High Yield | A+/ Stable | Minimum Investment: 10k Only

Bond overview

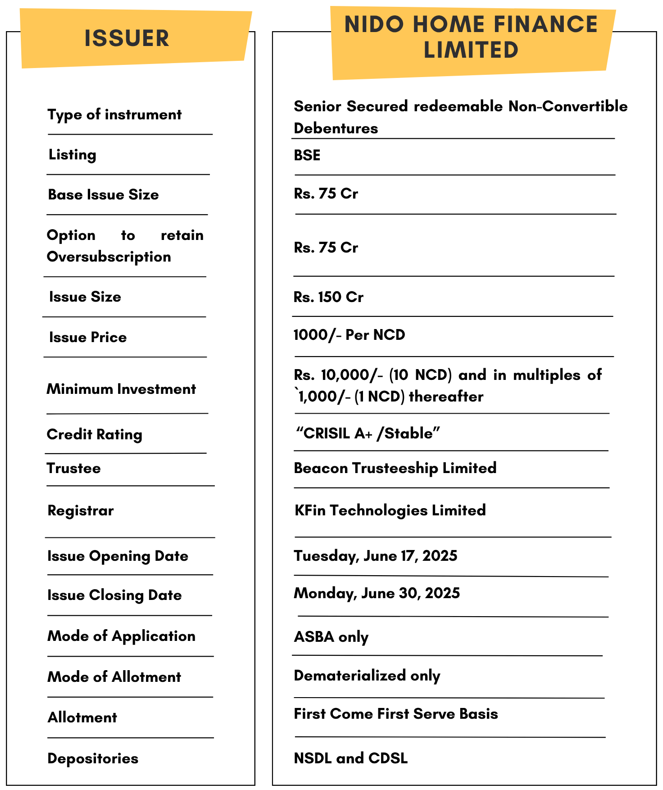

Nido Home Finance Limited is issuing the Non-Convertible Debentures. These NCDs are “CRISIL A+/Stable” rated. The NCDs are being issued in ten series: coupon ranges from 9.25% to 10.75% p.a. and different tenures of 24 months, 36 months, 60 months and 120 months. The NCDs are secured and redeemable in nature.

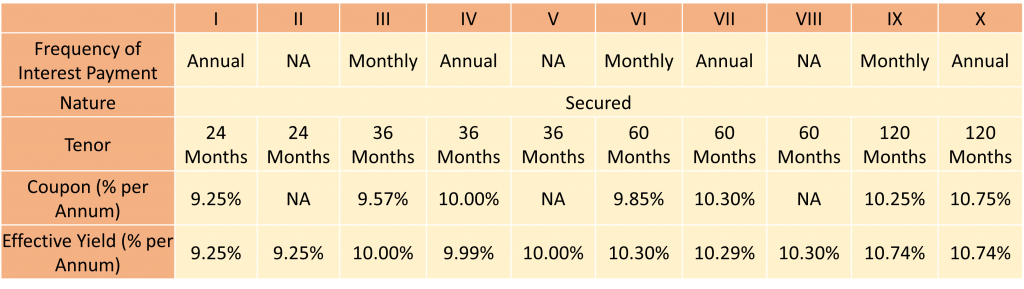

Coupon rates and effective yield for each of the series

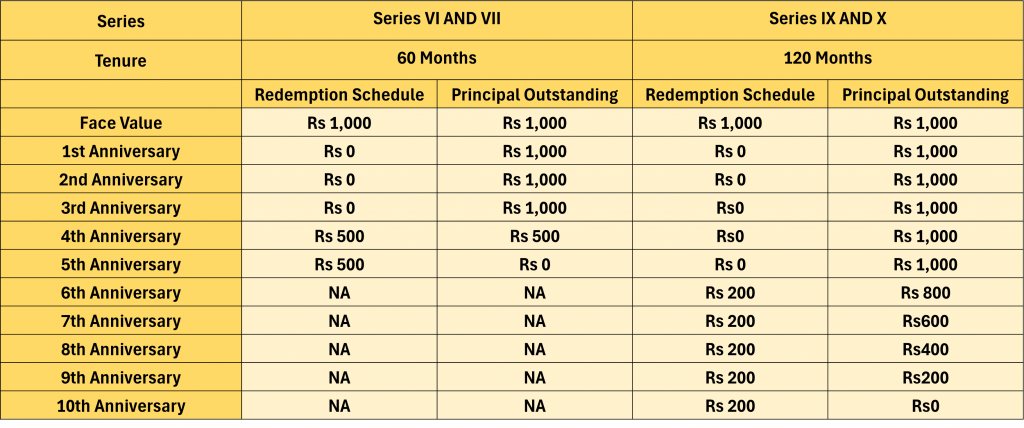

Redemption Payment Schedule

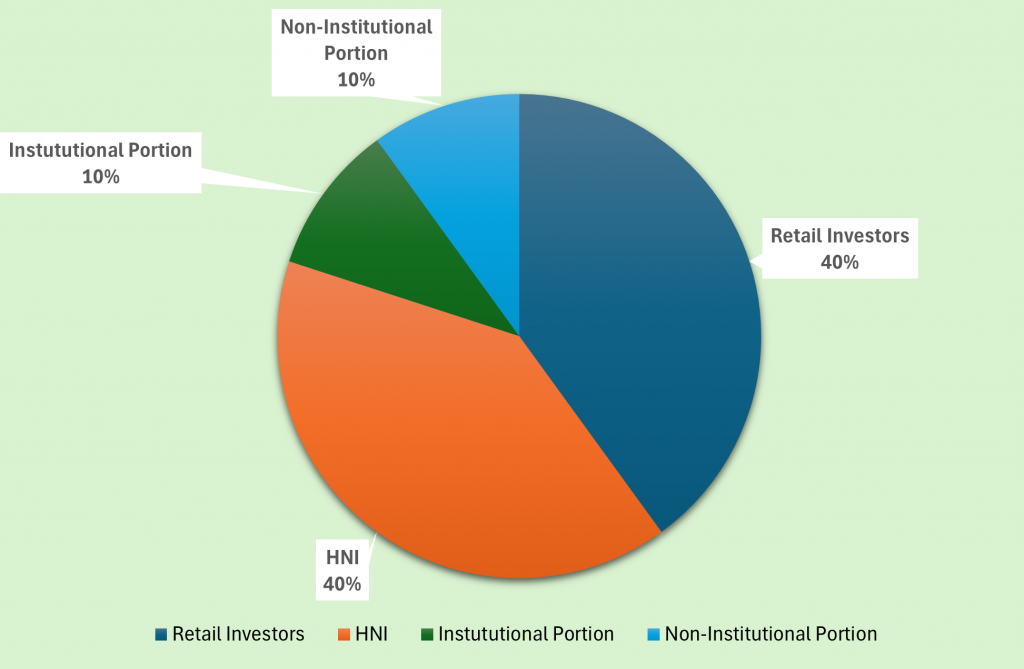

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Nido Home Finance Limited NCD-IPO.

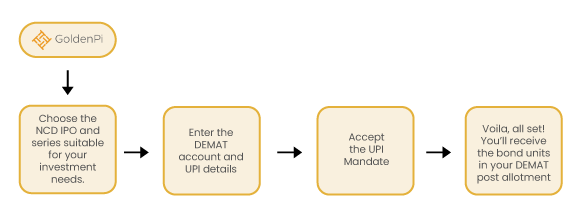

Investment Process for Nido Home Finance Ltd NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

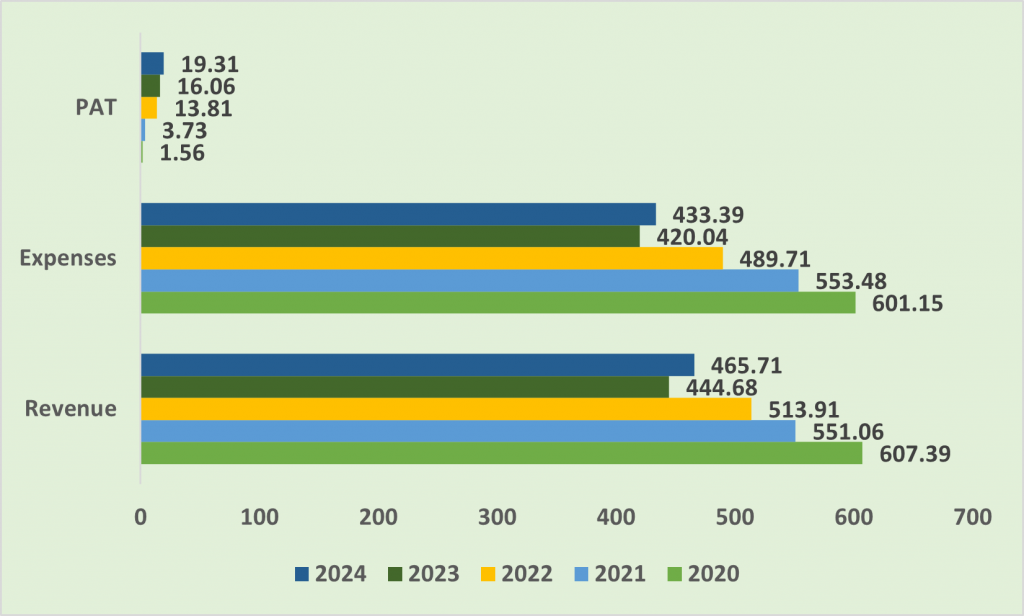

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

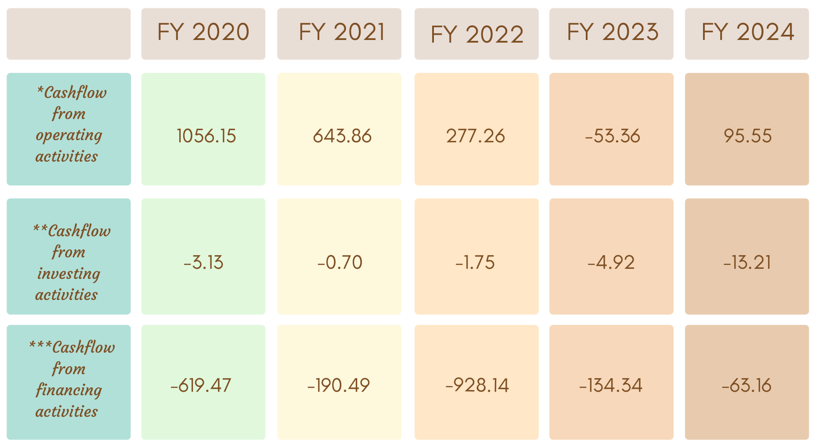

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

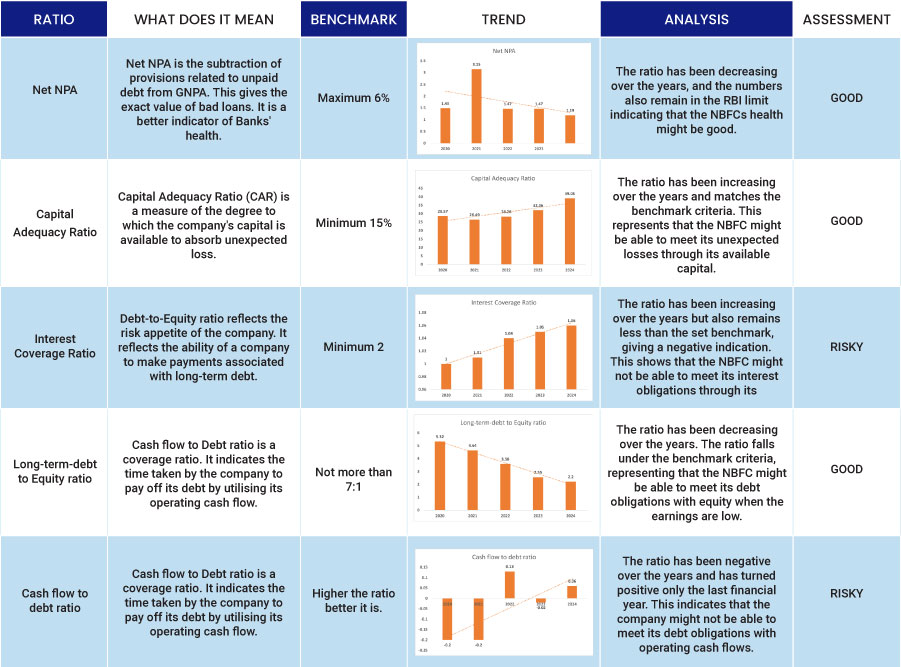

Ratio Analysis

Issue analysis

Pros

- Stable Credit Rating (CRISIL A+/Stable)

The NCDs are rated “CRISIL A+/Stable,” indicating adequate safety regarding timely servicing of financial obligations and relatively low credit risk.

- Secured NCDs

These debentures are secured by a pari-passu charge on the company’s loan receivables and current assets, with at least 100% asset cover—enhancing investor protection.

- Reputed Promoter Group

Nido is part of the Edelweiss Group, a known name in Indian financial services, which brings operational experience, credibility, and potential for stronger governance.

Cons

- Exposure to Real Estate Volatility

As a housing finance company, Nido’s collateral is tied to the real estate market. Any price correction or legal/regulatory issues in the realty sector could affect recoveries.

- Limited Business Track Record under New Name

While Nido was formerly Edelweiss Housing Finance, the rebranding and change of identity might limit brand recall and investor familiarity. - Macroeconomic Sensitivity

Rising interest rates, inflationary pressures, or regulatory tightening in the NBFC/HFC space could impact borrowing costs and NIMs (Net Interest Margins).

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Nido Home Finance Limited

Nido Home Finance Limited (Nido) is a housing finance company that is registered with National Housing Bank. It was established in FY2011 in accordance with the Group’s plan to establish a presence in the affordable housing market. In May 2023, the business changed its name to Nido Home Finance Limited (Formerly Edelweiss Housing Finance Limited) as part of the Group’s positioning effort. The business has adjusted its approach in recent years to concentrate on small-ticket home loans.

September 2024

Strengths

Strong Group Backing

- Wholly owned by Edelweiss Financial Services Ltd. (EFSL), providing operational, financial, and managerial support. EFSL has a diversified financial services portfolio and experience of nearly three decades.

Comfortable Capital Adequacy

- Capital adequacy ratio at 33.60% (above regulatory thresholds), indicating financial resilience.

Adequate Liquidity

- Liquidity buffer of ₹5240 crore and additional inflows expected from asset monetization support timely debt servicing.

Diversified Business Model (Group Level)

- Presence across lending, insurance, asset management, and ARC segments reduces business concentration risk.

Reduced Leverage

- Consolidated debt-to-equity ratio improved from 3.35x (FY24) to 3.02x (FY25); standalone D/E for Nido at 3.79x.

Weakness

Deterioration in Asset Quality

- Nido’s GNPA/NNPA worsened to 2.17%/1.77% in FY25 from 1.46%/1.19% in FY24. This raises concerns over credit underwriting.

Decline in Profitability

- While interest income rose, PAT dropped 3.5% YoY due to a significant rise in impairment (₹10.68 Cr in FY25 vs ₹1.65 Cr in FY24).

Business Model Transition Risk

- Shift from wholesale to retail (co-lending focused) has not yet achieved optimal scale; growth is slower-than-expected.

High Exposure to Group Risk

- Rating heavily depends on the financial and governance strength of the Edelweiss Group; any adverse event at group level could impact Nido.

Regulatory Scrutiny History

- Past RBI restrictions on group entities like ECL Finance and Edelweiss ARC signal heightened regulatory sensitivity.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus June 12, 2025

Disclaimer- The information is published as on date 6/16/2025 based on information available on Prospectus June 12, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors