|

Getting your Trinity Audio player ready...

|

When most investors buy a bond, they usually focus on three things:

- What’s the interest rate?

- What’s the credit rating?

- When will I get my money back?

Fair enough.

After all, if a company is offering a 9% coupon and has a good credit rating, it seems like a decent investment.

But experienced debt investors often pay attention to something else hidden deep inside the bond document.

Imagine lending ₹10 lakh to a friend for five years.

Before handing over the money, you may ask him to agree to a few conditions:

- Don’t take too many additional loans.

- Keep some money in your bank account.

- Inform me if your financial situation worsens.

- Don’t sell your house without telling me.

Why would you impose these conditions?

Because once the money leaves your account, your biggest concern isn’t earning interest.

It’s getting your money back.

Debt investors think exactly the same way.

Whenever investors buy bonds or lend money to a company, they don’t simply rely on trust. They ask the borrower to follow certain rules and maintain financial discipline throughout the life of the loan.

These rules are known as covenants.

While they rarely make headlines, covenants are often the first line of defence between investors and potential losses.

Why Do Covenants Matter?

Most people think a company’s problems begin when it misses an interest payment or defaults on its debt.

In reality, warning signs usually appear much earlier.

Covenants act like a smoke alarm.

A smoke alarm doesn’t mean the building is on fire. It simply alerts you that something may be wrong and requires attention.

Similarly, when a company breaches a covenant, investors receive an early indication that financial conditions may be deteriorating.

For Investors

Covenants help investors by:

- Identifying financial stress at an early stage

- Ensuring management maintains financial discipline

- Providing mechanisms to protect investor capital

- Allowing timely intervention before a situation worsens

For Issuers

Interestingly, covenants also benefit companies.

By agreeing to stronger investor protections, companies can:

- Raise funds more easily

- Access a wider pool of investors

- Borrow at lower interest rates

- Build long-term credibility in debt markets

In simple terms: Greater investor protection often translates into lower borrowing costs.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowThe Three Types of Covenants

Not all covenants serve the same purpose.

Most bond issuances contain a combination of investor-friendly, issuer-friendly and financial covenants.

1. Investor-Friendly Covenants

These are designed primarily to protect investors.

Some common examples include:

| Covenant | Why It Matters |

| Step-up coupon clause | Investors receive a higher coupon if the issuer’s credit rating is downgraded |

| Promoter shareholding requirement | Ensures promoters retain meaningful skin in the game |

| Security cover requirement | Provides asset backing for the debt |

| Pre-payment penalty | Prevents issuers from refinancing too easily when rates fall |

| Mandatory early redemption | Allows investors to exit under specific adverse events |

One of the most popular investor protections is the step-up coupon covenant.

Suppose a bond carries a coupon rate of 9%.

The bond document may specify:

- Rating downgrade by one notch → Coupon increases by 0.25%

- Rating downgrade by two notches → Coupon increases by 0.50%

In this case, if the rating falls from AA to AA-, the coupon automatically increases from 9.00% to 9.25%.

The logic is simple: Higher risk should mean higher compensation.

2. Issuer-Friendly Covenants

Not every covenant benefits investors.

Some are included to provide flexibility to the borrower.

Examples include:

| Covenant | Why It Matters |

| Step-down coupon clause | Coupon reduces if the issuer’s rating improves |

| Issuer buyback option | Allows the company to repurchase bonds from the market |

| Call option | Allows early redemption before maturity |

For example, if a company’s rating improves significantly, it may no longer need to pay the same high coupon.

A step-down covenant allows borrowing costs to reduce as credit quality improves.

Think of it as a reward for maintaining strong financial performance.

3. Financial Covenants

These are perhaps the most closely monitored covenants in debt markets.

Rather than focusing on specific actions, they track a company’s financial health.

Common examples include:

- Capital Adequacy Ratio (CAR) – especially for NBFCs/MFIs

- Debt-to-Equity Ratio

- Net Worth

- Profitability Metrics

- Gross NPA and Net NPA Levels

- Liquidity Ratios

But where do investors actually find these covenants?

For listed NCDs, the answer is usually the Information Memorandum (IM) – the primary legal document issued along with the bond. It contains the detailed terms and conditions governing the issuance, including the covenants agreed between the issuer and investors.

In other words, the IM is not just a regulatory document – it is the rulebook that defines both the issuer’s obligations and the protections available to bondholders throughout the life of the bond. This is why experienced debt investors don’t stop at the credit rating – they also spend time understanding the Information Memorandum, especially the sections dealing with covenants, security, events of default and investor rights.

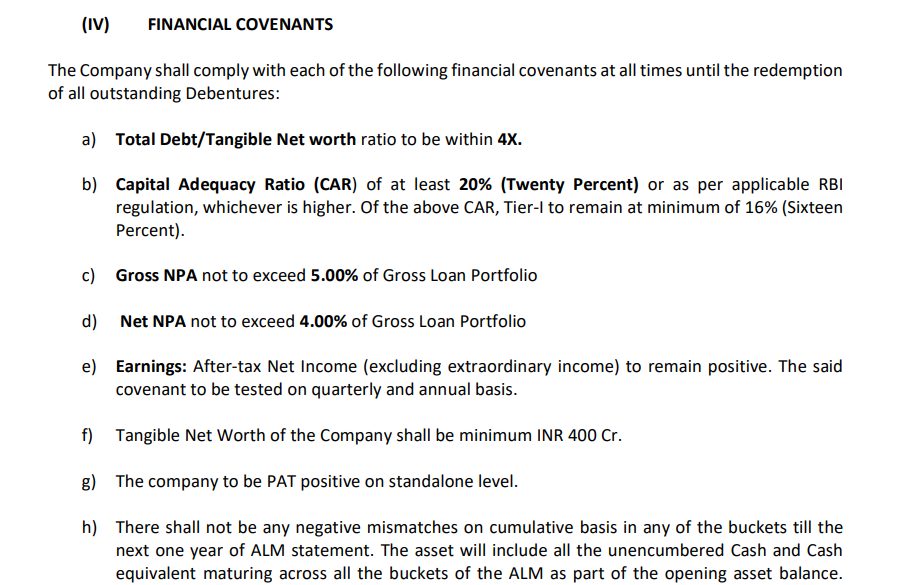

Below is a sample financial covenant extracted from an Information Memorandum (IM):

These covenants function much like a regular health check-up.

As long as financial parameters remain within agreed limits, investors remain comfortable.

When these metrics deteriorate, concerns begin to emerge.

Why Do Covenant Breaches Happen?

Over the past few years, covenant breaches have become increasingly common across sectors such as MSME lending and microfinance. However, covenant breaches rarely happen overnight. They are usually the result of a gradual deterioration in a company’s financial health.

A common pattern is as follows: During periods of strong economic growth, lenders often expand their loan books aggressively. As credit demand remains high and default rates stay low, competition for growth may lead some lenders to relax their underwriting standards, lend to riskier borrowers, or enter new markets.

The real challenge begins when the economic cycle turns.

As economic activity slows, some borrowers find it difficult to repay their loans. This leads to a deterioration in asset quality, higher provisioning requirements (credit costs), lower profitability and, in some cases, weaker capital and liquidity positions.

When these financial metrics fall below the thresholds agreed with investors, the company may breach its financial covenants – even if it continues to service its interest and principal payments on time.

In short, covenant breaches are often an early warning sign that a company’s financial health is weakening, rather than an indication that it has already defaulted.

Recent years have seen investors closely monitor covenant compliance among institutions such as Fusion Finance, Ashirwad Micro Finance, as operating conditions became more challenging.

The important point is this: covenant breach does not necessarily indicate default.

However, it often signals that investors should pay closer attention.

What Happens When a Covenant Is Breached?

When a covenant breach occurs, the process typically begins with the debenture trustee informing bondholders.

Investors then assess the seriousness of the situation and discuss potential remedial actions.

Depending on the circumstances, investors may choose to:

- Waive the breach

- Seek additional disclosures

- Demand higher coupon payments

- Request additional collateral

- Trigger early redemption provisions

The outcome depends on the company’s overall financial position and the nature of the breach.

A temporary breach caused by short-term stress is viewed very differently from a breach arising from structural financial weakness.

The Real Cost of a Covenant Breach

Even when a company continues making interest payments on time, covenant breaches can create significant challenges.

Potential consequences include:

| Potential Consequence | Impact |

| Rating Pressure | Credit rating agencies may reassess the issuer’s risk profile. |

| Higher Borrowing Costs | Future fund-raising may become more expensive. |

| Reduced Access to Capital | Banks and investors may become more cautious. |

| Technical Default | Certain covenant breaches can trigger default provisions even if interest payments remain current. |

| Liquidity Pressure | The company may need to arrange funds quickly to meet covenant requirements or investor demands. |

In many cases, the reputational impact can be as damaging as the financial consequences.

Conclusion: The Most Important Part of a Bond May Be Hidden in the Fine Print

Most investors focus on coupon rates, credit ratings and maturity dates when evaluating bonds.

While these factors are important, experienced debt investors often pay equal attention to the covenant package.

Why?

Because credit ratings tell investors where a company stands today.

Covenants help investors understand what might happen tomorrow.

They provide early warning signals, encourage financial discipline and create accountability between borrowers and lenders.

In a market where preserving capital is often more important than chasing the highest yield, covenants are far more than legal clauses buried in bond documents.

They are one of the strongest safeguards available to debt investors.

Frequently Asked Questions About Covenants

1. What is a covenant?

A covenant is a contractual condition that requires the issuer to follow certain financial or operational rules throughout the life of the bond. These covenants are designed to protect bondholders and reduce credit risk.

2. Why are covenants important for bond investors?

Covenants provide an early warning if a company’s financial health starts deteriorating. They also give investors certain rights and protections before a payment default occurs.

3. Does a covenant breach mean the company has defaulted?

No. A covenant breach does not automatically mean the company has defaulted. It is usually an early warning sign that certain agreed financial or operational conditions have not been met. In many cases, the company continues to pay interest and principal on time. However, investors should monitor the situation closely, as repeated or severe breaches may indicate increasing credit risk.

4. Where can investors find the covenants of a bond?

Most bond covenants are disclosed in the Information Memorandum (IM) or the bond’s offering document. The IM outlines the issuer’s obligations, financial covenants, security cover, events of default, and the rights available to bondholders during the life of the bond.

5. What happens when a company breaches a covenant?

Most bond covenants are disclosed in the Information Memorandum (IM) or the bond’s offering document. The IM outlines the issuer’s obligations, financial covenants, security cover, events of default, and the rights available to bondholders during the life of the bond.

Disclaimer:

This information is for general information purposes only. GoldenPi makes no guarantee on the accuracy of the data provided here; the information displayed is subject to change and is provided on an as-is basis. Nothing contained herein is intended to or shall be deemed to be investment advice, implied or otherwise. Investments in the securities market are subject to market risks. Read all the offer-related documents carefully before investing.

Bonds or non-convertible debentures (NCDs) are regulated by the Securities and Exchange Board of India and other government authorities. GoldenPi Securities Private Limited is a registered debt broker and acts as a distributor and not as a manufacturer of the product.