|

Getting your Trinity Audio player ready...

|

Summary: Capri Global Capital Limited is issuing the Non-Convertible Debentures. These NCDs are AA/Stable rated by ACUITE and AA/Positive rated by IVR. The NCDs are being issued in six series: coupon ranges from 8.80% to 9.50% p.a. and different tenures of 24 months, 36 months, 60 months and 120 months. The NCDs are secured and redeemable in nature.

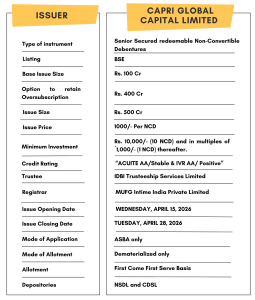

Capri Global Capital Limited NCD IPO: Issue Overview

Capri Global Capital Limited is issuing Secured, Redeemable Non-Convertible Debentures (NCDs). This issue is a strategic opportunity for investors looking for fixed-income assets with a high degree of safety.

- Credit Rating: AA/Stable (ACUITE) and AA/Positive (IVR)

- Yield Range: 8.80% to 9.50% p.a.

- Tenures: 24, 36, 60, and 120 months.

- Nature: Secured and Redeemable.

- High Yield | AA/Stable | Minimum Investment: 10k Only

Capri Global NCD Interest Rates and Effective Yields

The NCDs are being issued in six different series to cater to different investor needs, ranging from short-term liquidity to long-term wealth compounding.

| Series | I | II | III | IV | V | VI |

| Frequency of Interest Payment | Annual | Monthly | Annual | Monthly | Annual | Annual |

| Nature | Secured | Secured | Secured | Secured | Secured | Secured |

| Tenor | 24 Months | 36 Months | 36 Months | 60 Months | 60 Months | 120 Months |

| Coupon (% per Annum) | 9.00% | 8.80% | 9.15% | 8.93% | 9.30% | 9.50% |

| Effective Yield (% per Annum) | 8.99% | 9.15% | 9.14% | 9.30% | 9.29% | 9.49% |

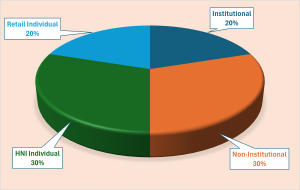

Understanding the Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories.

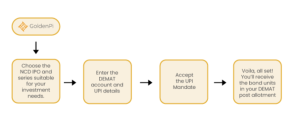

How to Invest in Capri Global NCD IPO via GoldenPi

Investing in Bond IPOs is now seamless. Follow these easy steps:

- Log in to GoldenPi.

- Look for the Search option and type Capri Global Capital

- Select Capri Global NCD IPO or directly check this link – Capri Global NCD IPO.

- Choose your series and apply via UPI.

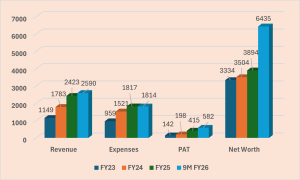

Financial Overview of Capri Global Capital Limited

A deep dive into the company’s balance sheet reveals a consistent growth trajectory in revenue and net worth.

Snapshot stating the Revenue, Expenses, PAT, Net Worth (In crores):

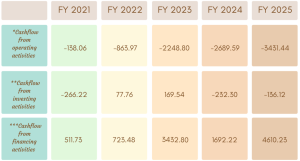

Cash Flow Analysis (In crore)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

Source – https://www.capriloans.in/documents/financial-reports/

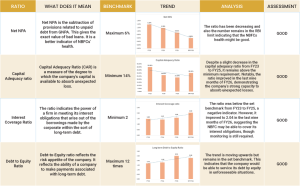

Ratio Analysis:

Should You Invest? Pros and Cons of Capri Global NCD

Pros:

- Strong Credit Rating: Rated ACUITE AA/Stable and IVR AA/Positive, indicating high safety and low credit risk.

- Secured NCDs: Backed by receivables, loan book, and bank balances with 1.10x security cover.

- Listed on BSE: Provides potential liquidity for investors via stock exchange.

- Trusted NBFC: Capri Global has operated since 1994, serving MSME, housing, gold & construction finance.

- Clear Fund Usage: Funds raised will go towards lending, financing, and working capital – core NBFC activities.

Cons:

- Interest Rate Risk: Fixed returns may underperform if market interest rates rise. More pronounced in longer tenors (60-120 months).

- Limited Liquidity: Secondary markets for NCDs can be illiquid, resale may be difficult.

- Sector Vulnerabilities: NBFC business is exposed to asset quality (NPAs), interest rate spreads, and regulatory changes.

- Pari-Passu Charge: In case of default, recovery is shared with other secured lenders – no priority for this issuance.

Must Check: To get better returns than Bank FDs, invest in NCD-IPOs online.

About Capri Global Capital Limited (CGCL)

Capri Global Capital Ltd., incorporated in 1994 and listed on NSE & BSE, is a systemically important non-deposit taking NBFC (NBFC-ND-SI) registered with the RBI. Headquartered in Mumbai, CGCL operates through 1331 branches across India (as of Dec 31st, 2025).

The company has built a diversified lending portfolio spanning:

- MSME loans (core segment)

- Affordable housing finance (via Capri Global Housing Finance)

- Construction finance (real estate developers)

- Gold loans (fastest-growing vertical with ₹12,799.2 Cr book as of Dec 2025)

CGCL is positioned as a retail-focused NBFC addressing India’s large credit gap for MSMEs, affordable housing, and emerging retail borrowers. Its recent ₹2,000 Cr QIP equity raise (Q1FY26) from marquee investors (MFs, FIIs, insurers) underscores market confidence in its growth trajectory.

Strengths:

- Robust shareholding structure: Demonstrating high confidence in the business. Promoter Group (~60%), DIIs/FIIs (~25%): LIC (8.21%), Quant MF (~3%), SBI Life insurance (2.11%) and Societe Generale (1.07%).

- Experienced management: Promoted by Rajesh Sharma (30+ years experience in BFSI); strong board (7 members have 30-40+ yrs experience in BFSI)

- Strong Debt Partnership: Public sector banks (SBI, PNB, BOB, Canara), Private Sector banks (HDFC, ICICI, Axis) and NBFCs ( Bajaj finance).

- Well-diversified product portfolio: Gold loans (42.0%), MSME loans (19.36%), housing loans (17.80%) and construction finance (17.80%) with 1331 branches.

- Robust AUM Growth: Consolidated AUM rose with 48.83% CAGR to ₹22,860 Cr (FY25) from ₹10,320 Cr ( FY23); Q3 FY26 at ₹30,406 Cr. ( 47% increase YoY).

- Profitability Surge: PAT more than doubled (122% Increase YoY) – ₹300.80 Cr (9M 2025) → ₹666.30 Cr Cr (9M FY26); RoAA at 3.7% vs 2.4% (YoY)

- Improving Asset Quality: Net NPA declined to 0.7% (9M 2026) vs 1.00% (9M 2025).

- Capital Support: Net worth of ₹6846 Cr (FY25); QIP equity raise of ₹2,000 Cr in Q1FY26 from MFs, FIIs & insurers strengthens buffers.

- Liquidity Adequate: No negative ALM mismatches across buckets (Dec’25). Cash & equivalents of ₹1,507 Cr (FY25); increased to ₹2350 Cr (9M FY26).

Weaknesses:

- Rising MSME Stress: MSME GNPA rose to 4.3% (June 2025) from 3.9% (March 2025). Its has improved to 3% (Dec 2025) but still high.

- Construction Finance Risk: ~18% of AUM exposed to cyclical real estate; delays could pressure asset quality.

- Moderate Earnings vs Peers: Though improving, RoNW only at 11.8% (FY25); Opex/earning assets high at 6.75%.

- Young Loan Book: Rapid expansion in gold/MSME loans = limited seasoning; asset quality stability remains to be tested.

Invest Now: Invest in Bond IPO online in just 5 minutes

Source– Tranche I Prospectus March 30, 2026

Disclaimer – The information is published as on date 08/04/2026 based on information available on Tranche I Prospectus March 30, 2026. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors