|

Getting your Trinity Audio player ready...

|

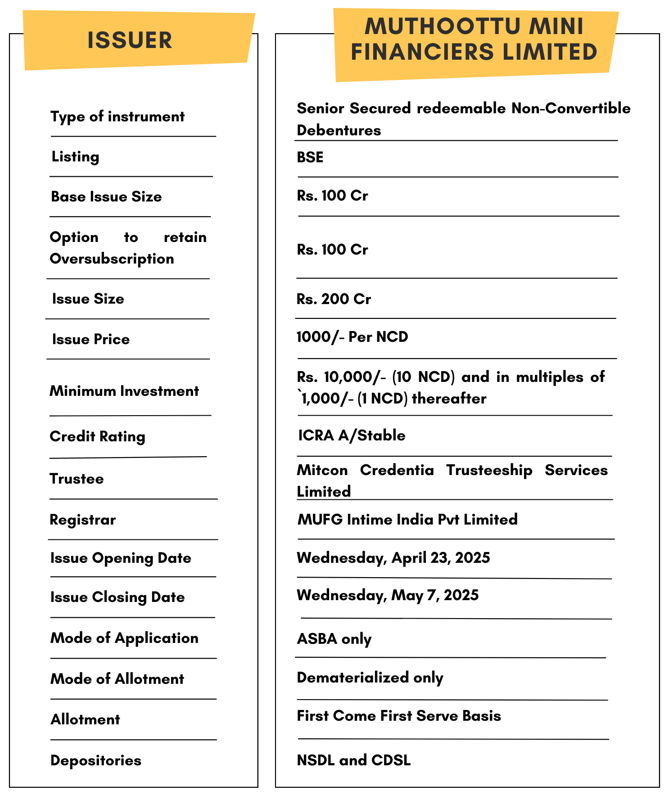

High Yield | A/Stable Rated | Minimum Investment: 10k Only

Muthoottu Mini Financiers Ltd is issuing Non-Convertible Debentures. These NCDs are A/Stable by ICRA. The NCDs are being issued in six series: yield ranges from 9.26% to 11.02% p.a. and different tenures of 18 months, 24 months, 36 months, 48 months and 60 months. The NCDs are secured and redeemable in nature.

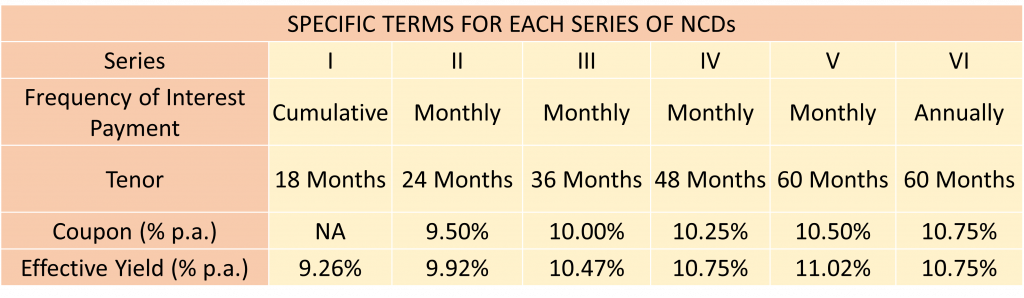

Muthoottu Mini Financiers Limited NCD IPO: Coupon rates and effective yield for each of the series

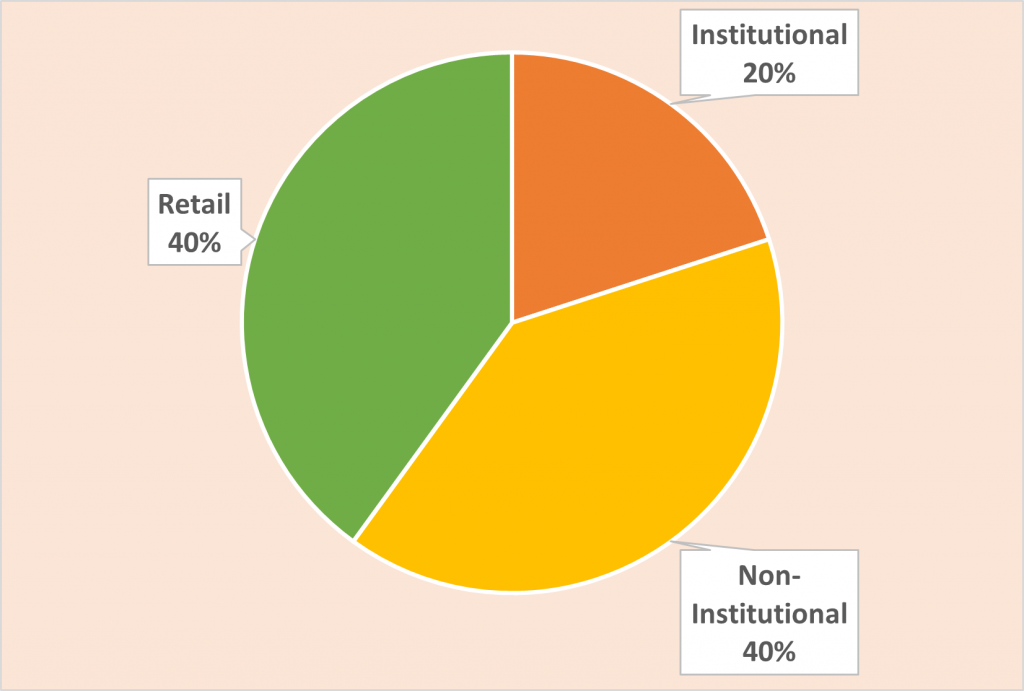

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Muthoottu Mini Financiers Ltd NCD-IPO.

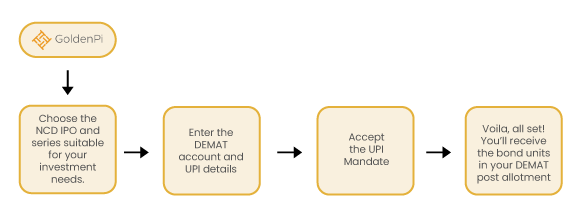

Investment Process for Muthoottu Mini Financiers Ltd NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

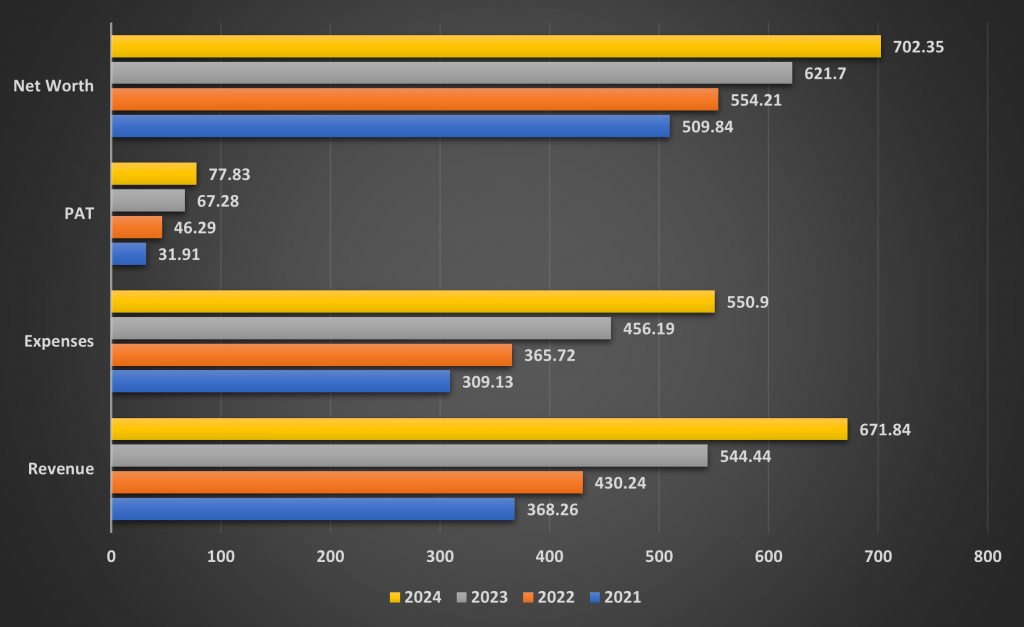

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT

(Amount in Rs. Cr)

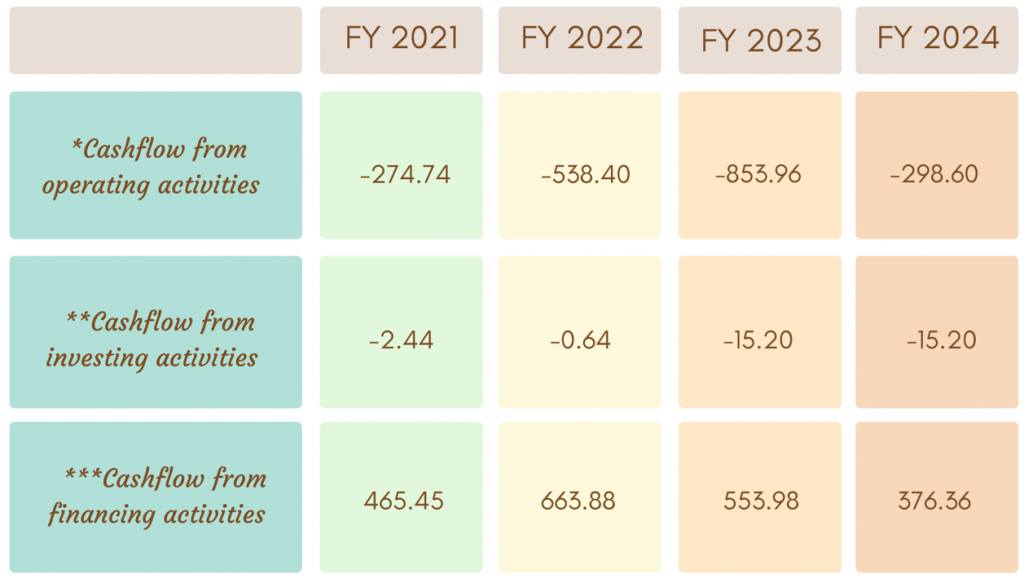

Cash flow for last 5 years

(Amount in Rs. Cr)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

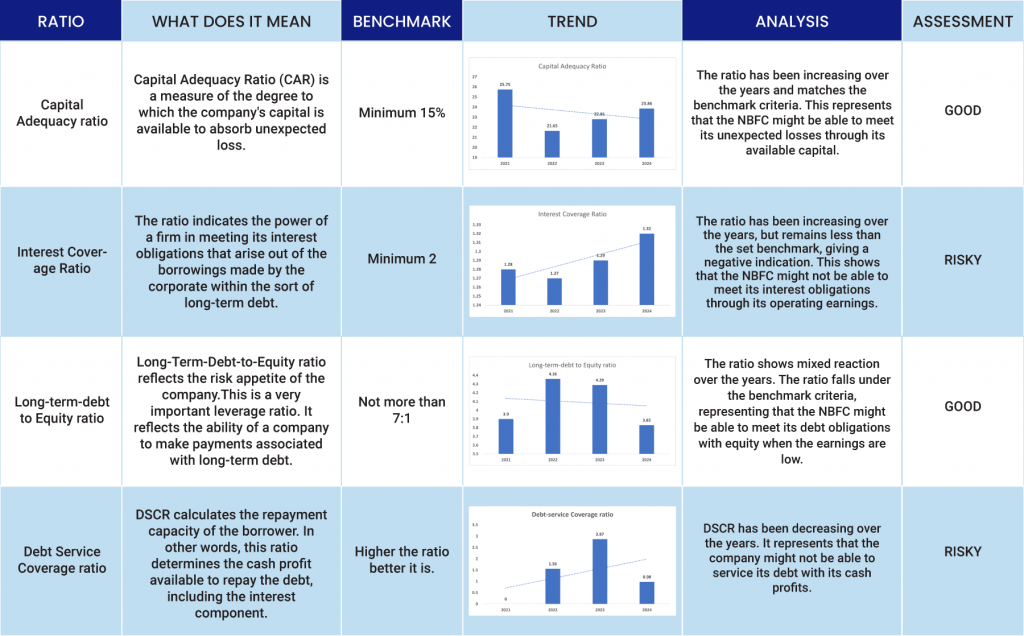

Ratio Analysis

Issue analysis

Pros

Attractive Coupon Rate:

- Offers competitive interest rates with various tenors (details in Series structure), making it appealing for fixed-income investors.

