|

Getting your Trinity Audio player ready...

|

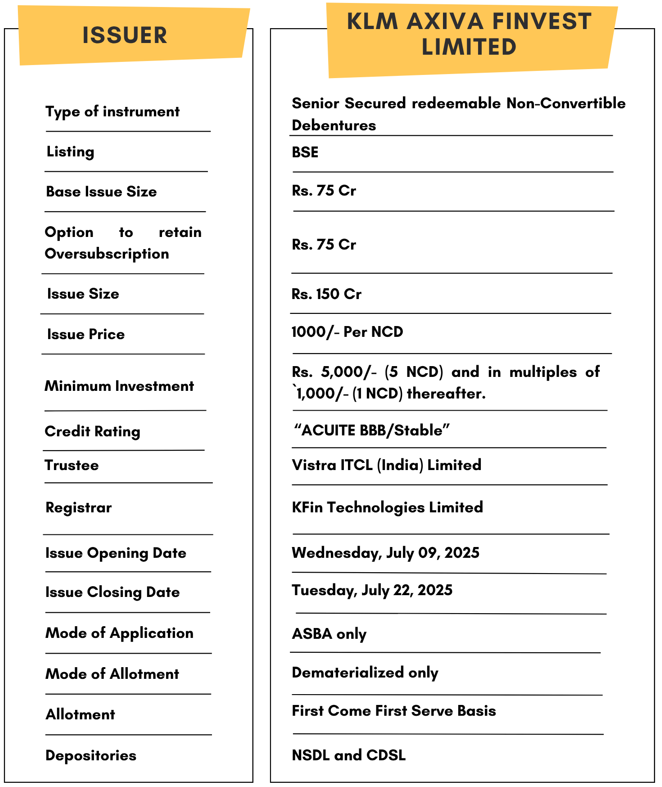

High Yield | ACUITE BBB/Stable Rated | Minimum Investment: 5k Only

Bond overview

KLM Axiva Finvest Limited is issuing the Non-Convertible Debentures. These NCDs are BBB rated with stable outlook by Acuite Ratings. The NCDs are being issued in ten series: coupon ranges from 9.5% to 11% p.a. and different tenures of 400 days, 16 months, 18 months, 2 years, 3 years, 5 years, and 79 months. The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series

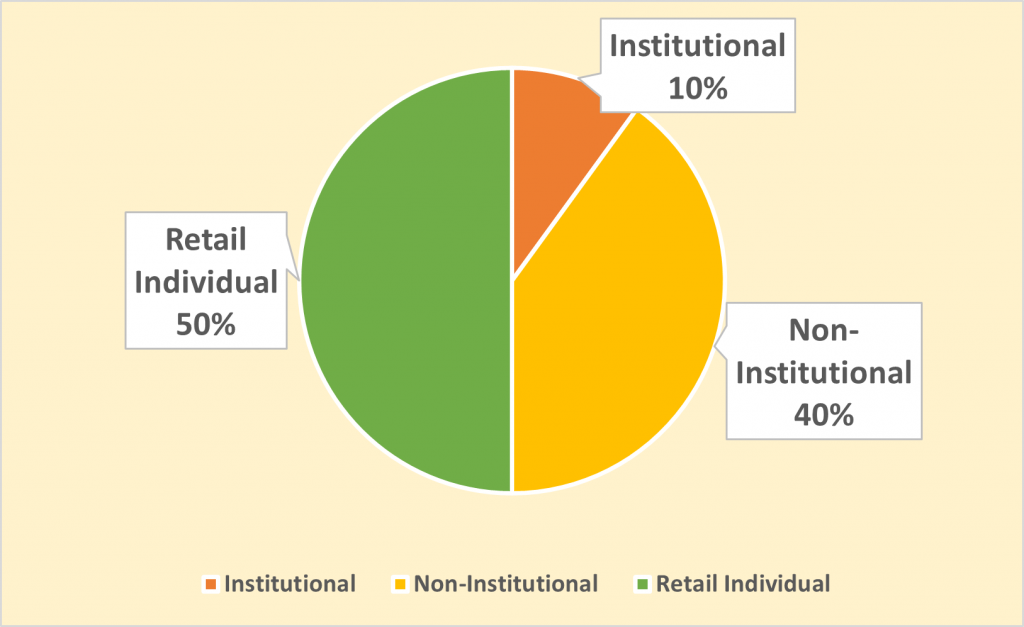

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for KLM Axiva Finvest NCD-IPO.

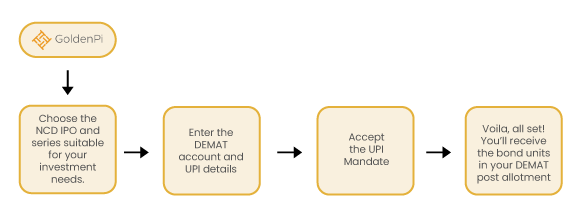

Investment Process for KLM Axiva Finvest NCD IPO

You can invest in IPOs via GoldenPi in 3 easy steps.

Issue analysis

Pros

- High Yield Options

Coupon rates range up to 11.5% p.a., higher than most secured NCDs in the market — especially attractive in a falling interest rate environment. - Secured NCDs

The instruments are secured by loan receivables, giving investors a senior charge on underlying assets. - Tenor Flexibility

Investors can choose from multiple tenure options: 400 days, 18, 24, 36, 60, and 75 months — suiting both short- and long-term income seekers. - Listed on BSE

Offers liquidity through market trading (though actual trading volume may be limited).

Cons

- Lower Credit Rating

Rated ‘Acuité BBB/Stable’, indicating moderate credit risk. This is investment grade, but lower compared to top-rated NBFCs . - Limited Liquidity in Secondary Market

Historical KLM NCDs have shown low trading volumes, making premature exits harder. - Narrow Geographic & Product Focus

Heavy reliance on gold loan segment and southern India limits resilience to sectoral or regional disruptions. - Smaller NBFC Size

Investors may perceive higher default or downgrade risk due to lower institutional strength and scalability.

Liquidity Position

- Cash & Bank Balances stood at ₹47.65 crore as of March 31, 2025 .

- Working Capital Facilities: Out of ₹520 crore sanctioned, average utilization remained at 60–65%, leaving a buffer for short-term obligations.

- Liquidity is adequate to cover upcoming 6–12 months debt maturities, aided by steady monthly collections from gold loans.

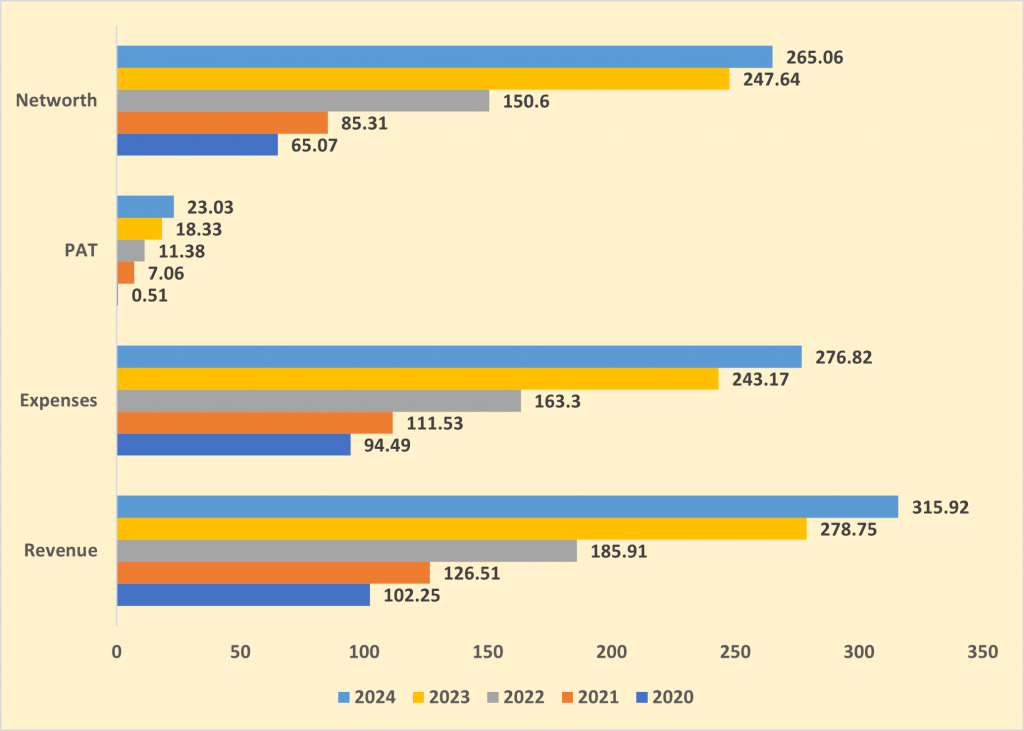

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

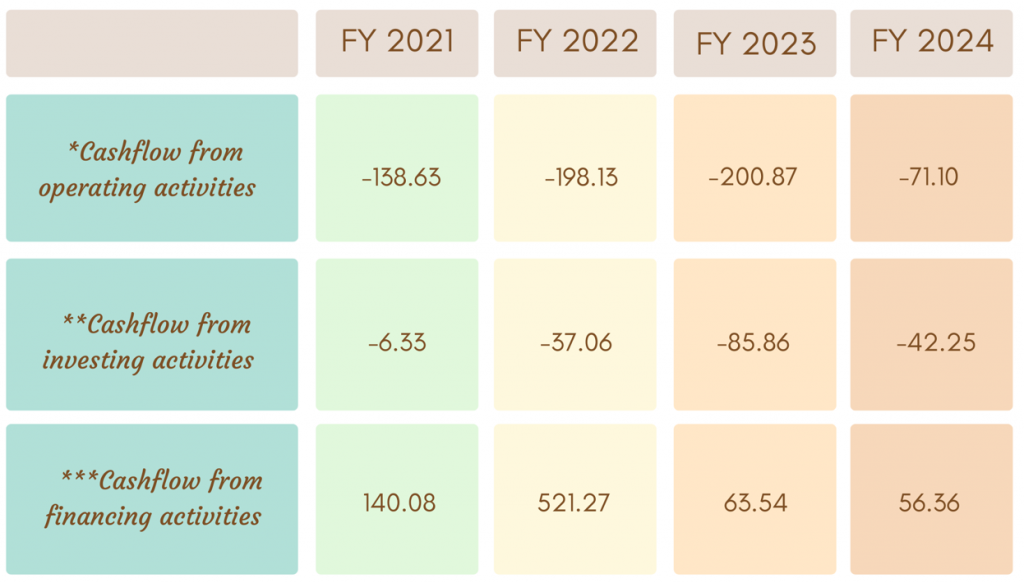

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

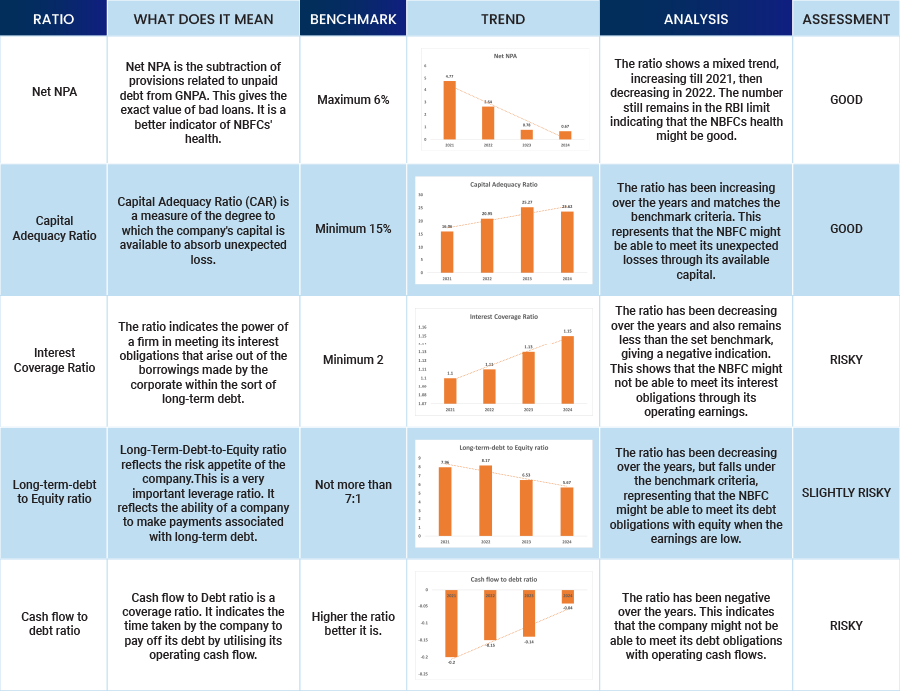

Ratio Analysis

To get better returns than Bank FDs, invest in NCD-IPOs online.

About KLM Axiva Finvest Limited

KLM Axiva Finvest is a Kerala based non-deposit taking systemically important NBFC ( Middle Layer ) registered with RBI. Since Incorporation in 1997, the company has been serving Low and middle income individuals and businesses that have limited or no access to formal credit facilities and finance channels. KLM operates in four business verticals mainly- Gold loan and household jewelry loans, MSME Loans, Personal Loans and Microfinance Loans. Apart from that the company also provides Money transfer facility, Insurance and Forex related services to their customers. Mr Manoj Ravi is serving the position of Chief Executive Officer in the company.

Here is a table below illustrating the % of interest income generated by the company across its business segments.

| Business Verticals | FY-2023 | FY-2024 |

| Gold Loans | 64.60% | 69.81% |

| MSME Loans | 20.38% | 16.85% |

| Microfinance Loans | 12.04% | 9.19% |

| Personal Loans | 2.98% | 4.15% |

| Total | 100% | 100% |

Approximately 70% of the business of the company is generated through Gold loans and household jewelry Loans.

Strengths

- Rapid AUM Growth

The company’s Assets Under Management (AUM) rose to ₹1,985 crore as of March 31, 2025, from ₹1,670 crore in FY23, showing robust business expansion.

- Strong Regional Presence

KLM operates 600+ branches across 5 states, enabling access to rural and semi-urban segments, especially in South India.

- Improving Profitability

Net profit increased to ₹22.38 crore in FY2025, up from ₹14.42 crore in FY23 — a 55% growth, indicating improved operational efficiency .

- High Capital Adequacy

CRAR stood at 17.71% in FY2025, comfortably above the minimum regulatory requirement, providing a cushion for growth and risk coverage .

Weakness

- Concentration Risk

Gold loans continue to dominate, forming 98% of the total loan book, limiting diversification across other asset classes. - Regional Risk Exposure

With 100% branch presence in South India, KLM is exposed to geographic concentration risks, including region-specific regulatory, economic, or climatic risks. - Moderate Asset Quality

Gross NPA ratio increased slightly to 1.88% in FY25 (from 1.85% in FY23), requiring tighter credit oversight and provisioning. - Smaller NBFC by Scale

Compared to large peers, KLM operates on a modest scale with moderate brand visibility outside its primary regions.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus July 04, 2025

Disclaimer- The information is published as on date 07/10/2025 based on information available on Prospectus July 04, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors