|

Getting your Trinity Audio player ready...

|

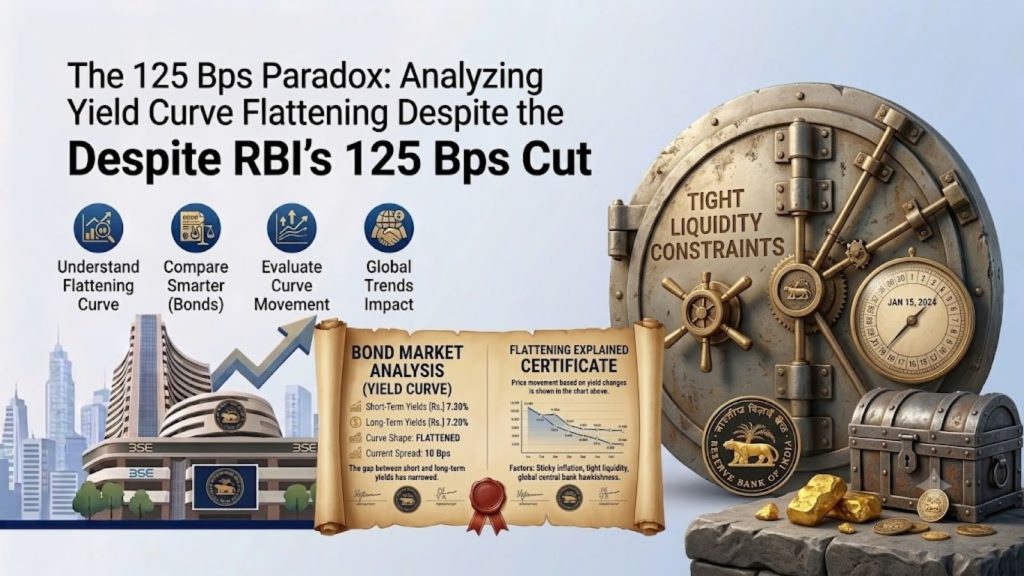

If you jumped into a long-duration gilt fund back in late 2025, expecting the market to go wild, you’re probably scratching your head right about now, wondering what happened. The Reserve Bank of India just pulled off one of its most dramatic easing cycles since COVID, slashing 125 basis points off the repo rate, which now sits at 5.25% [1]. You’d think that’d be enough to spark a full-blown bond rally, but the benchmark 10-year government bond yield has been stuck in this ridiculously narrow range, just drifting lazily between 6.75% and 7.0% for months on end. And retail investors who went all-in on long-duration debt funds, hoping for lucrative double-digit capital gains, are now looking at returns that barely beat a savings account. So, why hasn’t this super-aggressive rate-cutting cycle delivered the bond bull run investors were promised?

The Broken Textbook Promise: Why Easing Didn’t Trigger the Bond Price Rally

Here’s the mechanic every finance student learns early: When a central bank slashes interest rates, it means newly issued bonds have lower coupons, which in turn makes existing bonds with higher coupons way more appealing, and naturally, their prices go up. It’s pretty simple; rates and bond prices have an inverse relationship.

Now, if you crunch the numbers on this whole cycle, a 125 bps repo cut should’ve theoretically sent long-term yields tumbling down to around 6.25%. Instead, they’re just sort of stuck near 7%. That gap would’ve meant ample double-digit capital gains for anyone holding onto long-duration gilt or dynamic bond funds. But here’s the problem: The usual connection between policy rates and bond prices has observably weakened in 2026. There are three key structural forces at play, and getting a handle on them is basically the difference between continuing to hope for the best and repositioning smartly.

Start investing with just 10K & grow your wealth with fixed-return bond opportunities.

Explore NowThe Three Macro Culprits Behind the Sticky Yields

The stickiness of the 10-year G-Sec yield near 7.0% is not random. It is driven by three distinct macroeconomic factors balancing out the RBI’s rate cuts:

The Record Market Borrowing Supply Inflow

Even with the RBI easing up, the government still needs to fund itself, and that’s a pretty big bill. The Union Budget for FY27 is looking at a record ₹17.2 trillion [2] in gross market borrowing, which is roughly 16-17% higher than what they borrowed in FY26. And that’s partly because they’ve got a bunch of maturing bonds that need to be paid off. Now, when you flood the market with all this new government paper week after week, it’s just basic supply and demand: bond prices are gonna go down, and yields are going to go up, no matter what the central bank is doing.

- Gross borrowing FY27: ₹17.2 trillion (vs ₹14.6-14.8 trillion in FY26)

- Net borrowing FY27: ₹11.73 trillion

Protecting the Real Rate of Return Against Sticky Inflation

The RBI’s June 2026 policy did something unusual for an easing cycle: they actually revised their inflation forecast upward, to 5.1% for FY27 [1], while also trimming their GDP growth estimate to 6.6% [1]. And the reason for that? Mostly external. All the geopolitical tension in West Asia has kept crude oil prices all over the place, and since India imports a lot of energy, any spike in prices quickly affects inflation. So, bond investors demand a higher risk premium on long-dated papers because if inflation stays high for too long, the fixed coupon they’re getting today isn’t going to be worth as much in real terms.

Recent Bond News:

- SGB Premature Redemption vs Selling on Stock Exchange: Which is Better?

- The Bond Market Paradox: Why Prices Haven’t Rallied Despite RBI’s 125 Bps Cut

- Tax Rules on Sovereign Gold Bond Redemption in 2026: What Investors Should Know

The Diminishing India-US Yield Spread

Bonds don’t trade in a vacuum. The US Federal Reserve is still being restrictive, and with 10-year US Treasury yields hovering around 4.35-4.40% [3], the spread between US and Indian sovereign debt has narrowed to about 235-250 bps, which, historically speaking, is pretty thin. And for Foreign Portfolio Investors (FPIs), that shrinking cushion is a big deal, because the cost of hedging the rupee can quietly eat into whatever profit they’re making from arbitrage, making them less aggressive buyers of Indian debt than the whole rate-cut narrative would suggest.

| Metric | Level (as of late June 2026) |

| RBI Repo Rate | 5.25% (down 125 bps cumulative) |

| 10-Year G-Sec Yield | 6.75%-7.0% |

| FY27 CPI Inflation Forecast | 5.1% |

| Gross Government Borrowing (FY27) | ₹17.2 trillion |

| US 10-Year Treasury Yield | 4.40% |

| Approx. US-India 10Y Spread | 235-250 bps |

Worth noting: Yields did dip to a 15-week low of around ~6.7% back in late June, but that was largely due to the government throwing tax incentives at FPIs using the Fully Accessible Route; not exactly the kind of broad-based rally a 125 bps cut was supposed to produce.

What This Means for Your Debt Portfolio

If you’re already invested or thinking of investing in long-duration gilt or dynamic bond funds just to make a quick capital gain, you might want to dial back your expectations. The usual rally that comes with a rate-cut cycle just isn’t happening this time around, and those underlying structural pressures aren’t going away anytime soon.

The more attractive spot on the curve right now sits at the short-to-medium end:

- Liquid and money market funds

- Ultra-short and low-duration debt funds

- 1-to-3-year bank Certificates of Deposit (CDs)

These instruments are offering decent, stable yields without all the price volatility that comes with long bonds. It’s all about shifting your mindset: Instead of betting on price rallies, you’re better off focusing on harvesting accrual income and collecting steady interest, rather than chasing some capital-gains dream that just isn’t supported by current macro conditions.

Frequently Asked Questions

Because heavy government borrowing, sticky inflation, and a shrinking US-India yield gap have offset the usual rate-cut effect on long-term bond prices.

Not necessarily if your investment horizon is longer than 5 years. While you won’t see immediate capital gains from a bond price surge, these funds will continue to accumulate stable interest returns over time. For shorter horizons, however, short-duration or liquid funds offer a safer risk-adjusted profile.

It depends heavily on crude oil prices, the FY27 borrowing execution, and whether the US Fed shifts to a more dovish stance.

Yes. Home loan and floating-rate borrowers have already seen meaningful EMI relief, even though that hasn’t fully shown up in the bond market.

Sources

- https://cfo.economictimes.indiatimes.com/news/policy/rbi-maintains-repo-rate-at-525-in-june-2026-policy-meeting/131521208.

- https://www.business-standard.com/budget/news/centre-to-borrow-record-17-2-trillion-in-fy27-bond-supply-tops-estimates-126020100454_1.html

- https://fred.stlouisfed.org/series/DGS10