|

Getting your Trinity Audio player ready...

|

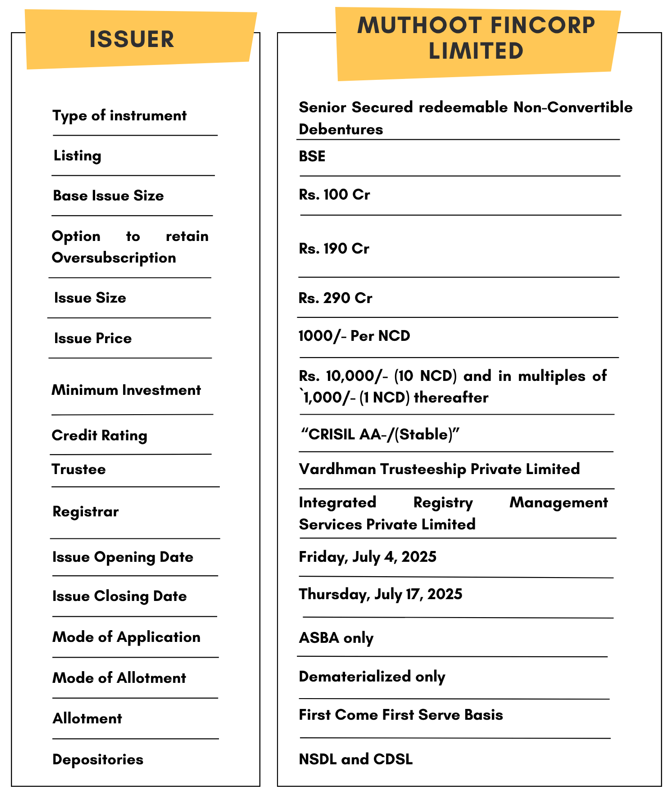

High Yield | AA-/Stable Rated | Minimum Investment: 10k Only

Muthoot Fincorp Ltd is issuing Non-Convertible Debentures. These NCDs are AA-/Stable by CRISIL. The NCDs are being issued in twelve series: yield ranges from 9.20% to 9.81% p.a. and different tenures of 24 months, 36 months, 60 months, and 72 months. The NCDs are secured and redeemable in nature.

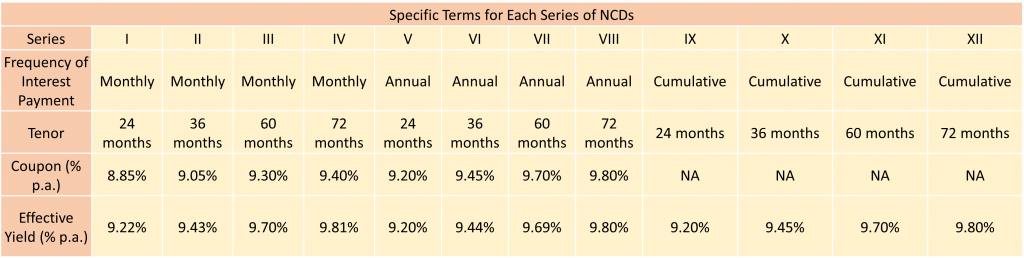

Muthoot Fincorp Ltd NCD IPO: Coupon rates and effective yield for each of the series

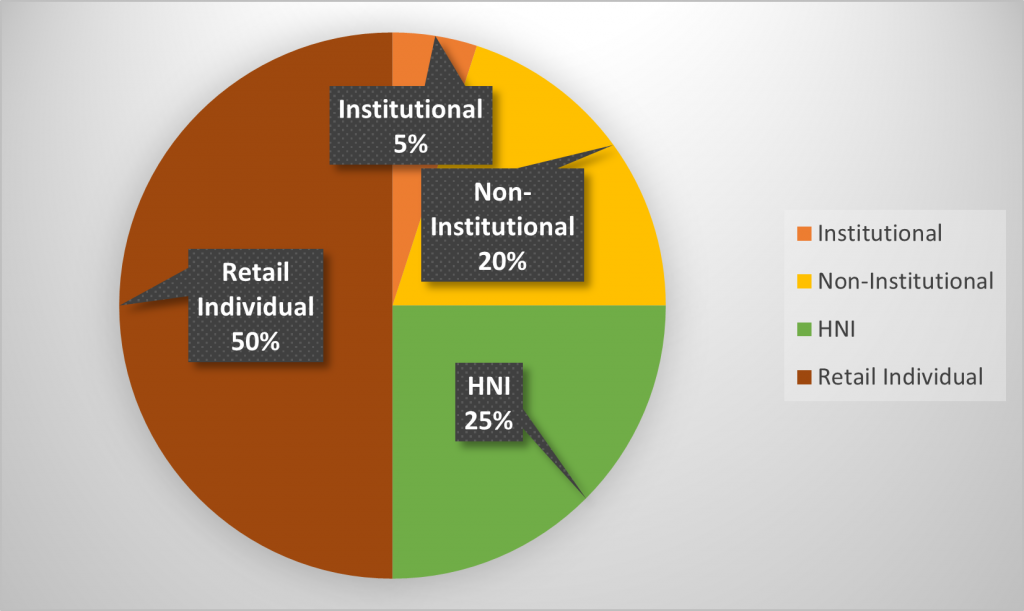

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Muthoot Fincorp Ltd NCD-IPO.

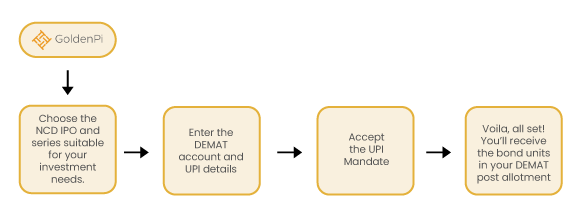

Investment Process for Muthoot Fincorp Ltd NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

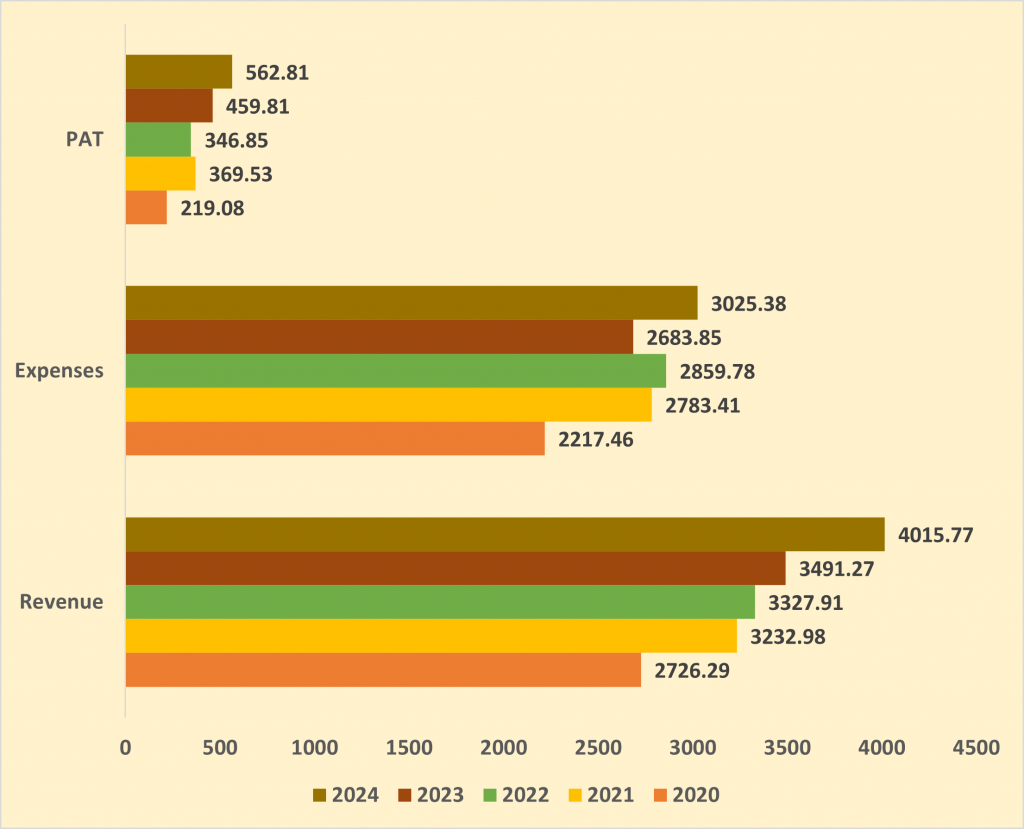

Financial Overview

Snapshot stating the Revenue, Expenses, EBIT, Net Worth and P AT

(Amount in Rs. Cr)

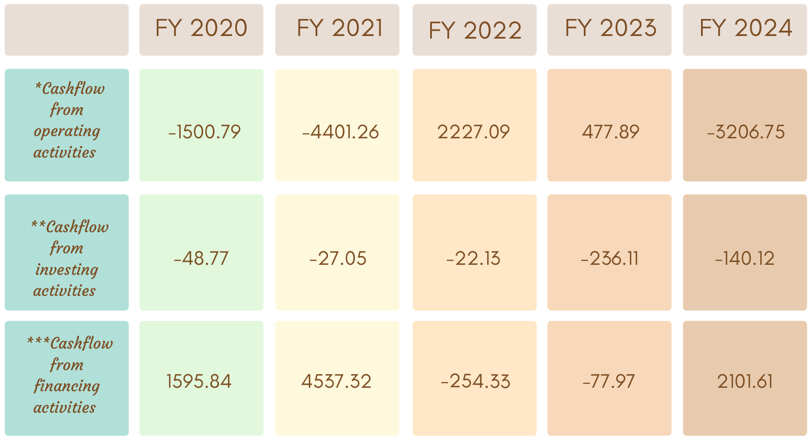

Cash flow for last 5 years

(Amount in Rs. Cr)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

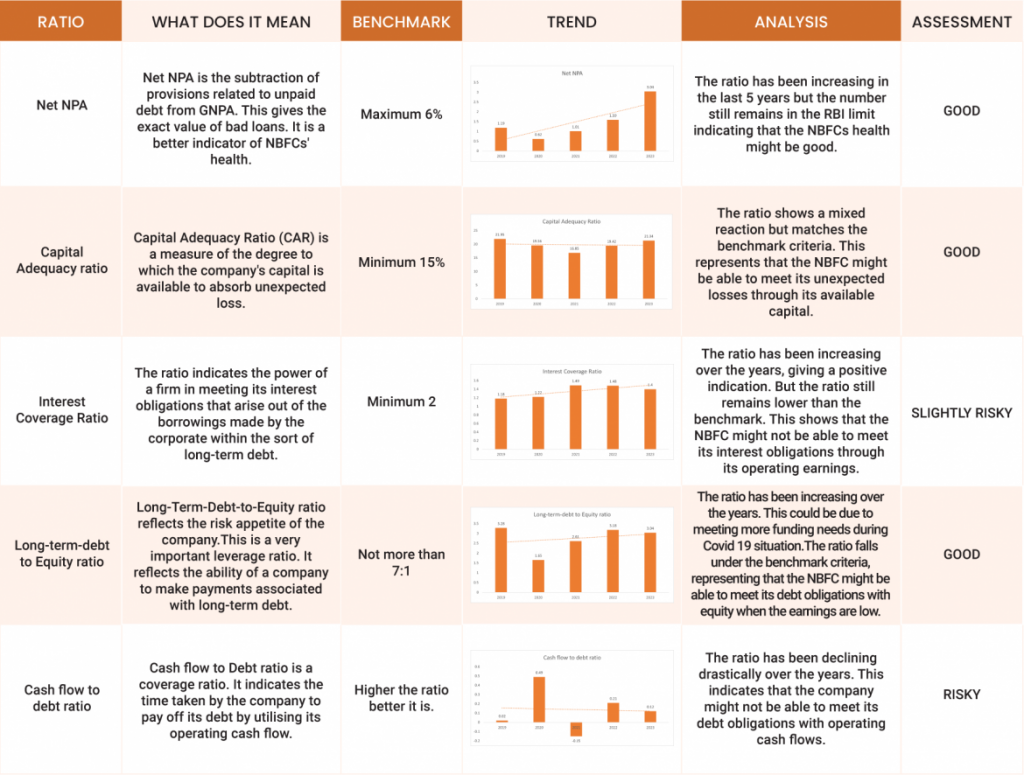

Ratio Analysis

Issue analysis

Pros

- Strong Credit Rating: Rated CRISIL AA-/Stable, indicating high degree of safety and low credit risk.

- Diversified NBFC: Operates across gold loans, MSME financing, and two-wheeler loans, reducing reliance on a single segment.

- Robust Parentage: Part of the Muthoot Pappachan Group, a well-established financial services conglomerate.

- Extensive Reach: Over 3,600 branches across India ensures strong customer base and rural presence.

- Secured NCDs: Backed by a subservient charge on loan receivables and current assets, offering security to debenture holders.

Cons

- Exposure to Gold Loan Volatility: A large portion of business still depends on gold loan pricing and demand cycles.

- Asset Quality Pressure: Any adverse movement in collateral value (especially gold) could impact collections.

- Interest Rate Risk: High interest rate environment could affect borrowing costs and NIM (Net Interest Margin).

- Moderate Capitalisation: While comfortable, the capital adequacy ratio (CAR) needs constant monitoring as business scales.

Liquidity Position

- Strong buffer: Standalone liquidity ₹5,106 cr as of Feb 28, 2025 (~5–8% of balance sheet); liquidity cover 1.5× over next two months without roll‑overs.

- Access to funding: ₹20,700 cr bank limits and ₹2,000 cr commercial paper line; since Oct 2024, raised ~₹16,047 cr at competitive rates .

To get better returns than Bank FDs, invest in NCD-IPOs online.

About MFL

Founded in 1997, Muthoot Fincorp Ltd.(MFL) is a non-deposit taking, one of the leading NBFCs in the country. The NBFC primarily deals into lending against gold jewelry. It is the flagship company of the Muthoot Pappachan Group also popularly known as the Muthoot Blue Group, which has diverse business interests such as hospitality, real estate, and power generation.

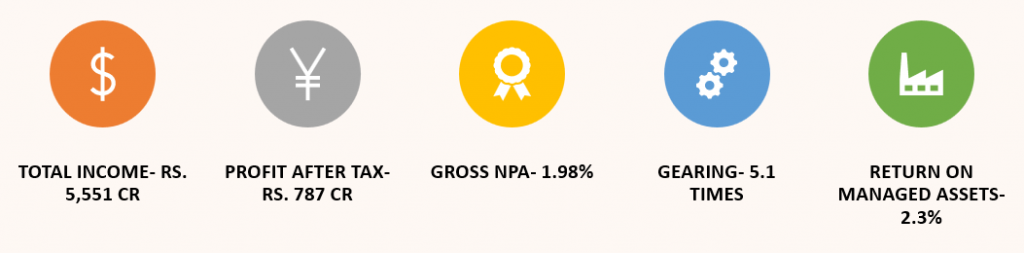

FY25

Strengths

- Strong market leadership & AUM: Gold-loan AUM stood at ₹28,509 cr (55 % of group total), including ₹6,424 cr co‑lending as of March 31, 2025; non-gold AUM spans ₹12,356 cr MFI, ₹3,058 cr vehicle, ₹2,557 cr housing.

- Robust asset quality: Steady gold loan performance and controlled GNPA (~3–4% across segments), demonstrating resilience.

- Solid capitalisation: Net worth grew from ₹6,570 cr in FY24 to ₹7,432 cr in FY25, with consolidated gearing at 5.2×. Standalone, gearing ~2.7× and consolidated net worth ~₹27,916 cr as of Dec 31, 2024.

- Profitable operations: Strong interest margins with return on managed assets (RoMA) of ~5.1% in FY24, ~4.8% in 9M FY25; credit costs contained.

- Parent & group support: Backed by experienced promoters; microfinance IPO (₹760 cr new equity + ₹200 cr offer for sale) boosted capital in Dec 2023.

Weaknesses

- Geographic concentration: Gold-loan book heavily regional; potential underwriting variability across regions.

- Regulatory uncertainty: RBI’s draft directions on gold loans (April 9, 2025) may affect practices and margins.

- Elevated delinquencies in non-gold segment: Microfinance GNPA rose from 2.3% (Mar 2024) to 4.8% (Mar 2025); 90+ days overdue at 5.7%.

- Profit pressure in MFI: Muthoot Microfin reported net loss ₹222 cr in FY25, RoMA negative at –1.6% vs +3.7% in FY24; credit cost surged to 5.6%, operating cost ~5.5%.

Invest in Bond IPO online in just 5 minutes

Source- Tranche VI Prospectus June 27, 2025

Disclaimer- The information is published as on date 7/03/2025 based on information available on Tranche VI Prospectus June 27, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors