Ever since the system of gold having a fixed value pegged to the value of the USD was changed by Nixon decades after world war II, individuals could finally trade gold and the value of the precious metal reached extreme highs in the later decades. The continuous rise of gold finally halted and even reached extreme lows in the late 90s which proved the jittery investor behavior and the inherent volatility associated with the gold trade.

Ever since then, gold has been in long-term cyclic behavior where money from a nervous capital market flows toward gold assets which have a reputation of being valuable just by being in association with inadequate natural reserves. The amount of this resource is fixed and the value in all rational sense should and will continue to increase and all economic institutions have similar views on the precious metal.

The Change in Paradigm

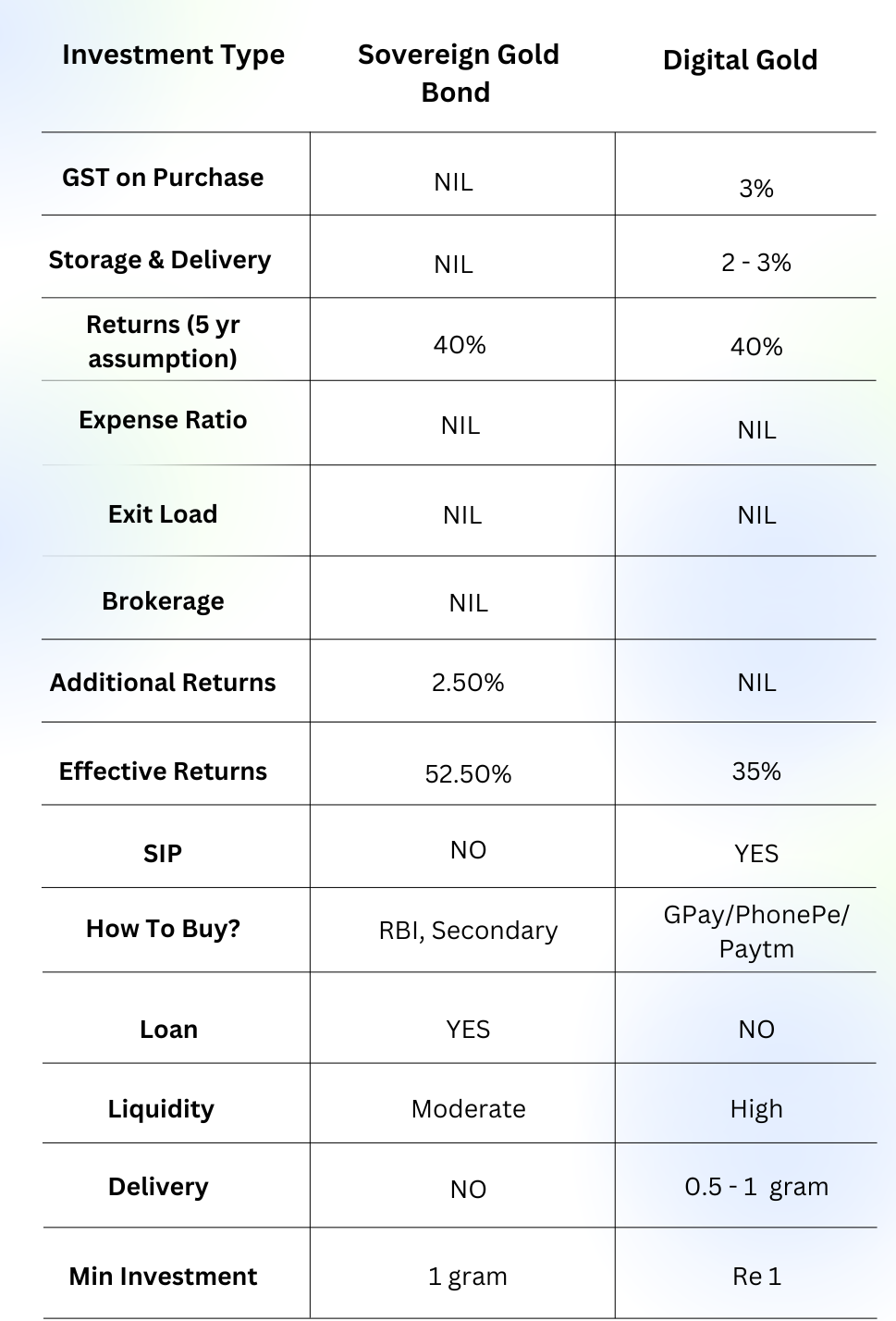

Trading physical gold has been the norm for thousands of years but there are plenty of disadvantages to this which are very well known. In the information age, technology has been leveraged and utilized to come up with digital gold which can be traded all year round from anywhere on the planet. Since gold has been institutionalized and its value recognized globally, this provides the basis of the digital gold trade. The price fluctuations in this volatile asset can be completely mitigated from a long-term investor point of view. Even though all platforms and markets allow the trade of digital gold, it is notable that these might incur charges from the point of sale as the purchased digital gold still needs to be stored safely. 3% of taxes are applicable upon digital gold orders as well.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowSovereign Gold Bond is the Safest Bet!

Sovereign Gold Bonds come to the rescue of intelligent investors when it comes to trading gold assets. The RBI on behalf of the Govt of India issues SGBs and hence the assurance of the investment associated with the allotted gold for the purpose of the bond exists. Even though stable growth cannot be guaranteed by the central bank, this risk exists with the gold asset in general.

However, a 2.5% annual return is guaranteed on the capital invested in the SGB which is paid out biannually. Another important thing to consider is the fact that all capital gains from the maturity of the SGB are exempted from tax completely.

This makes SGB a lucrative deal as the investment earns on the capital which pays out every six months while also holding the appreciating value which will be gained at maturity. The final value at the end of 8 years, which is the maturity period for SGBs, will be the average value of the previous 3 trading days before the maturity date.

What is Sovereign Gold Bond?

But How?

