(1)")

Sovereign Gold Bonds (SGBs) have emerged as the top choice for investors seeking an alternative investment to gold in India. Issued by the Government of India and backed by the Reserve Bank of India (RBI), Sovereign Gold Bonds allow investors to earn interest along with gaining from the rising value of gold.

In spite of this, there are many questions regarding Sovereign Gold Bonds, particularly among those who will be redeeming their bonds. One of the frequently asked questions is, “How does the redemption of Sovereign Gold Bonds work?”

Be it an early exit from the bond or reaching the maturity period, knowing the process of Sovereign Gold Bonds redemption may prove to be beneficial for your investments.

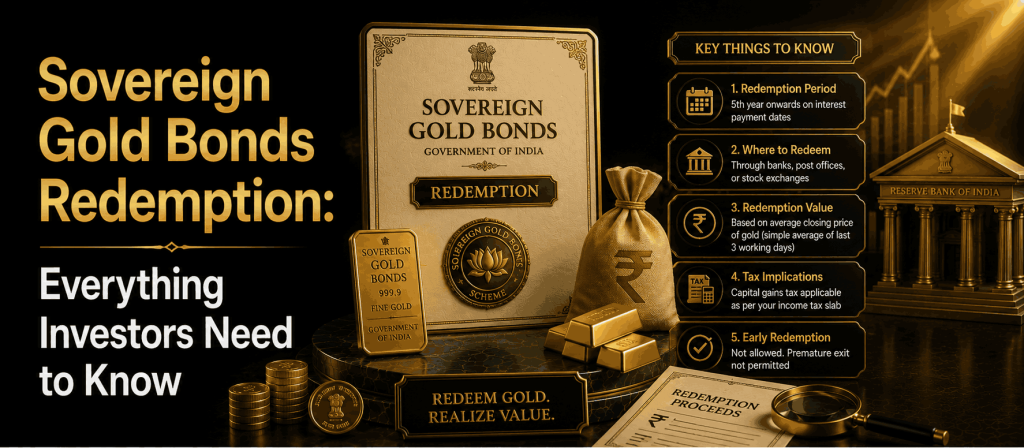

How Does Sovereign Gold Bond Redemption Work?

The sovereign gold bond redemption means the procedure where an individual gets their invested amount on the basis of their holdings of the bond.

As sovereign gold bonds have an 8-year duration, the value of gold in the market at that particular time becomes the redemption price for the investors. Investors get the redemption amount directly into their bank accounts.

In contrast to physical gold, there is no risk associated with the storage or purity of the gold. Also, it doesn’t require any jeweler’s services to sell off the gold.

How is the SGB Redemption Price Calculated?

It is important for one to understand the way that the redemption price for the SGBs is calculated in order to determine the possible gains from investment. The calculation of the redemption price is done through the use of the simple average of the closing gold price of 999 purity gold, which has been provided by the Indian Bullion and Jewellers Association. Using this system, fluctuations in the price of gold have been effectively minimized.

For example, in the case of the price of gold being ₹9,500 per gram and the holding being bonds that have a value of 10 grams of gold, the price of the bond will be around ₹95,000. The actual amount will be determined by the market price of gold at the time of redemption.

What is Premature Redemption in Sovereign Gold Bonds?

Premature redemption refers to the investor’s right to redeem his or her investment five years from the date of issue of the bonds. Such rights become exercisable on interest payment dates fixed by the Reserve Bank of India. This helps investors have the benefits of liquidity options or portfolio rebalancing even before the end of their investment term.

Recent Post:

- Bond Yield vs Interest Rate: Understanding the Difference in Bond Investing

- Long-Term Bonds vs. Long-Term Stocks: Which Investment is Better for Wealth Creation?

- India’s Bond Market: India Considers Tax Cuts to Attract Foreign Bond Investors

How to Redeem Sovereign Gold Bonds Before Maturity

There are two main ways for investors seeking liquidity before eight years of holding the bonds.

The first way is early redemption of the bond through the RBI after completing five years. An application can be made by the investor through the respective bank or post office where they have acquired the bond.

The second way is to sell the bond in stock markets such as the National Stock Exchange and BSE. Since SGBs are liquid assets, investors are able to dispose of them in the secondary markets at prevailing market prices.

But note that the market price may not always match the intrinsic gold value due to reasons such as liquidity and market sentiment. Both choices should be compared before making any decision.

Taxation on SGB Premature Redemption Proceeds

Taxation is one of the key factors that must be considered by investors intending to make an early withdrawal from their investment. The taxation of SGB premature redemption income is determined by the mode used in the redemption process.

In cases where the bond is redeemed by the individual directly with the RBI after the expiry of the appropriate lock-in period, the benefits accorded under the capital gains tax exemption when the investment matures would usually still remain applicable to the individual investor. In instances where the bond has been sold on a stock exchange before it matures, capital gains tax would normally be levied depending on the period of holding of the bond.

Benefits of Holding SGBs Till Maturity

Even though premature redemption ensures flexibility, there are several advantages associated with holding the SGB till maturity.

The first advantage involves the earning of fixed annual interest irrespective of changes in the prices of gold for the entire period of investment.

The second advantage includes gaining from the appreciation in gold prices during the entire duration.

Finally, the third advantage is that of tax efficiency, as it enables individuals to make maximum use of their investments made in SGBs, due to which these become one of the most lucrative gold investments in India.

It can therefore be concluded that maturity redemption results in better tax efficiency for individual investors.

Can I Invest in SGB in 2026?

The first query among potential investors is whether an investor will be able to invest in SGB in 2026.

Investors are advised that as of now, the Indian government has stopped issuing new Sovereign Gold Bond tranches for some time past and will issue new tranches depending upon the needs and considerations of the government.

Should there be any announcement of issuance of new tranches, investors will be able to purchase them from banks, stock exchanges, approved post offices, and other authorized financial organizations.

Gold-oriented investors may also think of purchasing already issued SGB tranches from stock exchanges depending upon their availability.

It is suggested that investors check the RBI and government announcements before investment.

Related Post:

- Gold Price and Bond Market in India: Understanding the Relationship in 2026

- RBI Gold Bond Scheme Explained: A Simple Guide for 2026

- Are Gold Backed Bonds Safe? A Simple Guide for Investors in 2026

Should You Redeem or Continue Holding Your SGBs?

It will depend upon your financial objectives, liquidity requirements, and view on the markets.

In case you require capital or want to include SGBs in your investment portfolio for diversification purposes, it may prove to be an ideal choice when you become eligible.

In the event that your goal is wealth accumulation in the long run, along with the element of gold, keeping SGBs until their maturity will give you the benefit of interest, as well as favorable tax status.

The price of gold currently is not the only factor that investors must take into consideration.

Frequently Asked Questions (FAQs)

Sovereign Gold Bonds have a maturity tenure of eight years from the time of issue.

Yes. Premature exit may be undertaken after five years from the date of issue in accordance with RBI rules.

Redemption value is determined using the average closing rate of 999 purity gold quoted by IBJA in the last three days prior to redemption.

Under current tax laws, capital gain upon early redemption with RBI is usually exempt from income tax.

Yes. Sovereign Gold Bonds can be traded on stock exchanges, including NSE and BSE prior to their maturity.

It depends upon many factors, including market conditions and your personal considerations.

Sovereign Gold Bonds are free from storage worries, robbery issues, and purity tests since they are guaranteed by the Government of India.

Conclusion

Sovereign Gold Bond redemption is a straightforward process, but understanding the nuances of maturity redemption, premature redemption, taxation, and pricing can significantly impact investment outcomes.

For investors seeking long-term exposure to gold with added interest income and potential tax benefits, SGBs remain one of the most efficient gold investment options available. Whether you choose to redeem early or hold until maturity, being aware of the redemption process ensures that you maximize the value of your investment.

Disclaimer:

Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities and municipal debt securities/securitized debt instruments are subject to credit risks, market risks, and default risks, including delay and/or default in payment. Read all the offer-related documents carefully. This blog/article should not be construed as financial advice or as an offer or recommendation to buy or sell any security or any products/services of/on GoldenPi or any product/services of its third-party client(s). For a detailed calculation of YTM, visit our website. T&C’s Apply.

")