Types | Advantages | Disadvantages | Investment Process

As the name suggests, the bonds issued by corporates are called Corporate Bonds.

Yes, we know you want to know more than the definition of Corporate Bonds.

Here is a blog that explains how corporate bonds work, the advantages of investing in them, and how the corporate bond market functions.

Corporates issue debt securities, i.e., bonds, to raise capital to be utilized for their growth and business operations. Like any other bond, corporate bonds provide coupon payments at a fixed rate at predetermined dates – monthly/ quarterly/ bi-annually/ annually- till maturity. On maturity, the bond investor receives back his principal amount. Compared to government bonds, corporate bonds are relatively riskier. Corporates offer higher yields than Government Bonds, popularly called ‘G-secs.’ which is why investors often explore high yield bonds to enhance portfolio returns. The corporate bonds assigned “A-grade” or above by credit rating agencies are considered safer instruments to invest in.

Credit Rating Agencies study the debtor’s credit history and predict the ability to pay back the bonds or other debt instruments. Based on these and other relevant parameters, Agencies then provide a forecast on the debtor defaulting possibility.

Types of Corporate Bonds in India

Fixed-Rate: This is the most common type of corporate bond that carries a fixed rate of interest(called coupon rate) till maturity.

Example:

Issuer: Mahindra & Mahindra Financial Services Limited

Coupon Rate: 9% p.a

ISIN: INE774D08MA6

Zero-Coupon: Zero-coupon bonds do not provide interest payouts. They are sold at a highly discounted value. On maturity, the investor receives the face value of the bond.

Example :

Suppose Bond A carries a face value of Rs 1000. It is sold at a discounted value of Rs 750 to the investor. It matures in 3 years. On maturity, the investor receives Rs 1000, thus making an annualized gain of 10%

Tax-Free: These Bonds and issued only by PSUs. The interest income from these Bonds is 100% tax exempted by the Government of India. Such bonds are in great demand from HNIs, who fall in higher tax brackets.

Example:

Issuer: Indian Renewable Energy Development Agency Limited

Coupon Rate: Coupon 7.17% p.a

ISIN: INE202E07179

Callable: Callable bonds are bonds in which the issuer has the option to call back the bonds before it reaches the maturity date. Callable bonds offer a higher rate of interest than noncallable bonds of equal quality. As calling the bonds is an option and is not binding, so if needed, the issuer can also skip calling the bonds on the call date.

Example:

Issuer: Indian Bank

Coupon Rate: 9.53% p.a

ISIN: INE428A08101

Call Date: 27-Dec-2024

Convertible: A convertible bond gets converted into its issuer’s common stock/ shares on the date of maturity or conversion.

Example from history:

During the ’80s, when Dhirubhai Ambani was scaling up Reliance Industries, he frequently used convertible bonds to raise funds. On the conversion date, the bonds would be converted to an equivalent number of shares based on RIL’s current share price at that time.

Senior and Subordinate Bonds: Senior Bonds are the bonds considered before other junior bonds in the hierarchy of payment during liquidation of the issuer. In the extreme case of liquidation of the Bond Issuing company, “senior bonds” are paid off before subordinate bonds. Senior Bonds come with lower risk. Subordinate bonds come with higher returns and relatively higher risk.

Example: (Senior Bonds)

Example:

Issuer: REC Limited

Coupon Rate: 7.93% p.a

ISIN: INE020B07GG9

Example: (Subordinate Bonds)

Issuer: The Tata Power Company Limited

Coupon Rate: 10.75% p.a

ISIN: INE245A08042

Secured and Unsecured Bonds: Secured Bonds are bonds that are collateralized by an issuer’s assets or future cash flows. If the issuer defaults, then bondholders can claim the assets or the cash flow generating source. Unsecured Bonds don’t come with any collateral. If the issuer defaults, unsecured bondholders can’t claim any of the issuers’ assets. Here investment decision is taken purely on trust in the issuer and credit history of the issuer. All unsecured bonds are not unsafe. In the case of unsecured bonds, the creditworthiness of the issuer’s matters. For example, US Treasury Bills are considered to be one of the safest fixed-income bonds worldwide. However, these T Bills are unsecured in nature. During bankruptcy, secured bonds are paid before unsecured bonds.

Example: (Secured Bonds)

Issuer: MANAPPURAM FINANCE LIMITED

Coupon Rate: 9.25% p.a

ISIN: INE522D07BG1

Example: (Unsecured)

Issuer: Cholamandalam MS general insurance company

Coupon Rate: 8.75% p.a

ISIN: INE439H08012

Tier I Bonds and Tier II Bonds: Tier I Bonds are also called Perpetual Bonds. As per BASEL III norms, theoretically, these bonds can be carried on till infinity. In reality, they come with a call option after 5 years or 10 years from the date of issuance. It is a popular option among Banks to raise capital to meet their core capital (Tier I capital) needs as instructed by RBI.

They carry considerable risk and hence pay high-interest rates to investors. The issuer can skip interest payments if the current year’s business is at a loss. In dire conditions, it can get converted to equity (with approval from RBI). Hence they are also called “quasi-equity.” If RBI approves, then it can be written off up to the full value as well.

In case of winding up of the issuer, if any payment is to be made to Tier I capital holders, ATI bondholders are paid before equity holders. . However, in case the Bank is getting merged with another Bank due to its non-viable business state, then AT1 Bonds can be written off fully while keeping the equity capital unaffected.

Example:

Issuer: The South Indian Bank Limited

Coupon Rate: 13.75% p.a

ISIN: INE683A08051

As per BASEL III norms, Banks raise money via Tier II bonds to meet regulatory norms around capital adequacy. Tier II bonds are subordinated debt and hence not first to be paid during the liquidation process. Tier II bonds are senior to Tier I Bonds. When a bank has to write off losses, it will first write off Tier I bonds and then, if required, move on to Tier II bonds. It also can be written off if PONV (point of non-viability) is triggered.

Example:

Issuer: Indian Bank

Coupon Rate: 9.53% p.a

ISIN: INE428A08101

Advantages and Disadvantages of Corporate Bonds

Advantages:

- Corporate bonds offer higher yields than G-secs. For example, the 10-year G-sec yield is around 6.0%, and the yield from Indiabulls Housing Finance Limited’s bonds is 10.89%. Indiabulls Housing Finance Limited has been rated AA+ by CARE.

- The maturity of corporate bonds is usually shorter than that of Gsecs; hence these bonds are less vulnerable to inflation.

- The number of corporates going bankrupt is not zero but rare. During the insolvency of the issuer, bondholders are paid before shareholders.

- Corporate bonds are a level riskier than G-secs but safer than equities.

- The liquidity of corporate bonds is high. They can be bought and sold with ease.

Disadvantages:

- Most Corporate Bonds carry a minimum investment value of 2 Lacs and above. So, not everybody can afford Bonds.

- In the long run, returns from corporate bonds can be lower than equities.

- The corporate bond market is a quite happening place; hence demand and supply of corporate bonds may fluctuate. So, at times, a bond may become unavailable in the secondary investment market.

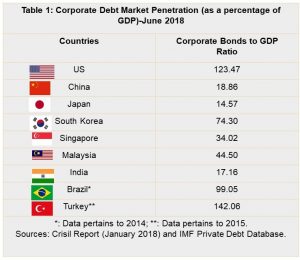

A glance at the WorldwideCorporate Bond Market

Interesting facts about the Corporate Bond Market

- The corporate bond market has deeper penetration in developed countries such as the USA.

- The total outstanding global corporate debt market was $13.5 trillion in 2019. It has grown to 200% since the last recession in 2008. (Remember the Lehman Brothers crisis in Wall Street?)

- Globally, the corporate bond market is performing well, with high volumes of bonds being traded every day.

- In India, it is developing fast. Government and SEBI have a laser-sharp focus on making this market-wide and deep.

- Listed Corporate bonds are available on the National Stock Exchange, Bombay Stock Exchange, and the online platform of GoldenPi.

Select bonds, make a payment, and receive bond units in your Demat account. To view the collection of Corporate Bonds, click here.

1 comment

Hi Varghese,

Please sign up with us. https://goldenpi.com/sign-up

A dedicated Relationship Manager will be assigned to you who will support you with all the required details.

Regards

GoldenPi Team

Comments are closed.