|

Getting your Trinity Audio player ready...

|

High Yield | Crisil AA+/Stable & IND AA+/Stable Rated | Minimum Investment: 10k Only

Bond overview:

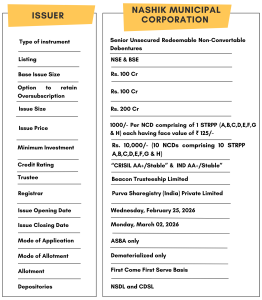

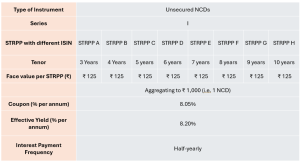

Nashik Municipal Corporation is offering unsecured, redeemable Non-Convertible Debentures (NCDs) that carry a provisional ‘AA+/Stable’ credit rating from CRISIL and India Ratings and Research (IND). The issuance comprises eight STRPPs* with distinct tenors of 3,4,5,6,7,8,9 and 10 years, each having a face value of ₹125.

*Separately Transferable and Redeemable Principal Parts (STRPPs) are a specialized bond structure where the principal amount of a single bond is split into multiple parts, each with its own maturity date and ability to be traded independently.

Coupon rates and effective yield for each of the series:

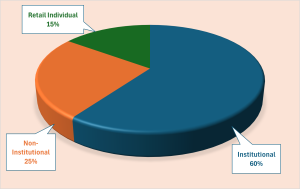

Allocation Ratio:

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Nashik Municipal Corporation NCD-IPO.

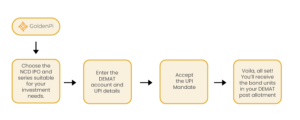

Investment Process for Nashik Municipal Corporation NCD IPO:

You can invest in IPOs via GoldenPi in 3 easy steps.

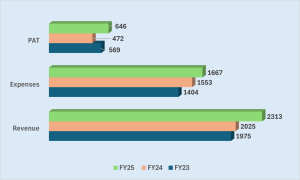

Financial Overview:

Snapshot stating the Revenue, Expenses and PAT ( In Crores):

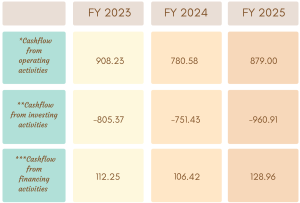

Cash flow for last few years ( In Crores):

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

Issue analysis:

Pros:

- Strong Credit Rating: Rated AA+/Stable by Crisil and India Ratings indicating high degree of safety and low credit risk.

- Attractive Coupon : All STRPP (A,B,C,D,E,F,G & H) carry an 8% coupon, competitive compared to FDs (5%-7.8%).

- Green Bond Incentives: Issuance under the AMRUT 2.0 framework , with eligibility for central government incentives for green municipal bonds.

- Wide tenor : 3,4,5,6,7,8,9 & 10 Yrs providing flexibility to investors.

- Listing Benefit: Proposed to be listed on NSE and BSE, improving liquidity for investors.

- Use of Proceeds: Proceeds earmarked for sustainable infrastructure projects ( Water supply, waste processing, water treatment and Sanitation), aligning with ESG-focused investments.

Cons:

- Municipal Risk Profile: Unlike corporate issuers, municipal corporations depend heavily on tax/non-tax revenues and grants; delays or shortfalls in collection could affect servicing.

- Project Execution Risk: Funds are tied to multiple infrastructure projects; delays, cost overruns, or regulatory hurdles could impact repayment capacity.

- Interest Rate Risk: If interest rates rise significantly over 4-10 years, the fixed 8% coupon may become less attractive.

- Limited Investor Base: While open to retail, institutional appetite will largely drive liquidity and secondary market performance.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Nashik Municipal Corporation:

The Nashik Municipal Corporation (NMC), established on November 7, 1982, serves as the governing body for Nashik city in Maharashtra, India. Operating under the Bombay Provincial Municipal Corporation Act, 1949, the NMC is tasked with the administration and development of a 259.13 square kilometer area. Its key responsibilities encompass urban planning, infrastructure management, and providing essential civic services to its 1.49 million residents (based on the 2011 census). These services primarily include water supply, sewerage disposal, solid waste management, healthcare, and road maintenance.

Strengths:

- Strong Revenue Growth: NMC has demonstrated consistent revenue growth, with income rising from ₹2,025.45 crore in FY24 to ₹2,312.91 crore in FY25. This increase is indicative of enhanced collections and improved operational efficiency.

- Consistent Revenue Surplus: NMC has maintained a healthy revenue surplus (₹646.35 crore in FY25 vs 471.79 Crore in FY24), indicating strong operating performance and sound financial management.

- Healthy Cash Position: Closing cash and bank balance stood at ₹915.17 crore in FY25 ( vs 868.11 crore in FY24 & 732.53 crore in FY23), providing strong liquidity to fund infrastructure and development projects.

- Strong escrowed revenue-backed structure: Entire own-revenue collections (tax and non-tax) are escrowed with a clearly defined waterfall (money flows from one priority level down to the next); escrow revenues increased to ₹663.60 crore in FY25 (FY24: ₹448.50 Crore), providing adequate cover for debt servicing.

- Trustee-monitored payment discipline: All escrow, Interest payment A/c (IPA) and Sinking Fund Account (SFA) accounts are monitored by the debenture trustee, ensuring strong control on cash flows and timely servicing of bond obligations.

- Robust and well-defined debt servicing mechanism: Structured payment mechanism with DSRA equivalent to one year of interest (in IPA) , SFA funded on priority basis; surplus withdrawal permitted only with trustee consent.

- Consistent operating surplus and low debt profile: Revenue surplus maintained over FY21-FY25 (FY25 surplus: ₹687.90 Crore); NMC was debt-free for over five years prior to the current bond issuance, supporting strong DSCR comfort.

- Healthy own-revenue base with low reliance on grants: NMC relies primarily on its own revenues (property tax, water tax, fees, and user charges), showing limited dependence on government grants. Grant income was minimal, averaging ~3.3% from FY20 to FY25 (last 5 yrs), and fell to 1.76% in FY25.

- Superior liquidity position: Cash balances and unencumbered investments stood at ₹1700.7 crore as of FY25; internal policy to maintain liquidity equivalent to three months of operating expenses; no principal repayment obligations in FY26-FY27.

Weaknesses:

- Moderate property tax collection efficiency: Overall property tax collection efficiency remained below 33% during FY21-FY25, impacted by rising arrears; current collection efficiency ranged 59-62%, though improvement initiatives are underway.

- High dependence on assigned revenues (GST compensation): Assigned revenues averaged ~58% of total revenue (FY21-FY25), exposing cash flows to policy changes in inter-governmental transfers.

- Execution risk on capex and service upgrades: Ongoing AMRUT-funded projects for water supply and sanitation need timely completion to translate into measurable service-level improvements.

Invest in Bond IPO online in just 5 minutes

Source- Offer Document February 20, 2026

Disclaimer – The information is published as on date 25/02/2026 based on information available on Offer document February 12, 2026. The information may be subject to change in case of change in terms of prospectus or any other reason as the case may be. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors