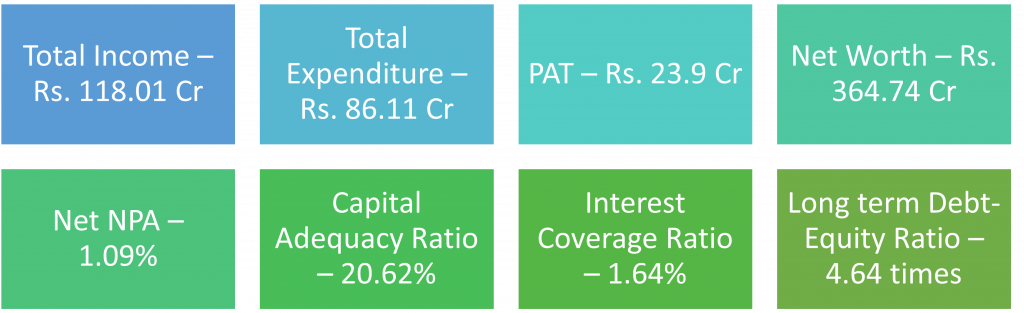

- Strong capitalisation (ongoing promoter support): Net worth ₹364.7 Cr (Jun 30, 2025) vs ₹319.5 Cr (Mar 31, 2025); promoter infusion ₹100 Cr in FY25 (₹37.04 Cr bonus + ₹62.96 Cr equity) and ₹21.85 Cr in Q1 FY26; plan to infuse ~₹80 Cr in FY26. Gearing at 4.64x (Q1 FY26) vs 4.44x (FY25), expected to improve with profits.

- Experienced leadership & governance depth: Chairman Mr. Mohanan Gopalakrishnan (38+ yrs banking); CEO Mr. Umesh Mohanan (20+ yrs financial services); 9-member Board with 4 independent directors, each 30+ yrs sector experience.

- High growth AUM trajectory: AUM ₹2,334.4 Cr (FY25) from ₹1,533.8 Cr (FY24) and ₹1,153.9 Cr (FY23) — 52.2% 3-yr CAGR; continued to ₹2,544.1 Cr in Q1 FY26.

- Focused, resilient portfolio mix: ~93% gold loans; ~7% business/MSME & digital personal loans — maintaining core specialization while testing adjacencies.

- Rising income, healthy margins: Net Interest Income up from ₹100.3 Cr (FY23) to ₹174.4 Cr (FY25); ₹62.7 Cr in Q1 FY26. NIM 9.02% (FY25) vs 12.59% (FY24) amid higher CoF/competition; 10.26% in Q1 FY26, indicating recovery.

- Diversified funding & improving CoF: Average borrowing cost 12.25% (Q1 FY26) vs 12.50% (FY25) with scope to decline. Borrowing mix: Capital markets ~42%, Co-lending ~26%, Banks ~19%, Direct assignment ~14% — supporting timely, scalable funding.

- Regulatory permissions for optionality: Holds RBI AD-II license (forex business nascent) — potential future fee income/adjacency without current P&L dependence.

- Positive outlook on capital & leverage: Regular equity infusions + profitability expected to strengthen net worth and reduce gearing from FY26 onward.

Weakness

- Asset quality only average (though improving): GNPA 1.61% & NNPA 1.09% (Q1 FY26) — better than 1.88%/1.35% (FY25) and 4.98%/3.17% (FY24), but still not best-in-class.

- Product concentration: ~93% of AUM in gold loans; resilience hinges on gold prices/auction outcomes despite ~96% of AUM being secured.

- Geographic concentration: Despite 369 branches across 14 states/UTs, ~65% of AUM is concentrated in five southern states (KA, TN, AP, TG, KL), exposing the book to regional shocks.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus September 29, 2025

Disclaimer- The information is published as on date 08/10/2025 based on information available on Prospectus September 29, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors