")

High Yield | AA-/Stable Rated | Minimum Investment: 10k Only

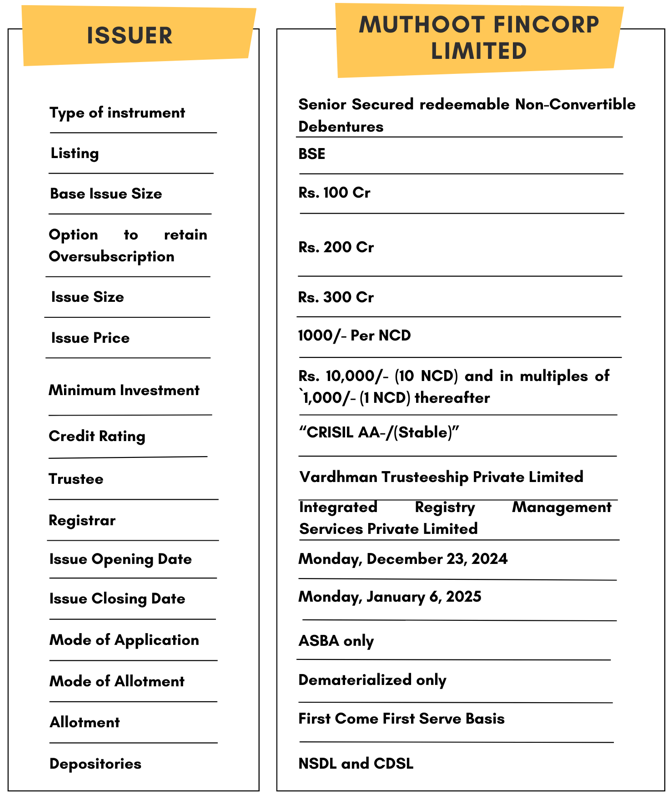

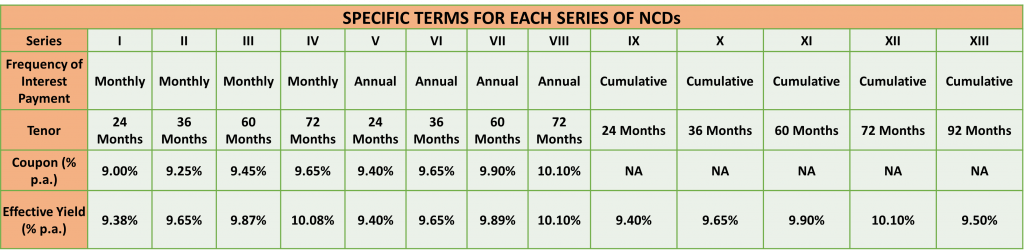

Muthoot Fincorp Ltd is issuing Non-Convertible Debentures. These NCDs are AA-/Stable by CRISIL. The NCDs are being issued in thirteen series: yield ranges from 9.38% to 10.10% p.a. and different tenures of 24 months, 36 months, 60 months, 72 months and 92 months. The NCDs are secured and redeemable in nature.

Muthoot Fincorp Ltd NCD IPO: Coupon rates and effective yield for each of the series

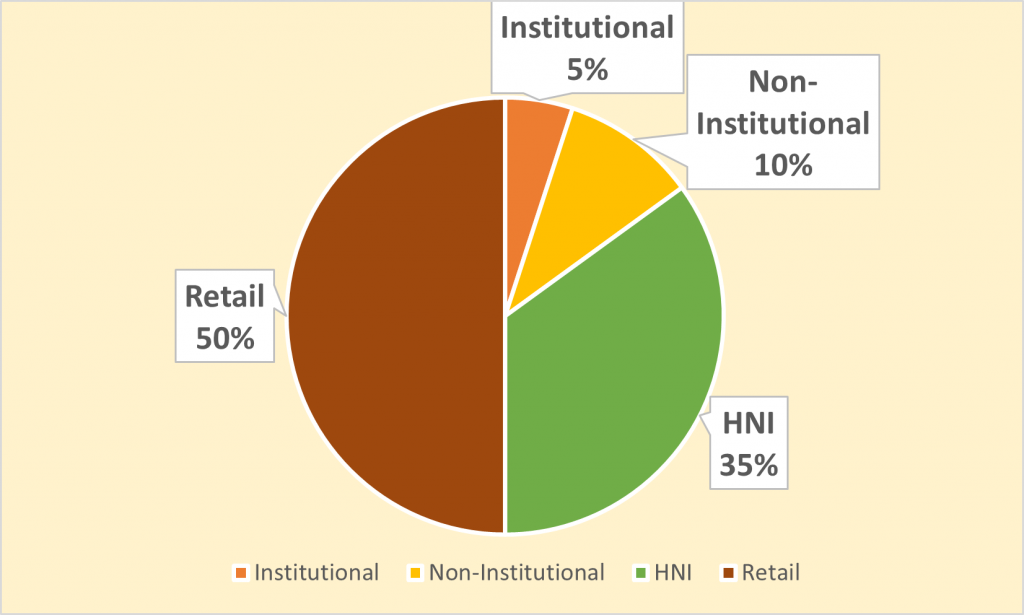

Allocation Ratio

The allocation ratio is prepared based on norms laid down by SEBI. Before announcing the allocation ratio, the same has to be approved by SEBI. Once the IPO subscription closes, applications will be divided into different categories. The category-wise allocation ratio is always decided and declared during the launch of the particular IPO. Considering the Allocation Ratio, units will be assigned to applicants. Refer to the chart to know the application ratio for Muthoot Fincorp Ltd NCD-IPO.

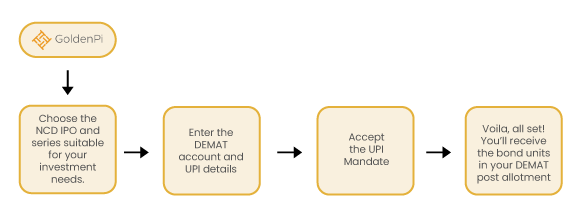

Investment Process for Muthoot Fincorp Ltd NCD IPO

You can invest in IPOs via GoldenPi in these easy steps.

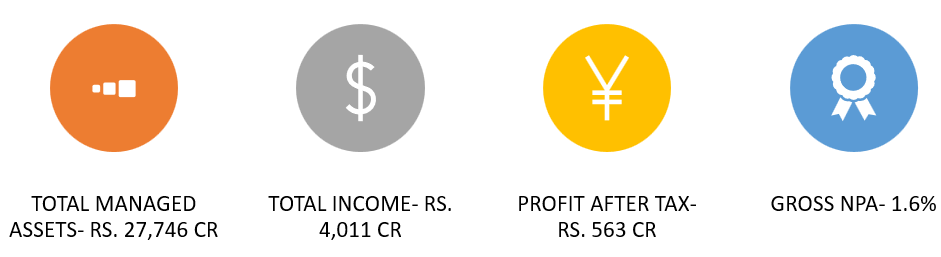

Financial Overview

Snapshot stating the Revenue, Expenses, EBIT, Net Worth and PAT

(Amount in Rs. Cr)

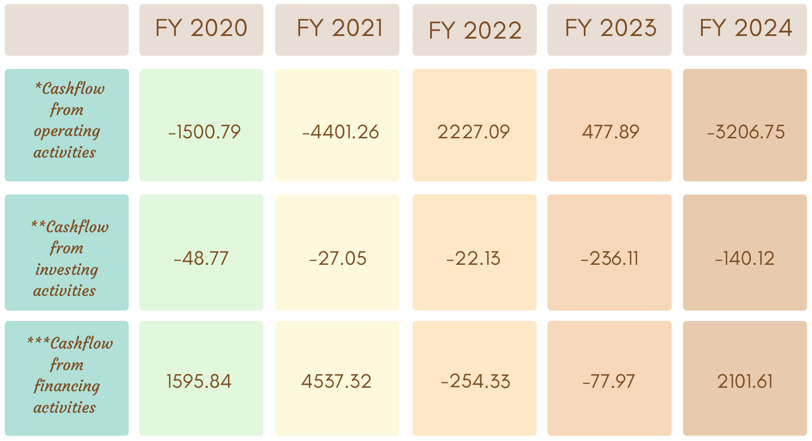

Cash flow for last 5 years

(Amount in Rs. Cr)

Cash flow refers to the movement of cash in and out of the business at a specific point in time. It represents the net balance of the cash movement.

-

- *Cash flow from operating activities reflects the amount a company generates through its product of services.

- **Cash flow from investing activities reflects cash generated and spent relating to investing activities, like purchase of assets, sales of securities etc.

- ***Cash flow from financing activities gives an insight into the financial stability of a company to its investors. It reflects the net flows of cash that are used to fund the company.

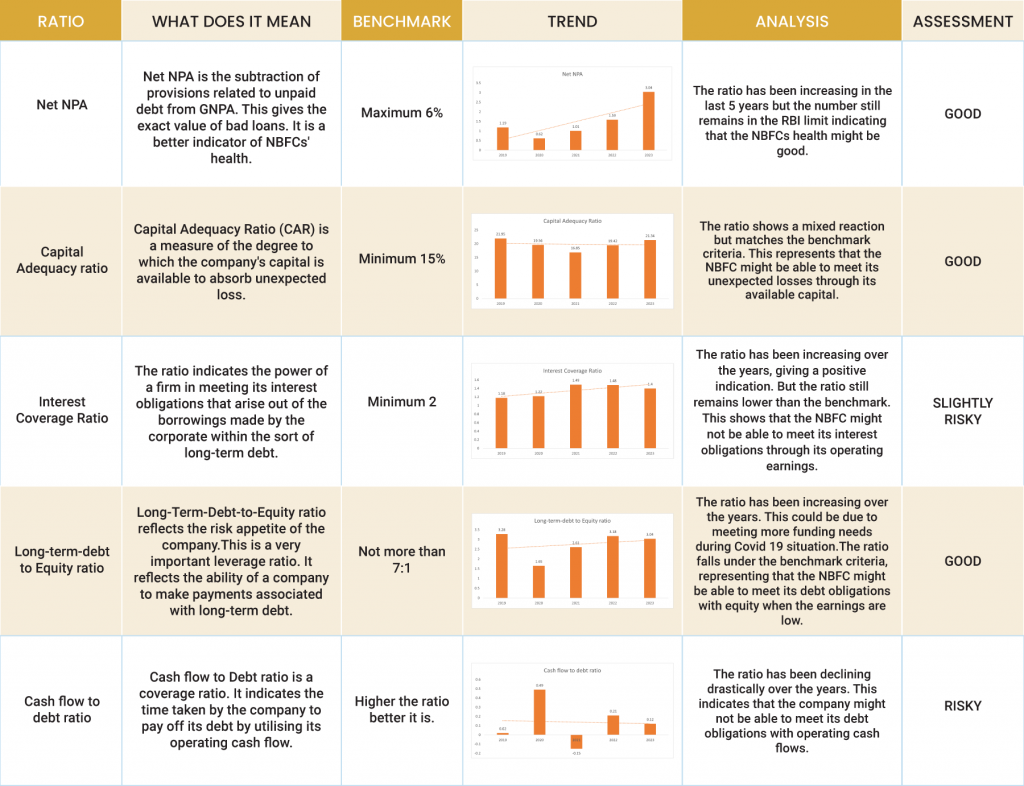

Ratio Analysis

Issue analysis

Pros

- The NCD is AA- rated security with a stable outlook.

- The yield offered is 9.43% which is much higher than FDs.

Cons

- The operations of NBFC is geographically constrained. It is majorly operated in South India.

To get better returns than Bank FDs, invest in NCD-IPOs online.

About MFL

Founded in 1997, Muthoot Fincorp Ltd.(MFL) is a non-deposit taking, one of the leading NBFCs in the country. The NBFC primarily deals into lending against gold jewelry. It is the flagship company of the Muthoot Pappachan Group also popularly known as the Muthoot Blue Group, which has diverse business interests such as hospitality, real estate, and power generation.

Business Verticals

Strengths

Established Market Leadership:

-

- Gold loan portfolio of ₹22,772 crore (54% of total AUM) as of June 2024.

- Promoters with 70+ years of gold lending experience enhance brand trust.

Diversified Offerings:

-

- Operates in 5 segments: gold loans, microfinance, two-wheeler finance, housing finance, and small business loans.

- Total AUM reached ₹42,378 crore in June 2024.

Strong Capitalization:

-

- Standalone net worth at ₹4,875 crore in June 2024.

- Consolidated net worth increased to ₹6,570 crore, supported by ₹760 crore IPO and ₹200 crore stake sale.

Healthy Asset Quality in Gold Loans:

-

- Gold loan GNPA at a low 1.5% as of June 2024.

- Short-tenure products and regular auctions minimize risks.

Earnings Growth:

-

- Standalone RoMA improved to 2.5% in Q1 FY25, the highest in 4–5 years.

- Consolidated RoMA for FY24 reached 2.8%, driven by microfinance and vehicle finance.

Technological Adaptability:

-

- Transition to digital channels for gold loan disbursements during regulatory changes.

Weakness

Geographical Concentration:

- 55% of the gold loan portfolio is concentrated in South India, down from 70% in 2019 but still high compared to peers.

Challenges in Non-Gold Loans:

- Non-gold loans form 48% of the portfolio, with risks in asset quality.

- GNPA for microfinance at 4.3% and vehicle finance at 10.2% (March 2024).

High Gearing:

- Consolidated gearing at ~5 times, though reduced from 5.8 times in FY23.

Regulatory Risks:

- RBI restrictions on cash disbursals for gold loans may impact short-term operations.

Dependence on Gold Prices:

- Portfolio sensitive to gold price fluctuations, though mitigated by short-tenure loans and auctions.

Invest in Bond IPO online in just 5 minutes

Source- Tranche III Prospectus December 12, 2024

Disclaimer- The information is published as on date 19/12/2024 based on information available on Tranche III Prospectus December 12, 2024. The information may be subject to change in case of change in terms of prospectus or any other reason as the case maybe. Contents which are exclusively for educational information/knowledge sharing on capital market concepts and has no influence the investment/sale decisions of any investors