|

Getting your Trinity Audio player ready...

|

Fixed deposits are one of the most popular savings tools in India. They’re safe, predictable and easy to open. But one complaint investors often have is this: what if you need the money before the FD matures? Breaking an FD early usually means paying a penalty and losing a portion of the interest you’ve earned.

There’s a way to manage this problem without giving up the benefits of FDs. It’s called the FD laddering strategy.

What Is an FD Ladder?

An FD ladder is a strategy where you split your total investment across multiple FDs with different maturity dates, instead of putting everything into one FD at one time.

But why does this help? Because when your FDs mature at different points, you always have money becoming available at regular intervals. You’re not locked into a single maturity date. And as each FD matures, you reinvest it at the prevailing interest rate, which may be higher than when you originally invested.

This approach tries to solve two problems at once: keeping money accessible when you need it and earning better average returns over time.

To see how this works in practice, let’s walk through a simple example.

Start investing with just ₹10K & grow your wealth with fixed return opportunities.

Invest NowA Simple FD Ladder: How It Works

Say you have Rs. 5 lakh to invest. Instead of putting the full amount into a single 5-year FD, you divide it into five parts and invest each in an FD with a different tenure:

At the end of Year 1, FD 1 matures. You take that Rs. 1 lakh and reinvest it in a new 5-year FD. Now you have FDs maturing in Years 2, 3, 4, 5 and 6.

You keep repeating this every year. Each time an FD matures, you reinvest it at the longer tenure. Over time, all your FDs settle into 5-year tenures, but they mature at staggered intervals, one every year.

The result? You always have an FD maturing within 12 months, so you’re never too far from accessing your money if you need it.

Benefits of an FD Laddering Strategy

Regular access to funds

With staggered maturity dates, you have money becoming available every year. You don’t need to break an FD and pay a penalty just because you need funds at a specific point in time.

Better average interest rates over time

Longer-tenure FDs typically offer higher interest rates than shorter ones. By always reinvesting into a longer tenure as each FD matures, you gradually shift your entire ladder toward higher-rate FDs. And if interest rates rise over time, you benefit because you’re reinvesting at the new, higher rates.

Reduced interest rate risk

If you invest your full corpus in a single long-term FD, you’re locked in at that rate even if rates go up later. With a ladder, only a portion of your money is locked in at any given rate. The rest gets reinvested periodically, so your portfolio naturally adapts to rate changes.

Protection against premature withdrawal penalties

Breaking an FD before maturity usually attracts a penalty of 0.5% to 1% on the interest rate. With a ladder, you can wait for the nearest FD to mature instead of breaking one early, saving that penalty.

Now that you know the benefits, here’s how to build your own ladder step by step.

How to Build Your Own FD Ladder

Following these five steps consistently is what makes the ladder work over the long term.

- Step 1: Decide your total investment amount

Start by deciding how much you want to put into your FD ladder. This could be a lump sum you have available now, or you can build the ladder gradually over time.

- Step 2: Choose the number of rungs

A “rung” is each individual FD in your ladder. Most investors use 3 to 5 rungs, but you can choose more depending on how often you want money to become available. More rungs mean more frequent maturities.

- Step 3: Split the amount evenly

Divide your total corpus equally across the number of FDs you’ve decided on. Equal splits keep the ladder balanced. Unequal splits work too, if you have a specific reason to have more money available at a particular point.

- Step 4: Stagger the tenures

Open each FD with a different maturity date. If you’re building a 5-rung ladder today, open FDs maturing in 1, 2, 3, 4 and 5 years.

- Step 5: Reinvest at maturity

Each time an FD matures, reinvest the principal and interest into a new FD at the longest tenure in your ladder. If your ladder spans 5 years, reinvest each maturity into a new 5-year FD.

Read More

- AI Conquered the Stock Market: Why the Bond Market Is Next

- HUDCO Plans ₹3 Lakh Crore Loan Book by 2030: Key Highlights

- Behind the Record Surge: How Sustainable Is FPI Investment in Indian Debt?

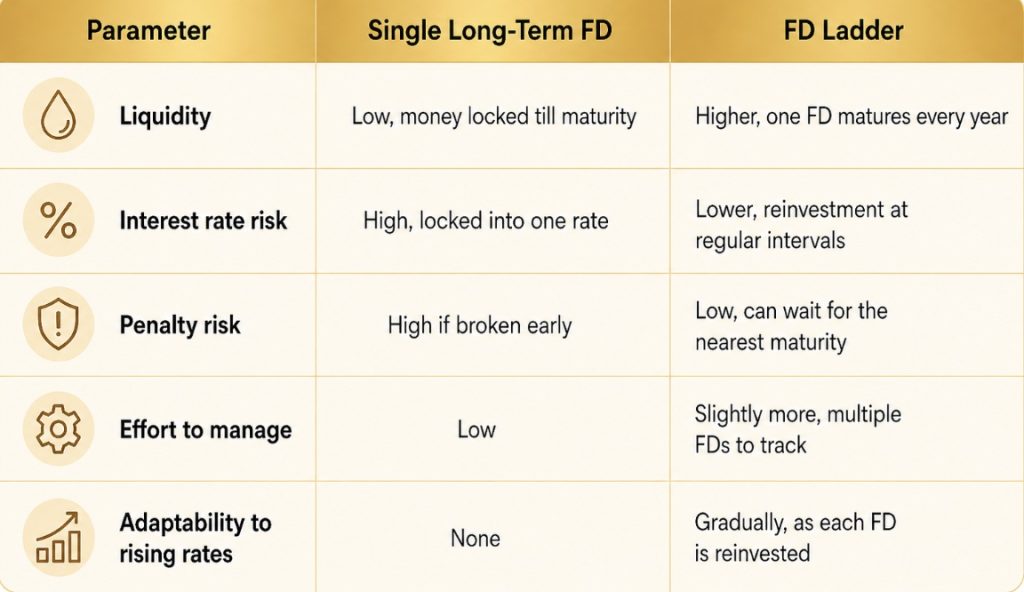

FD Ladder vs Single Long-Term FD: Key Differences

An FD ladder splits your corpus across multiple fixed deposits with staggered maturities, so one FD matures every year. A single long-term FD locks everything into one rate for the entire tenure. The table below shows how the two approaches differ across liquidity, interest rate risk, and flexibility.

A Few Things to Keep in Mind

- FD insurance cover: Deposits in banks are insured up to Rs. 5 lakh per depositor per bank under DICGC. If your ladder involves large amounts across a single bank, keep this limit in mind.

- Corporate FDs vs bank FDs: Corporate FDs often offer higher interest rates than bank FDs but carry higher credit risk. If you include corporate FDs in your ladder, check the credit rating of the issuing company.

- Tax on FD interest: Interest earned on FDs is taxable as per your income tax slab. If your total FD interest in a year exceeds Rs. 40,000 (Rs. 50,000 for senior citizens), TDS is deducted by the bank.

FAQs on the FD Laddering Strategy

An FD laddering strategy is when you split your investment across multiple FDs with different maturity dates, instead of investing the full amount in a single FD. As each FD matures, you reinvest it at a longer tenure. This gives you regular access to funds while earning better average returns over time.

There’s no fixed number. Most investors use 3 to 5 FDs to start. More FDs mean more frequent maturities and better liquidity, but also slightly more tracking. Start with a number that’s easy to manage and adjust over time.

Not necessarily higher at the outset, but it can over time. Since you’re regularly reinvesting at prevailing rates, if interest rates rise, your returns improve gradually. A single long-term FD locks you into one rate for the entire tenure.

Yes. Corporate FDs can be included in a ladder and often offer higher interest rates than bank FDs. Do check the credit rating of the company before investing. Corporate FDs are not covered under DICGC insurance, so the issuer’s financial health matters more.

The benefit of a ladder is that you usually won’t have to wait more than a year for the nearest maturity. If the need is urgent and you can’t wait, you can break the FD that’s closest to maturity to minimise the penalty, rather than breaking a long-term FD midway.

Disclaimer: Fixed returns do not constitute guaranteed or assured returns. Investments in corporate debt securities, municipal debt securities/securitised debt instruments are subject to credit risks, market risks and default risks including delay and/or default in payment. Read all the offer related documents carefully.