SGBs seem to be the more logical choice compared to digital gold as owning digital gold still has charges involved in the long term. Depending on the type of investment goals, for a long-term investor looking for a safe and strategic investment in the gold asset class, SGBs makes perfect sense. One of the primary concerns anyone might be having is, what if I need to exit early? It is not a worry as early exits are possible. SGBs allow exits during the 5th, 6th, and 7th years from the investment date. But it is notable that such exits will incur CGT (capital gain taxes). It is even possible to exit much earlier by selling the SGB via the national stock markets. The comparison in the below table steers it clear to contemplate the differences.

What is the Difference between Corporate Bond and Government Bond?

In Closing

Investment goals are the prime motivation behind any rational investment decision. If you are an aggressive trader who understands the ins and outs of the micro and macroeconomic factors that influence gold prices and is able to predict gold volatility with a fair bit of certainty, at least with respect to the trend, then digital gold might be a better fit for you.

As the charges for storage will not kick in until after a minimum of 3 months. The downside is the risk associated with exposure to gold’s volatility and no guaranteed return, unlike SGBs. If you are someone who does not wish any exposure to the fluctuations of the gold prices, is interested in building and diversifying your portfolio with guaranteed returns, and beat the short-term fluctuations with high stability and sovereign guarantees from the central bank of India, then SGBs are the way to go.

Investment Strategies in the Bond Market

FAQ’S For Gold Bond and Digital Gold

How do you convert digital gold to physical?

People who have invested in digital gold that are issued by the National Spot Exchange (NSEL) can convert it to physical gold units.

Below are the following steps:

Submit the delivery instruction slip to depository participant along with surrender request form .

DP will credit the digital gold to the NSEL

DP signs the the transfer request form and handover the documents to the investor.

The investor DIS and SRF to NSE and chose the center of the delivery.

Then the investor make payment according to NSEL guidelines.

Then the physical gold will be given to the investor after the ID verification.

Can I transfer digital gold?

Yes, digital gold can be transfer that provide this features and only to accounts within the same platform.

How do I buy and sell digital gold?

To buy and sell digital gold, you will need to find a reputable dealer that offers this service. A dealer will need to set up an account for you and fund it with the amount of gold you wish to purchase. When your account is funded, you can place your order and wait for the gold to arrive. Upon receiving your gold, you can then sell it back to the dealer at the current market price.