|

Getting your Trinity Audio player ready...

|

High Yield | CRISIL AA/Stable Rated | Minimum Investment: 10k Only

Bond overview

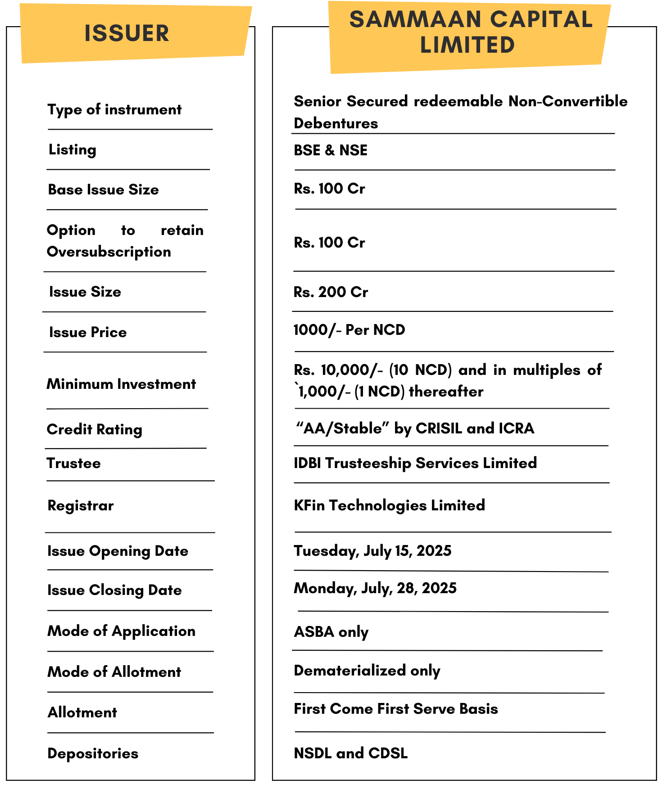

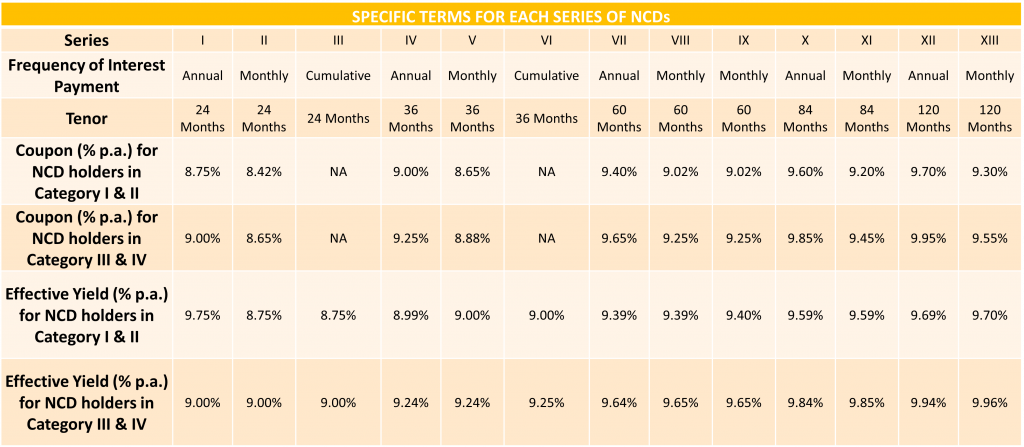

Sammaan Capital Limited is issuing the Non-Convertible Debentures. These NCDs are AA rated with stable outlook by CRISIL & ICRA. The NCDs are being issued in thirteen series: coupon ranges from 8.42% to 9.95% p.a. and different tenures of 24 months, 36 months, 60 months, 84 months, and 120 months. The NCDs are secured and redeemable in nature.

Coupon rates and effective yield for each of the series

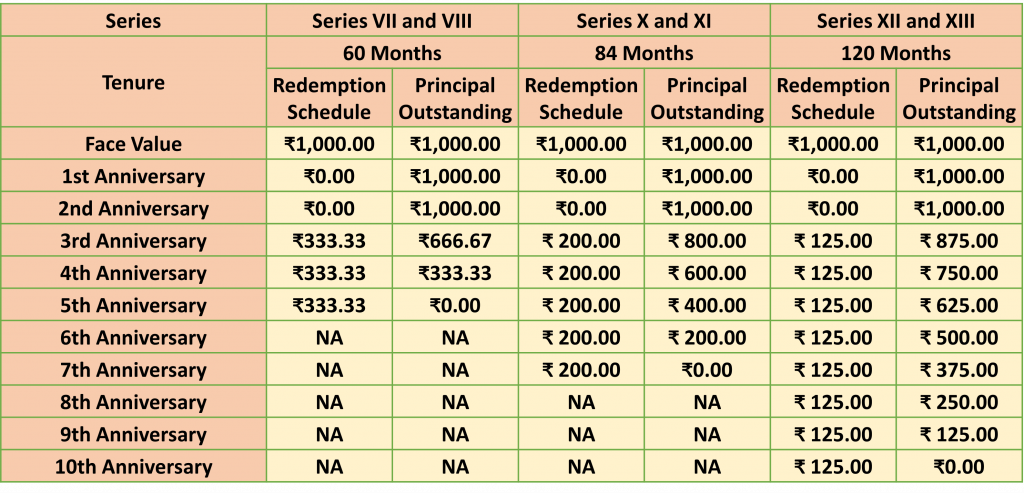

Principal Redemption Schedule and Redemption Amounts

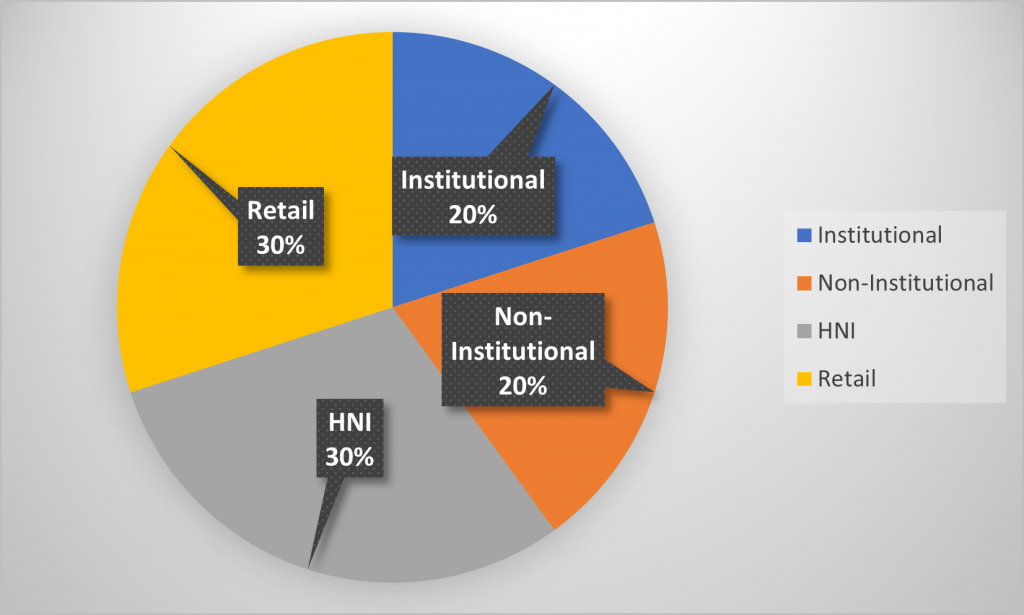

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Sammaan Capital Limited NCD-IPO.

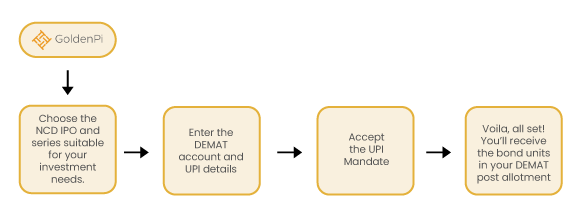

Investment Process for Sammaan Capital Limited NCD IPO

You can invest in IPOs via GoldenPi in 3 easy steps.

Issue analysis

Pros

- Attractive Yields

Yield goes up to 9.96% p.a., among the highest in the secured NCD category — ideal for yield-hunting investors. - Social Impact Investing

Investing supports a microfinance business model promoting women empowerment and rural income generation, aligning with ESG preferences. - Secured NCDs

The NCDs are secured by receivables with exclusive charge, enhancing investor safety in case of default. - Flexible Tenure Options

Options include 18, 24, 36, 60, and 75-month tenures with various payout modes (annual, monthly, cumulative).

Cons

- Low Liquidity on Exchange

Small-issue NCDs from MFIs often witness thin trading volumes, limiting secondary market exit options.

- Higher Risk Business Segment

The MFI sector is vulnerable to local political disruptions, regulatory caps on interest, and borrower repayment capacity issues.

- Limited Brand Recognition

As a smaller player in the microfinance space, Sammaan doesn’t enjoy the same brand recall or sponsor strength as larger NBFCs.

Liquidity Position

- Cash and equivalents stood at ₹48.4 crore as of March 31, 2025.

- Has unutilized sanctions of ₹45 crore from banks/FIs, providing buffer to meet near-term obligations.

- Positive cumulative mismatches in all time buckets (as per ALM profile), indicating comfortable short-term liquidity .

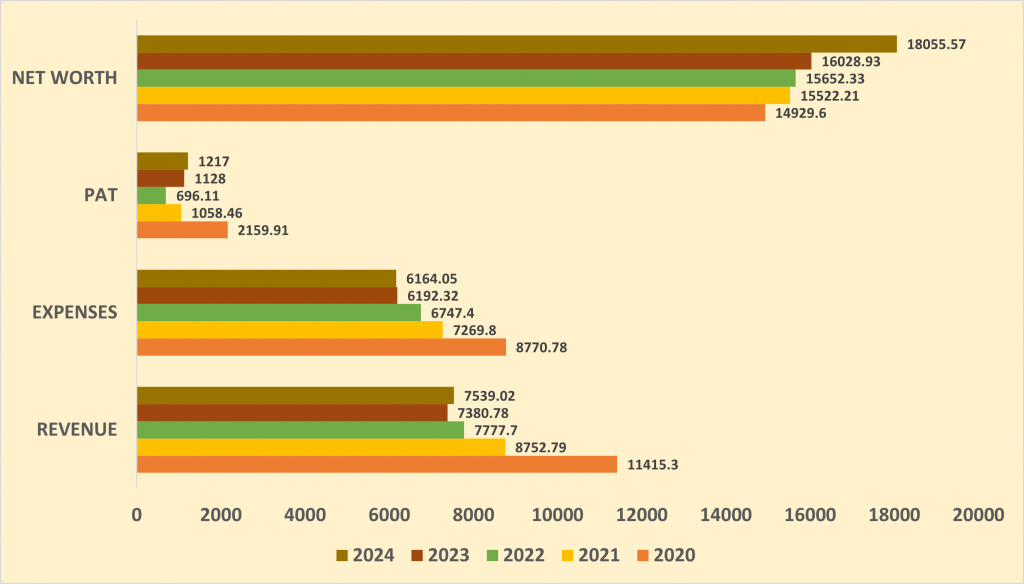

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

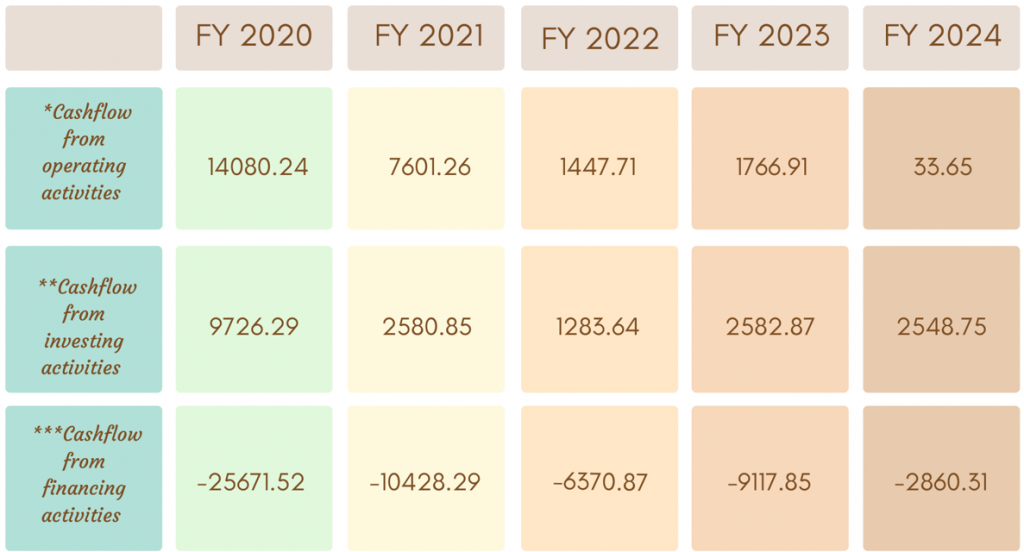

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

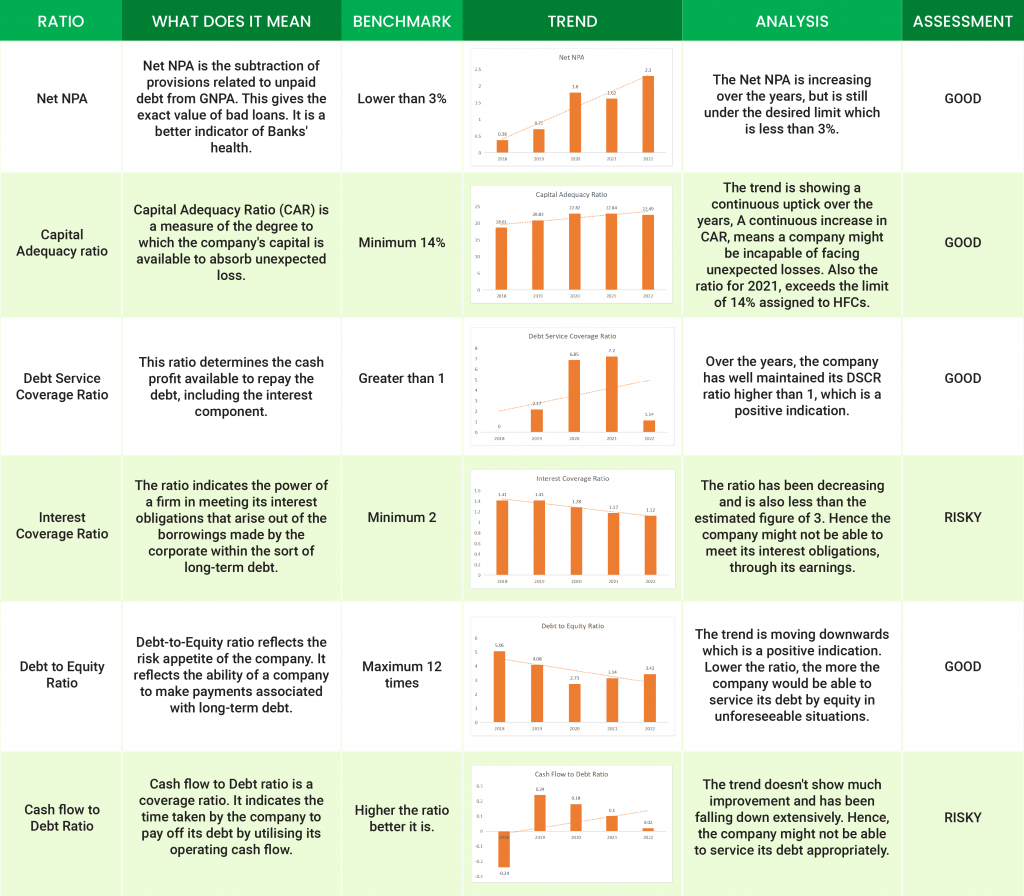

Ratio Analysis

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Sammaan Capital Limited

Sammaan Capital Limited is a prominent non-banking financial company (NBFC) primarily engaged in retail mortgage lending across India. The company has built a strong portfolio catering to individual homebuyers and small-business borrowers, particularly in underserved markets. Known for its prudent risk management and scalable operations, Sammaan has emerged as a significant player in the housing finance space.

As of FY2025, Sammaan Capital manages a diversified funding base comprising long-term and short-term instruments, including non-convertible debentures (NCDs), commercial papers, and subordinated debt. It has secured high credit ratings from CRISIL — AA (Stable) for long-term and A1+ for short-term borrowings — reflecting its strong capital position, robust asset quality in the retail segment, and disciplined underwriting practices.

With plans to transition toward a funding-light business model, Sammaan Capital is strategically repositioning itself to enhance operational efficiency and reduce funding concentration risks, while maintaining its focus on stable, asset-backed lending.

Strengths

-

Strong Credit Ratings & Large Scale Facilities

-

Maintains high ratings: CRISIL AA (Stable) for long-term and A1+ for short-term instruments.

-

Rated bank loans amounting to ₹24,550 crore, along with ₹4,000 crore in subordinated debt, ₹1,000 crore in short-term NCDs, ₹25,000 crore in commercial paper, ₹22,425 crore in NCDs, and ₹13,566 crore in retail bonds.

-

-

Robust Capitalisation & Asset Quality

-

CRISIL specifically highlights “strong capitalisation with healthy cover for asset-side risks” and “comfortable asset quality in retail segment”.

-

-

Significant Market Presence

-

A sizeable player in the retail mortgage finance sector, catering to individual homebuyers and small-business lending

-

Weaknesses

-

Strategic Transition Underway

-

The company is in the midst of shifting to a “planned new funding-light business model”. Demonstrating the success of this transition remains a key challenge.

-

-

Exposure to Commercial Real Estate (CRE)

-

Asset quality may be vulnerable due to significant exposure to CRE portfolios—a segment sensitive to economic cycles.

-

Invest in Bond IPO online in just 5 minutes

Source- Tranche IV Prospectus July 8, 2025

Disclaimer- The information is published as on date 07/14/2025 based on information available on Tranche IV Prospectus July 8, 2025. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors