|

Getting your Trinity Audio player ready...

|

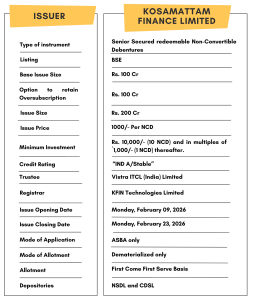

High Yield | IND A/Stable Rated | Minimum Investment: 10K Only

Bond overview:

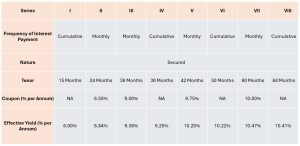

Kosamattam Finance Limited is issuing the Non-Convertible Debentures. These NCDs are A/Stable by India Ratings & Research. The NCDs are being issued in eight series: yield ranges from 8.00% to 10.47% p.a. and different tenures of 15 months, 24 months, 36 months, 42 months, 50 months, 60 months and 84 months. The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series:

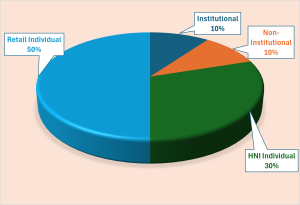

Allocation Ratio:

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Kosamattam Finance Ltd NCD-IPO.

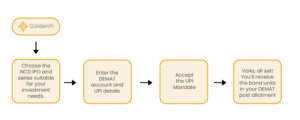

Investment Process for Kosamattam Finance Ltd NCD IPO:

You can invest in IPOs via GoldenPi in 3 easy steps.

Financial Overview:

Snapshot stating the Total Income, Expenses, Net Worth and PAT ( In Crores):

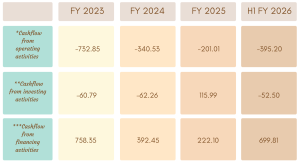

Cash flow for last few years ( In Crores):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

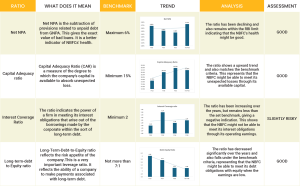

Ratio Analysis:

Issue analysis:

Pros:

- Strong Credit Rating: Rated IND A/Stable indicating high degree of safety and low credit risk.

- Secured NCDs: Senior, secured NCDs backed by First-ranking pari-passu charge by way of hypothecation of loan receivables

- Security Cover: The security cover required must be a minimum of 110% of the total of the outstanding principal balance of the NCDs

- Competitive yields: up to 10.47% vs bank FDs.

- Wide tenor and payout options: monthly to cumulative

Cons:

- Geographic concentration: ~97% AUM from South India (Tamil Nadu ~59% in FY25), exposing business to regional economic & political risks.

- Exposure to Gold Loan Volatility: A large portion (approx 99%) of business still depends on gold loan pricing and demand cycles.

- Interest Rate Risk: More pronounced in longer tenors (60-84 months).

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Kosamattam Finance Limited:

Kosamattam Finance Limited (KFL) is an RBI-registered NBFC primarily engaged in the gold loan business, lending against the pledge of household gold jewellery. The company is headquartered in Kottayam, Kerala, and has a long operating history in the gold loan segment. In addition to gold loans, Kosamattam Finance offers ancillary and fee-based services, including microfinance, money transfer services, foreign currency exchange, power generation, agriculture-related activities, and air ticketing services. However, revenues continue to be predominantly driven by the gold loan business, which contributed ~96% of total income in recent periods.

Kosamattam Finance operates a wide branch network of 981 branches as of Dec ‘2025, spread across Kerala, Tamil Nadu, Karnataka, Andhra Pradesh, Maharashtra, Uttar Pradesh, Telangana, and the Union Territories of Puducherry and Delhi. The company employs nearly 3,924 personnel to support its business operations, with a strong concentration in southern India.

The company is part of the Kosamattam Group, originally founded by Nasrani Varkey, and is currently led by Mathew K. Cherian, Chairman and MD, a fourth-generation entrepreneur. Under his leadership, the group has scaled its gold loan operations while maintaining a focused product strategy.

Highlights:

11.6+ Lakh Customers

175+ Years of Trust

981 Branches

3900+ Employees

Key Highlights:

Strengths:

- Strong Promoter Group: Kosamattam Finance Ltd. (KFL) is part of the Kosamattam Group, which has a 175+ year legacy, founded by Mr. Chacko Varkey. Mr. Mathew K. Cherian, a fourth-generation family member, serves as Chairman and MD. The strong 86.17% promoter and promoter group equity stake reflects a significant, long-term commitment to the business.

- Experienced management team: Led by Promoter & Director Mathew K. Cherian (40+ years in finance), supported by a stable senior management team (majority with 5+ years’ tenure), bringing deep expertise in gold lending and a strong understanding of rural and semi-urban customers.

- Growing AUM base along with Improving operational efficiency :Over 30 years in gold-loan business with steady expansion; KFL has demonstrated consistent growth in its gold loan AssetsThe gold loan AUM reached ₹6100 Cr. in Sept ‘2025, an increase from ₹5680 Cr in Mar’FY25 and ₹5310 Cr in FY24. This growth is supported by efficient operations, as indicated by a stable AUM per branch of ₹6.28 Cr. (up from ₹5.85 Cr. in Mar’2025 and ₹5.38 Cr. Mar’2024).

- Predominantly secured retail portfolio: ~100% of the Assets Under Management (AUM) are secured, with 99.07% backed by gold jewellery and the remaining 0.88% by mortgages (home loans and Loan Against Property or LAP), ensuring strong collateral cover and high recoverability.

- Granularity of loans: The company’s lending model is centered on low-risk, small-ticket retail loans, with an average loan amount of Rs. 50-55K and shorter tenures (9-12 months). This structure makes it less susceptible to interest rate fluctuations.

- Consistent Growth in Gold loan AUM: The company’s customer base, evidenced by its Gold Loan portfolio, has consistently expanded. Gold Loans remain dominant, comprising 98.68% (Mar’2023), 98.92% (Mar’2024), 99.07% (Mar’2025), and 99.21% (Sept’2025) of the total loan portfolio. Gold Loan accounts also grew significantly, from 8.82 lakh in March 2023 to 11.61 lakh by Sept’2025.

- Stable asset quality: GNPAs are stable at 1.75% in Sept’ 25 (Mar’25: 1.37%; Mar ’24: 1.44%), supported by regulatory LTV caps (75%) and timely gold auctions. In Mar’ 25, KFL auctioned gold worth ₹63.7 Cr. with no losses, fully recovering dues, resulting in modest and low-volatility credit costs.

- Diversified funding profile: Funding is well diversified, with access to a wide network of PSU/Private banks and NBFCs (including SBI, Bank of Baroda, Union Bank, HDFC Bank, Axis Bank, Kotak Mahindra Bank, Federal Bank, Bajaj Finance, TATA Capital among others), alongside capital market instruments (NCDs,Subdebt, CP), supporting funding stability and refinancing flexibility.

- Healthy capitalisation: Capital remains comfortable, supported by a ₹50 Cr. rights issue in FY24, lifting Tier I capital to 17.64% in Q2 FY26 (FY25: 17.39%; FY24: 16%), with moderate leverage of 4.9x.

- Stable and consistent profitability: KFL has demonstrated steady profitability, with PAT increasing to ₹127 Cr. in FY25 (FY24: ₹113.6 Cr; FY23: ₹107.1 Cr; FY22: ₹800 Cr.) and ROA sustained around 2.06% (FY24), 2% (FY23), 2.15% (FY22) . In Q2 FY26, PAT stood at ₹48.2 Cr with a healthy annualised ROA of 2.9% supported by a stable cost of borrowings (~10.4%), controlled opex (~3% of AUM), technology-led operating efficiency, rising AUM per branch, and minimal credit costs (0.02%) due to the secured gold loan portfolio.

- Adequate liquidity position: Positive ALM in all buckets up to 1 year, supported by short asset tenor (9–12 months) vs longer liabilities (~36 months) and liquid collateral.

Weaknesses:

- Product concentration risk: ~99% portfolio in gold loans, making earnings heavily dependent on gold-loan segment performance & gold price cycles.

- Geographic concentration: ~97% AUM from South India (Tamil Nadu ~59% in FY25), exposing business to regional economic & political risks.

Invest in Bond IPO online in just 5 minutes