|

Getting your Trinity Audio player ready...

|

When entering the fixed-income market, many investors treat bond yield and interest rate as if they were interchangeable. Even though these terms are related, using them that way is incorrect.

For folks diving into bond investments or similar fixed-income products, knowing the difference between bond yield and interest rate is super important. Interest rates affect borrowing costs throughout the whole economy, but bond yields show what investors actually get back based on current prices.

How these elements interact greatly influences bond pricing, the health of the debt market, and general investor mood too. Being clear on how bond yields and interest rates function can seriously benefit your decision-making whether you’re looking at government bonds, corporate bonds, or debt funds.

What is an Interest Rate?

An interest rate shows the percent charged for borrowing money or earned on deposits and investments. It’s pretty straightforward—this rate is what you pay to borrow, or what you get for saving cash.

You see interest rates all over the place too—loans from banks, fixed deposits, savings accounts, bonds, government securities, and when companies take out loans.

The Reserve Bank of India wields a lot of power here. They guide rates through policies like tweaking the repo rate.

So, when RBI hikes rates:

- Borrowing gets pricier

- Loan payments often go up

- Bond returns tend to climb

But if they lower rates:

- It becomes cheaper to borrow

- There’s more liquidity

- Bond returns might ease off

Thus, these rate changes ripple through the whole economy, affecting finance and business activity big time.

What is Bond Yield?

Bond yield is what investors get when they buy bonds. Unlike a fixed interest rate, the yield for bonds can change based on the market price.

There are a few things that go into calculating bond yield:

- The coupon payments

- What the bond’s selling for right now

- How much time’s left till it matures

- And its redemption value

When people talk about yields, they often focus on Yield to Maturity (YTM). This predicts what the overall return will be if you hold onto the bond till it matures.

Here’s an example: Say a bond has a fixed coupon rate of 8%. But if the market price goes up or down, the actual yield that new buyers get will change too. So, bond yields move around all the time in the financial markets.

Recent Post:

- Bond Yield vs Interest Rate: Understanding the Difference in Bond Investing

- Long-Term Bonds vs. Long-Term Stocks: Which Investment is Better for Wealth Creation?

- India’s Bond Market: India Considers Tax Cuts to Attract Foreign Bond Investors

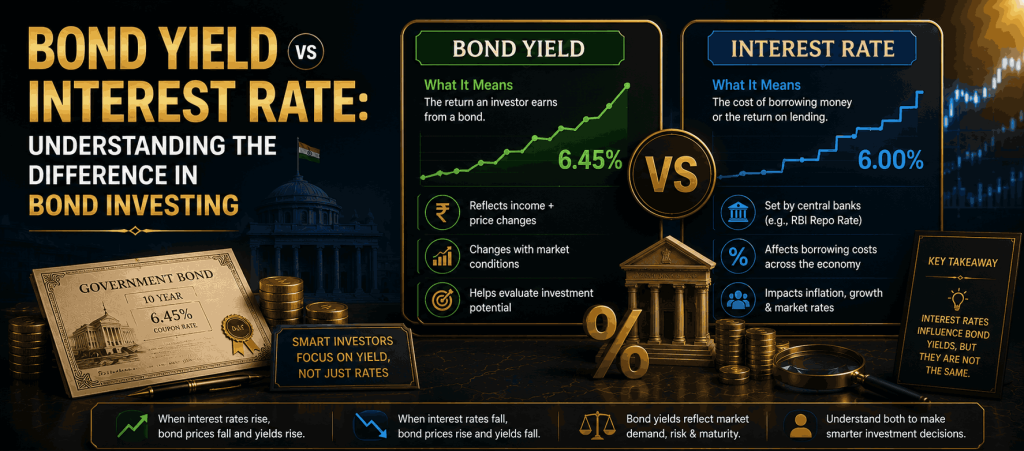

Bond Yield vs Interest Rate: The Core Difference

The biggest difference between bond yield vs. interest rate is that:

- Interest rate is usually fixed at the time the bond is issued

- Bond yield changes depending on market conditions and bond prices

Interest Rate

The interest rate, also called the coupon rate, is the fixed percentage paid by the bond issuer on the bond’s face value.

For example:

- A ₹1,000 bond with an 8% coupon pays ₹80 annually

This payment remains fixed unless specified otherwise.

Bond Yield

Bond yield depends on the price at which the bond is currently trading in the market.

If the same bond trades at:

- ₹900 > yield increases

- ₹1,100 > yield decreases

This happens because investors are paying different prices for the same fixed coupon payment.

Understanding Bond Yield with an Example

Let’s understand bond yield vs. interest rate with a simple example.

Suppose a company issues a bond with:

- Face value: ₹1,000

- Coupon interest rate: 8%

- Annual interest payment: ₹80

Scenario 1: Bond Trades at Face Value

If the bond trades at ₹1,000:

- Yield = 8%

Scenario 2: Bond Price Falls

If market interest rates rise and the bond price falls to ₹900:

- The investor still receives ₹80 annually

- Yield becomes higher than 8%

This is because ₹80 is now earned on a lower investment amount.

Scenario 3: Bond Price Rises

If interest rates decline and the bond price rises to ₹1,100:

- Coupon payment remains ₹80

- Yield becomes lower than 8%

The investor is paying more money for the same income stream. This explains why bond prices and yields move inversely.

Why Bond Yields Change

There are Several factors affecting bond yields in the market.

RBI Monetary Policy

The Reserve Bank of India’s decisions on interest rates directly impact bond yields.

When the RBI raises the repo rate:

- Bond yields rise

- Existing bond prices decrease

When the RBI lowers the repo rate:

- Bond yields decline

- Bond prices may increase

Inflation Expectation: Inflation expectations have a negative impact on the real return of bonds. As inflation expectations increase, the demand for higher yields also increases.

Economic Growth: If economic conditions are improving, the demand for borrowing and the expectation of rising interest rates increase, leading to higher bond yields.

Credit Risk: If the issuer of the bond is financially unstable, investors will demand higher yields to compensate for the increased risk.

Market Liquidity: Bonds are traded more frequently than other financial instruments, making the bond’s yield more stable than that of other financial instruments.

In addition to the factors listed above, the bond yield and interest rate influence debt mutual funds.

The majority of debt mutual funds invest in bonds or other fixed income securities; therefore, their net asset values fluctuate with movements in bond yields.

When interest rates rise:

- Bond yields increase

- Current bond prices decrease

- The net asset value of debt mutual funds will likely decrease temporarily.

When interest rates decline:

- Bond yields decrease

- Current bond prices increase

- The net asset value of debt mutual funds may increase.

Long-term bond funds will generally be more sensitive than short-term bond funds.

Must-Read Gold-Backed Bonds:

- Gold Price and Bond Market in India: Understanding the Relationship in 2026

- RBI Gold Bond Scheme Explained: A Simple Guide for 2026

- Are Gold Backed Bonds Safe? A Simple Guide for Investors in 2026

Bond Yield and Secondary Market Trading

One important feature of bonds is that they can usually be traded before maturity in the secondary market. Since bond prices fluctuate daily:

- Investors may earn capital gains if bond prices rise

- Investors may incur losses if bond prices fall

This is why bond yield differs from the original coupon interest rate. Secondary market pricing plays a major role in determining real-time bond yields.

Why Investors Should Understand Bond Yield vs Interest Rate

Understanding the difference between bond yield and interest rate helps investors:

- Evaluate bond investments correctly

- Understand debt mutual fund performance

- Make better interest rate decisions

- Manage portfolio risk effectively

- Identify opportunities in fixed-income markets

Many new investors focus only on coupon rates without considering market yields, which can lead to incomplete investment analysis.

Which is More Important: Bond Yield or Interest Rate?

Both are important, but they serve different purposes.

Interest Rate Matters For:

- Predictable coupon income

- Understanding fixed payments

- Comparing newly issued bonds

Bond Yield Matters For:

- Evaluating current market returns

- Comparing bonds in the secondary market

- Measuring investment attractiveness

Professional investors usually focus more on yield because it reflects real-time market conditions and return expectations.

Risks Associated with Bond Yield Movements

Bond yields can show drastic changes due to economic factors. Any of the following factors will create risk for the bondholder’s portfolio:

- Interest Rate Risk

- Inflation Risk

- Credit Risk

- Liquidity Risk

- Reinvestment Risk

Investors should recognize that as yields rise, the existing bondholder’s portfolio may experience short-term losses due to the rate increase.

Bond yield and interest rate: Frequently Asked Questions

Interest rate refers to the fixed coupon paid by the bond issuer, while bond yield represents the actual return based on the bond’s current market price.

Bond yields change because bond prices fluctuate due to interest rates, inflation, market demand, and credit risk.

No. Bond prices and yields generally move inversely.

When the RBI changes interest rates, bond yields and bond prices usually react accordingly.

For market investors, bond yield is often more important because it reflects the actual return based on current market conditions.

Rising yields reduce existing bond prices, which can temporarily lower debt mutual fund NAVs.

Yes, investors may earn capital gains if bond prices rise due to falling yields.

Conclusion

Understanding bond yield vs. interest rate is essential for anyone investing in fixed-income markets.

While interest rates determine fixed coupon payments, bond yields reflect the actual return investors earn based on market prices and economic conditions. The relationship between interest rates, bond prices, and yields influences everything from debt mutual fund performance to government borrowing costs and investor sentiment.

As India’s bond market continues to grow, investors who understand these concepts will be better equipped to manage risks, identify opportunities, and make informed fixed-income investment decisions.

Ready to Invest?

Visit GoldenPi to explore current bond options. Compare yields, ratings, and tenures in one place and invest online with as little as ₹30,000.

Disclaimer:

Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities and municipal debt securities/securitized debt instruments are subject to credit risks, market risks, and default risks, including delay and/or default in payment. Read all the offer-related documents carefully. This blog/article should not be construed as financial advice or as an offer or recommendation to buy or sell any security or any products/services of/on GoldenPi or any product/services of its third-party client(s). For a detailed calculation of YTM, visit our website. T&C’s Apply.