")

|

Getting your Trinity Audio player ready...

|

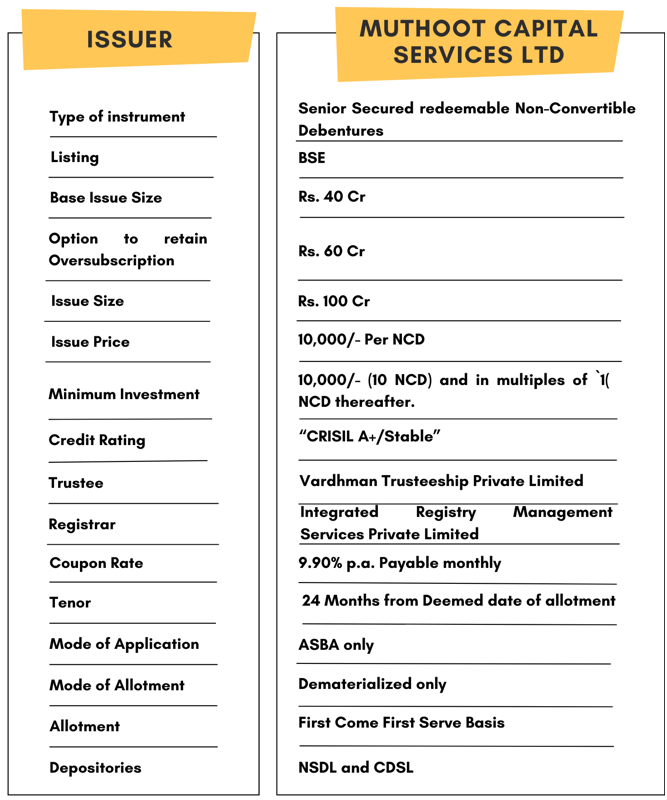

High Yield | A+/Stable Rated | Minimum Investment: 10,000

YIELD UPTO 10.80%

Muthoot Capital Services Ltd is issuing Non-Convertible Debentures (NCDs) rated A+/Stable by CRISIL. These debentures are offering a coupon rate of 9.90% per annum with monthly interest payment. The tenure for these NCDs is 24 months. The NCDs are secured and redeemable in nature.

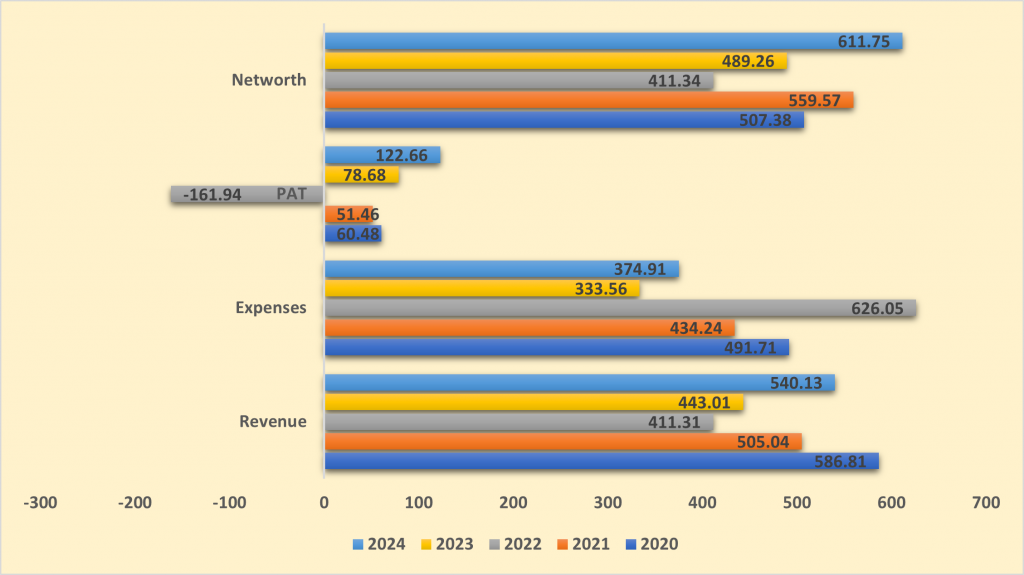

Financial Overview

Snapshot stating the Revenue, Expenses, PAT (In crores)

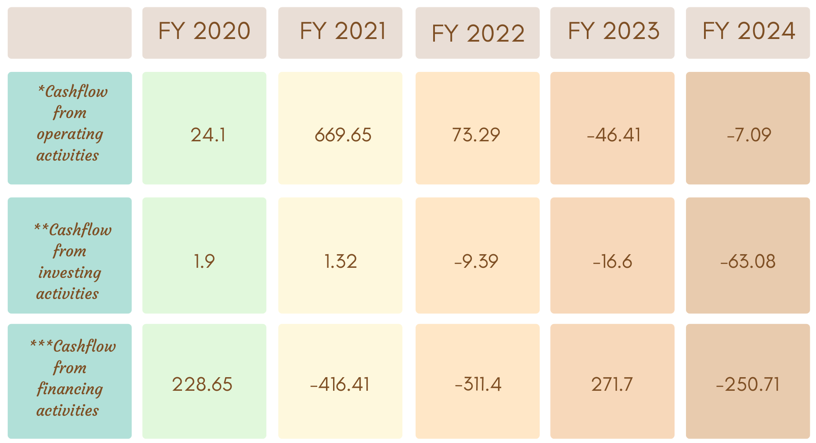

Cash flow for last 5 years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

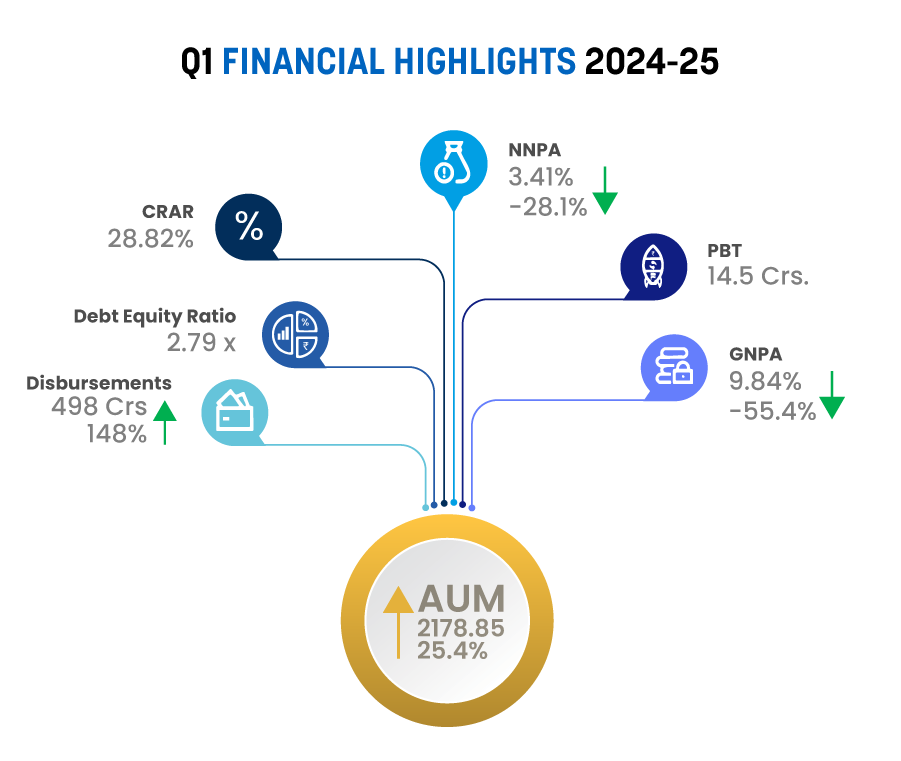

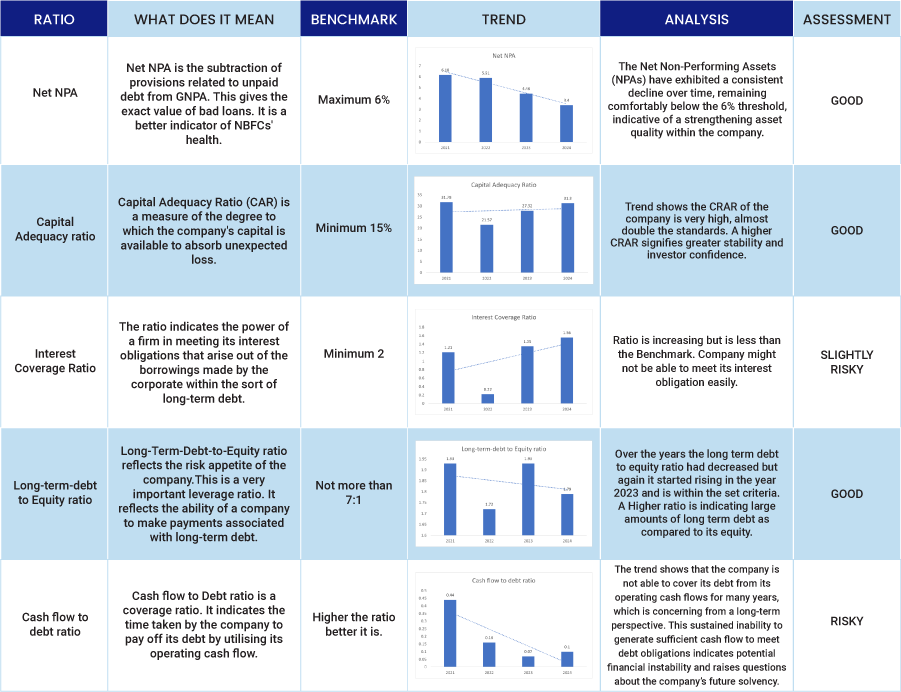

Ratio Analysis

Issue analysis

Pros

- The NCD is A+ rated security with a stable outlook.

- The yield offered is 9.90% which is much higher than FDs.

- Adding NCDs to a portfolio can enhance diversification, reducing overall portfolio risk by including fixed-income securities.

- It is a better opportunity to invest in fixed income securities for the short term, earning monthly interest.

- The company is actively borrowing money with over 1600 crore Rupees raised in FY 2024.

Cons

- The operations of the NBFC is geographically constrained. It is majorly operated in South India.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Muthoot Capital Services Ltd.

Muthoot Capital Services Ltd, backed by the Muthoot Pappachan Group, is a publicly listed Non-Banking Finance Company (NBFC) registered with the Reserve Bank of India. Founded in 1994, it stands out as one of India’s most progressive automobile finance companies. The company provides both fund-based and non-fund-based financial services to retail, corporate, and institutional clients. Their product portfolio includes two-wheeler loans, used car loans, and fixed deposit investment products. Mr. Ramandeep Singh Gill serves as the Chief Financial Officer for the company.

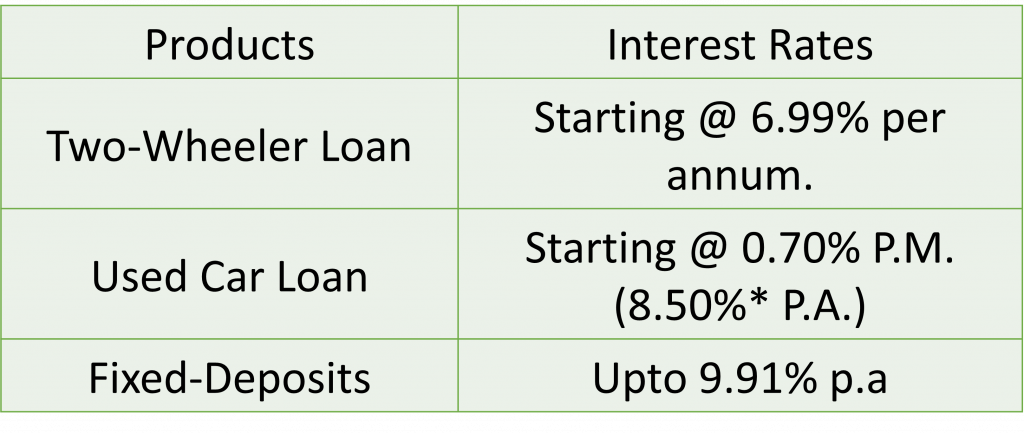

Here is a table showing their products and interest rates.

In addition, Muthoot offers secured business loans and loyalty loans to its existing customers at attractive rates.

Liquidity

MCSL has a strong liquidity position, with positive asset-liability management (ALM) across all buckets up to one year as of July 2024. It holds ₹365.34 crore in cash and equivalents against obligations of ₹255.6 crore over the next two months, resulting in a liquidity coverage of 1.4x. This assumes no collections, indicating a stable short-term liquidity. The company anticipates rolling over its credit lines and can rely on support from MPG if needed.

Strengths

- Support from Muthoot Pappachan Group (MPG):

Muthoot Capital Services Ltd. (MCSL) benefits significantly from MPG’s financial and operational backing, leveraging MPG’s network and access to Muthoot Fincorp Ltd (MFL) branches and clients, aiding in loan book expansion. - Adequate Capitalization:

MCSL’s net worth improved to ₹622.9 crore as of June 2024, up from ₹489 crore in March 2023. The gearing ratio also strengthened, moving from 3.9x to 2.8x, showcasing strong capital adequacy, with a target to keep it below 5x.

- Operational Efficiency and Collection Performance:

Initiatives in collection mechanisms have reduced 90+ days past due (DPD) from 16.4% in March 2023 to 9.3% by June 2024. Gross NPAs also improved, decreasing to 10.2% from 20.6% in FY23, and collection efficiency has consistently been above 99%. - Strong Promoter Expertise:

With over 30 years in the lending industry, the promoters’ experience is pivotal in scaling operations, supported by a seasoned management team, ensuring robust governance. - Strategic Partnerships in Co-Lending:

Collaborations with WheelsEMI, Manba Finance, Up Money, EV.fin, and Credit Wise Capital enhance customer reach in the two-wheeler financing sector, aligning well with MCSL’s growth strategy. - Exemplary Co-Lending Record:

In co-lending, MCSL has maintained a zero Non-Performing Assets (NPA) record, showcasing effective risk management and high asset quality in this segment.

Weaknesses

- High Borrowing Costs:

MCSL’s borrowing cost is relatively high at 9.8%, impacting profitability. - Asset Quality Still Recovering:

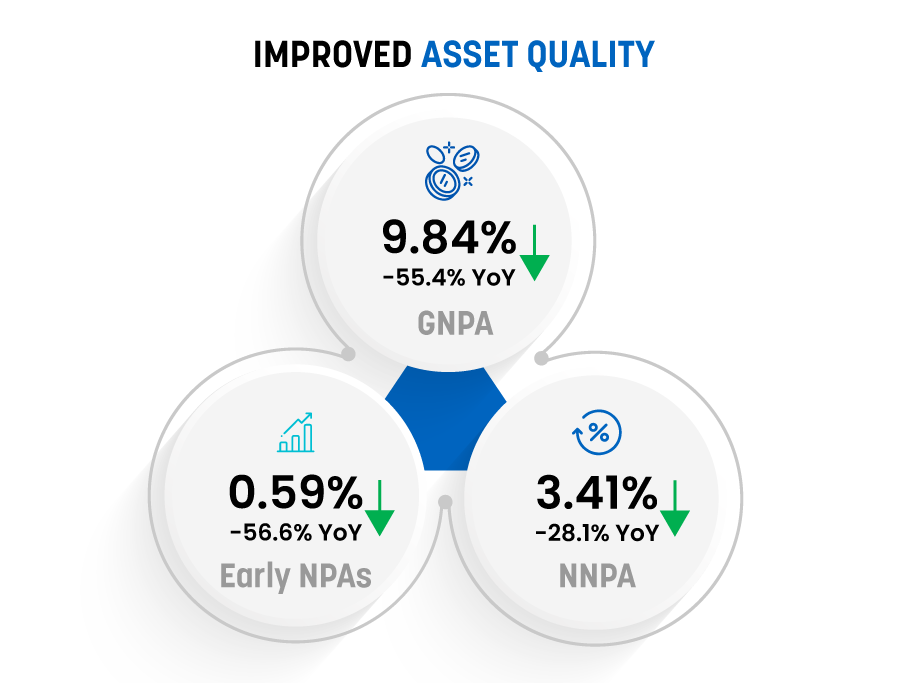

Despite improvement, asset quality remains modest, with a Gross NPA of 9.84% as of June 2024. COVID-19 impacted collections and increased provisioning, and while GNPAs have declined, collections from delinquent buckets are a continued risk. - Moderate Earnings Profile:

Earnings show improvement, but profitability is still recovering. FY24 PAT was ₹123 crore, with a RoMA of 3.4%. In Q1 FY25, PAT was ₹11.4 crore, with an annualized RoMA of 1.8%, indicating further potential for growth. - Geographical Concentration:

The portfolio is concentrated in southern India, with 60% of loans as of June 2024, creating exposure to regional market risks. Although expanding in the north and east, high regional concentration remains a vulnerability.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus October 23, 2024

Disclaimer – The information is published as on date 04/03/2024 based on information available on Prospectus October 23, 2024. The information may be subject to change in case of change in terms of prospectus or any other reason as the case may bemaybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors