|

Getting your Trinity Audio player ready...

|

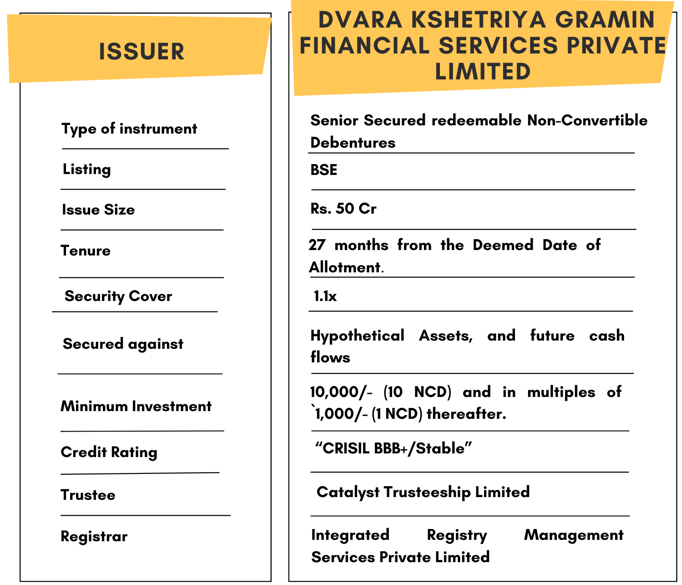

High Yield | BBB+/Stable | Minimum Investment: 10k Only

# Backed by Dvara Trust, the founders of Northern Arc Capital

Dvara Kshetriya Gramin Financial Services Private Limited is issuing the Non-Convertible Debentures via Private placement. These NCDs are BBB+/Stable rated by CRISIL. The NCDs are being issued with a tenure of 27 months. The NCDs are secured and redeemable in nature.

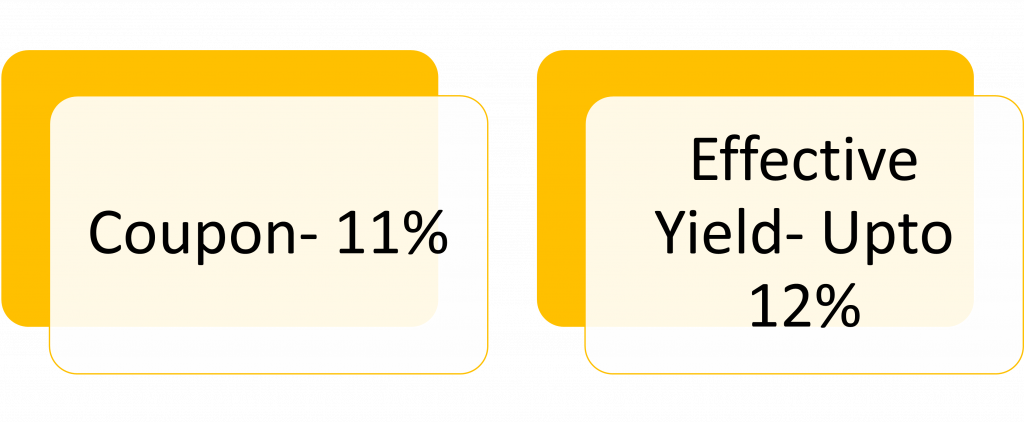

Dvara Kshetriya Gramin Financial Services Private Limited :Coupon rates and effective yield

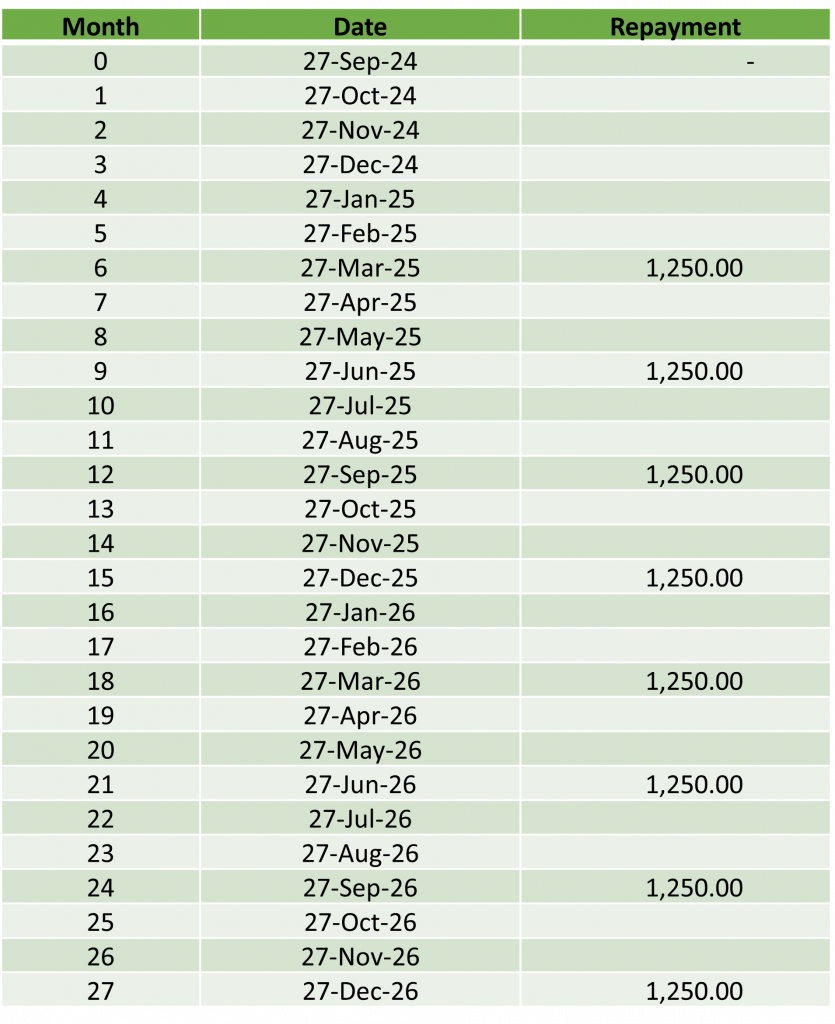

Redemption Schedule

For every 10,000 invested-

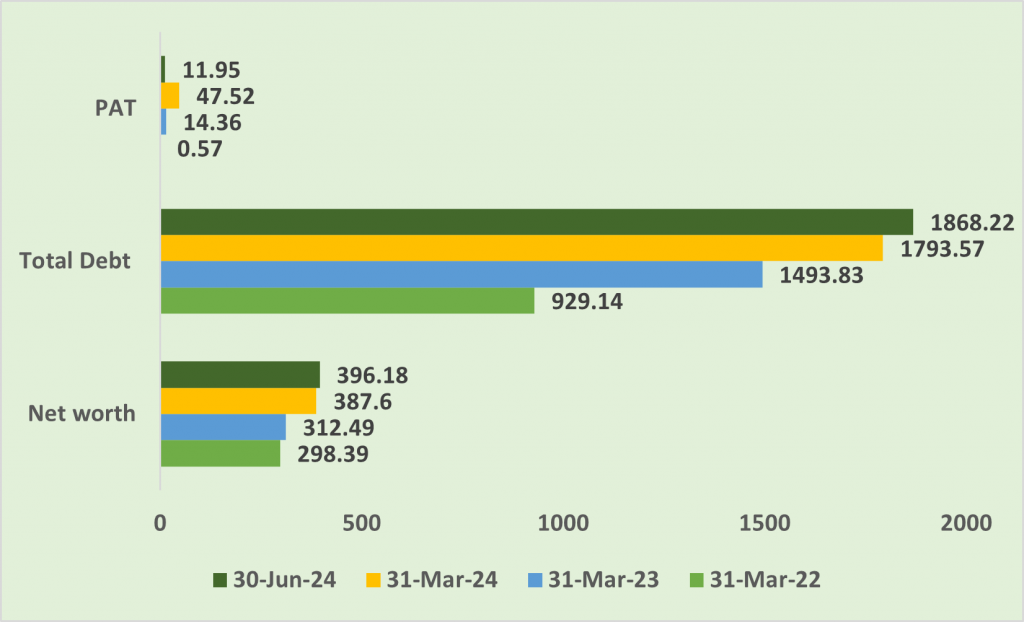

Financial Overview

Snapshot stating the Revenue, Expenses, Net Worth and PAT (In crores)

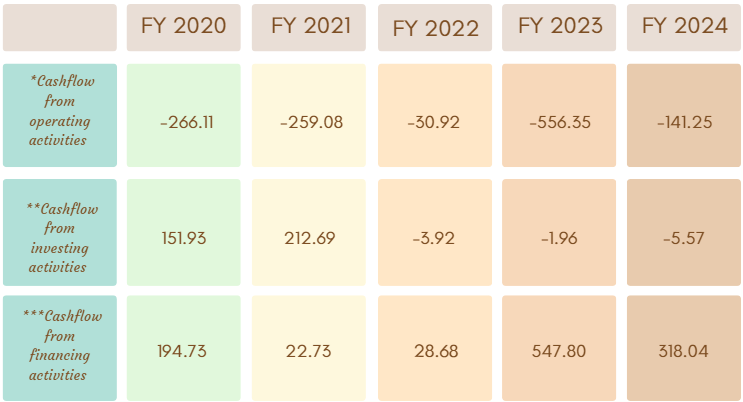

Cash flow for last few years (In crores)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

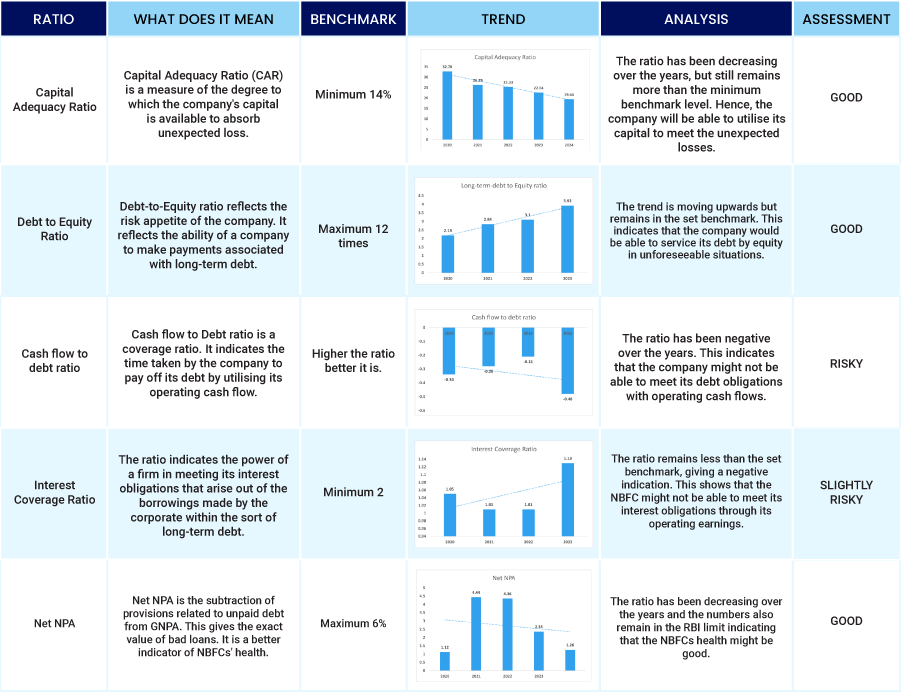

Ratio Analysis

Issue analysis

Pros

- The yield offered is up to 12% which is much higher than many traditional fixed-income investments like FDs.

- The NCDs are BBB+/Stable by CRISIL, ensuring safer investments.

- The company maintains a good Capital Adequacy Ratio, indicating that it has a sufficient capital buffer to absorb unexpected losses.

Cons

- Negative Cashflow

Liquidity

- Liquidity Cover: As of August 31, 2024, the company had a liquidity cover of 1.18x over its upcoming debt obligations for the next two months, assuming 75% collection efficiency.

- Cash Reserves: The company held ₹243 crore in cash, liquid investments, and unutilized debt facilities.

- Debt Obligations: Against the cash reserves, the company faced debt obligations of ₹307 crore for the period through October 2024.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About Dvara Kshetriya Gramin Financial Services Private Limited

Dvara Kshetriya Gramin Financial Services Private Limited (Dvara KGFS), founded in 2008 by Dvara Trust, focuses on providing secured and unsecured loans to underserved rural areas in India. With over 95% of its portfolio in Joint Liability Group (JLG) loans and unsecured enterprise loans, the company plays a vital role in rural financing. Operating across 10 Indian states with 395 branches, Dvara KGFS serves more than 1.2 million customers in 21,641 villages, offering interest rates between 24.5% and 29% on its loan products to meet diverse financial needs.

Financials as on 30th June 2024

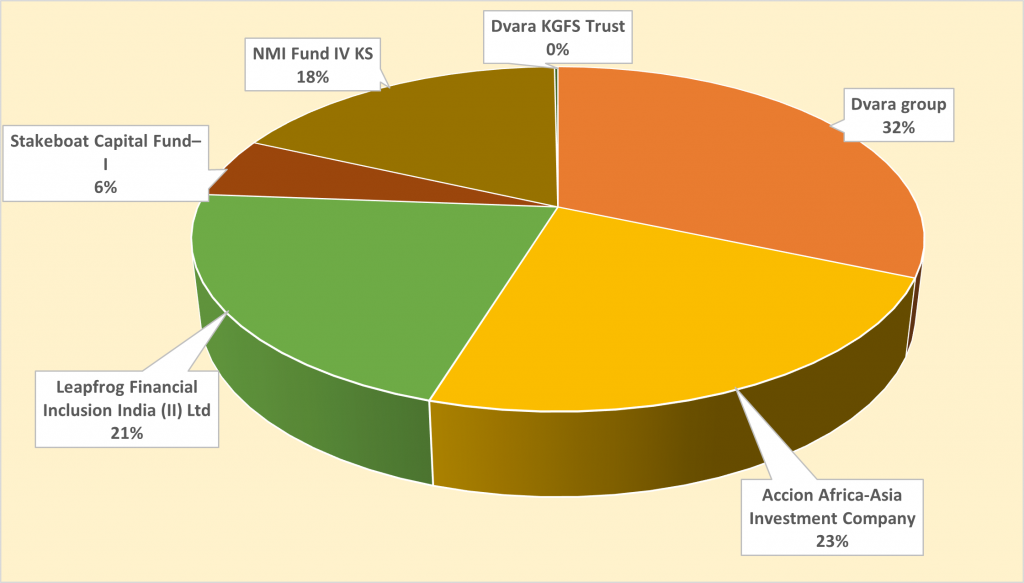

Shareholding Pattern

Strengths

- AUM Growth: The company’s Assets Under Management (AUM) grew 27% YoY to ₹2,251 crore by March 2024, with a further rise to ₹2,342 crore by June 2024. Disbursements grew by 17%.

- Strategic Acquisition: Acquiring 25.9% stake in Saija Finance in FY22 diversified its geographic reach.

- Asset Quality: GNPA stood at 3.2% by June 2024, improving from 4.0% in March 2023.

- Average collection efficiency: 1 st quarter- 2025- 96%, lower than last quarter of 97.5%. Reason- factor of external challenges like heat wave, elections and otherground level issues which surfaced during the quarter

- Profitability: FY24 PAT was ₹48 crore, RoMA at 1.9%, improving from ₹14 crore in the prior year. This improvement was a factor of improvement in yield and overall streamlining and increase inefficiency of operations. For Q1 2025, the company reported a PAT of Rs 12.0 crore and RoMA of 1.7% (annualized).

- Networth and Tier I capital adequacy ratio of 16.1% as on June 30, 2024 vis-a -vis Rs 388 crore and 17.2%, respectively, as on March 31, 2024.

- Gearing: The company’s book gearing rose to 4.7x by June 2024 as compared to 4.3 times, as on March 31, 2023

Weakness

- Write-Offs: Over the last three fiscals (up to March 2024), the company wrote off approximately ₹150 crore in bad loans.

- Portfolio Health: Only about 7% of the loan book is over 90 days past due (dpd), reflecting controlled delinquency.

- Loan Distribution: 82.8% of the portfolio consists of Joint Liability Group (JLG) loans, with the remainder in enterprise loans and other products.

- Geographical Concentration: Tamil Nadu accounts for 49% of the portfolio, followed by Bihar with 14% as of June 2024.

Invest in Bond IPO online in just 5 minutes

Source- Prospectus September 26, 2024

Disclaimer- The information is published as on date 10/04/2024 based on information available on Prospectus September 26, 2024. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors

Latest Updated: 23-02-2026