Reasonable Credit Rating:

- Rated [ICRA] A (Stable) as of March 27, 2025 – indicating adequate degree of safety for timely servicing of financial obligations.

Strong Regional Presence:

- MMFL has a well-established footprint in South India with a long track record in the gold loan segment.

Secured Issuance:

- The NCDs are secured by a first charge on current assets including receivables, ensuring 100% security cover.

Repeat Issuer with Track Record:

- This is the 19th public issue, demonstrating consistent access to debt capital markets.

Cons

Concentration in Gold Loans:

- MMFL’s business is primarily in gold loans, which exposes it to volatility in gold prices and borrower defaults.

Limited Geographic Diversification:

- Operations are primarily concentrated in Kerala and neighboring states, increasing regional risk exposure.

Moderate Credit Rating:

- While A (Stable) is investment grade, it’s below the highest safety rating (AAA), implying some risk.

NBFC Sector Sensitivity:

- Being an NBFC, MMFL is vulnerable to regulatory changes, interest rate fluctuations, and liquidity crunches in the financial system.

Liquidity Position

- Strong ALM Profile: Positive cumulative mismatches across all maturity buckets as of December 2024.

- Adequate Liquidity Buffers: Unencumbered liquidity of ₹88.9 crore and unused bank lines of ₹64.6 crore (February 2025). Monthly collections average ~₹700 crore, comfortably covering near-term debt obligations of ₹539.2 crore (March–May 2025).

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Muthoottu Mini Financiers Limited

Muthoottu Mini Financiers Limited (MMFL), founded in 1998, transitioned from an investment company to a leading non-banking financial company specializing in gold loans by 2007. Now operating through 907 branches across 12 states, MMFL has built a strong presence in South India, with a loan portfolio of ₹3,525 crore as of June 2024. The company also offers microfinance and property loans, alongside facilitating money transfer services for providers like Western Union, focusing on financial inclusion for diverse communities.

Strengths

- Established Track Record:

- MMFL benefits from the Muthoottu Group’s strong brand reputation and six decades of experience in gold loans.

- Senior management has extensive industry expertise, supporting consistent business growth.

- Healthy Asset Quality:

- Gross Stage 3 (non-performing assets) stood at a low 0.9% as of March 2024.

- Gold loan delinquencies (90+ dpd) were 0.9% in December 2024, with auction recoveries historically ranging between 95% and 105%.

- Adequate Capitalization:

- Gearing ratio improved to 4.9x (December 2024) from 5.1x (March 2024), supported by internal accruals.

- Capital Adequacy Ratio (CRAR) remained robust at 23.5% (Tier I: 17.5%) as of December 2024.

- Improving Profitability:

- Return on Managed Assets (RoMA) rose to 2.2% in 9M FY2025 from 1.6% in FY2022, driven by higher-yielding gold loans (89.6% under ₹3 lakh ticket size).

Weakness

- Geographic Concentration:

- 95.4% of the loan portfolio is concentrated in South India (Tamil Nadu alone contributes 33.3%), exposing MMFL to regional risks.

- Moderate Scale & Competition:

- Portfolio growth slowed to 8.3% in 9M FY2025 (vs. 30.6% in FY2023) due to a shift toward smaller-ticket loans.

- Faces intense competition from banks and large NBFCs in the gold loan segment.

- Microfinance Risks:

- Microfinance (7.8% of portfolio) saw 90+ dpd rise to 5.0% (December 2024) from 2.2% (March 2024), with ₹1.5 crore write-offs in 9M FY2025.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus April 11, 2025

Disclaimer- The information is published as on date 04/25/2025 based on information available on Prospectus April 11, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors